Original Medicare vs. Medicare Advantage

There are many distinct differences between Original Medicare and a Medicare Advantage plan.

My name is Mark Prip, and I’ve been helping Medicare beneficiaries find the right coverage for over 15 years. I’ll start by showing you the most important differences that affect your individual needs for medical care, including:

- Cost sharing

- Out-of-pocket limits

- Prior authorizations

- Provider networks

- Popularity

- Premium costs

- Coverage and benefits

Let’s jump right in.

Important to know:

If you are enrolled in Original Medicare, then you can also enroll in a Medicare Supplement (Medigap) plan to play for all of the gaps in copays, deductibles, and percentages that you’re left with from those high out-of-pocket costs.

If you have a Medicare Advantage plan, you cannot buy a Medigap plan in addition to Medicare Advantage.

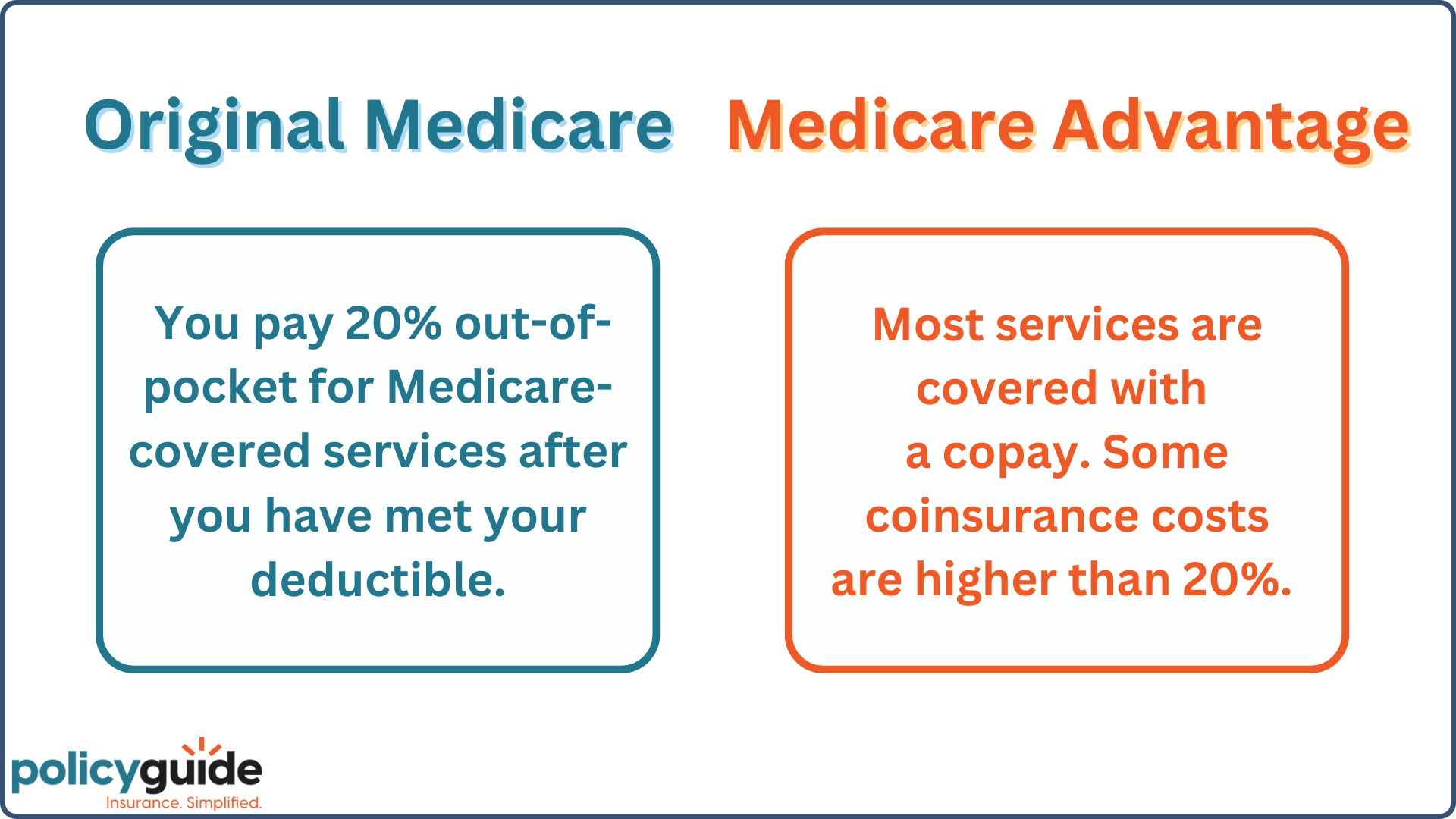

Cost Sharing

Generally, with Original Medicare, you pay 20% out of pocket for Medicare-covered services after the deductibles have been met.

With Medicare Advantage, most services are covered with a copay. Certain services will require a 20% or more coinsurance on a Medicare Advantage plan.

Let’s talk about out-of-pocket limits.

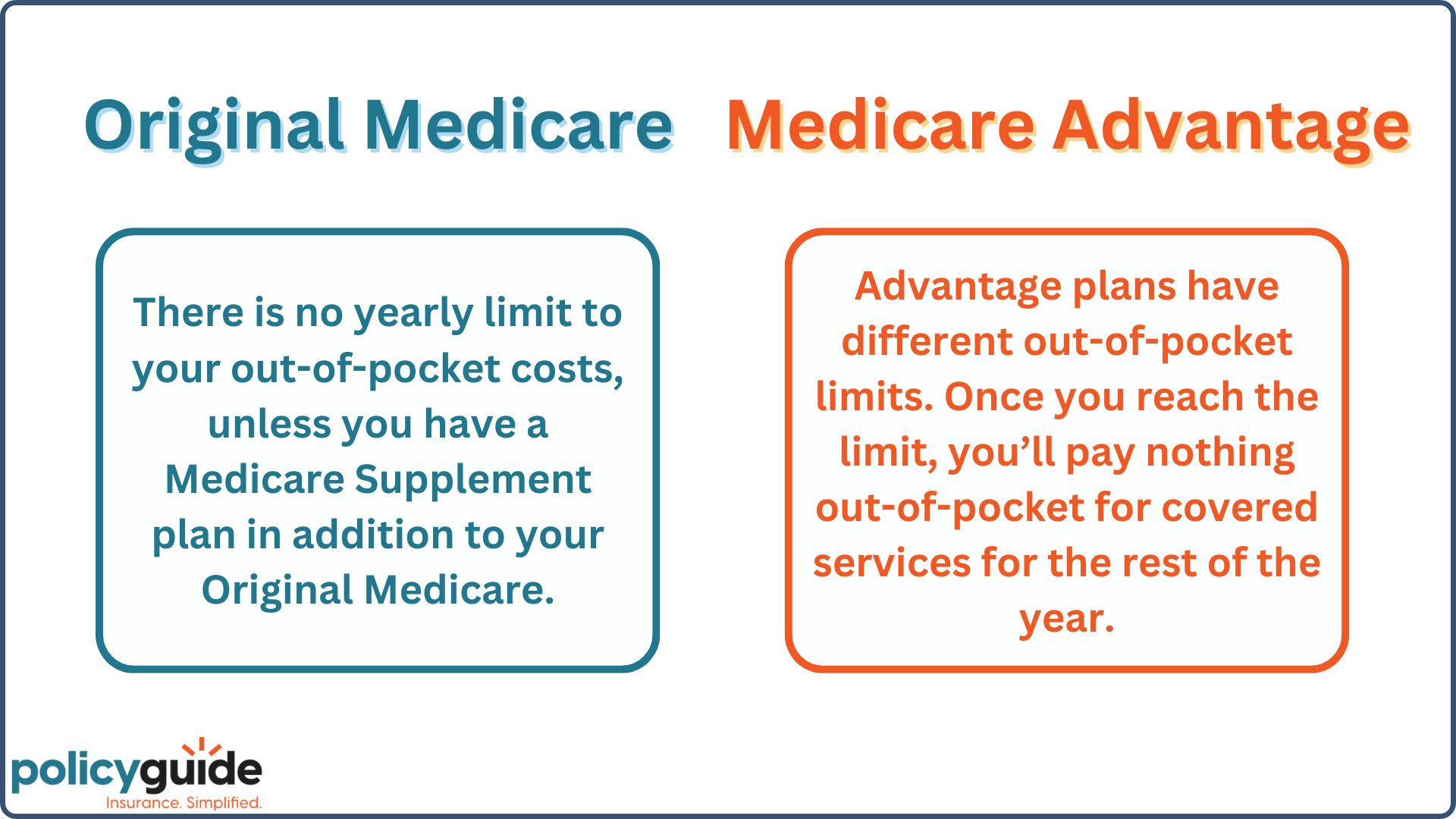

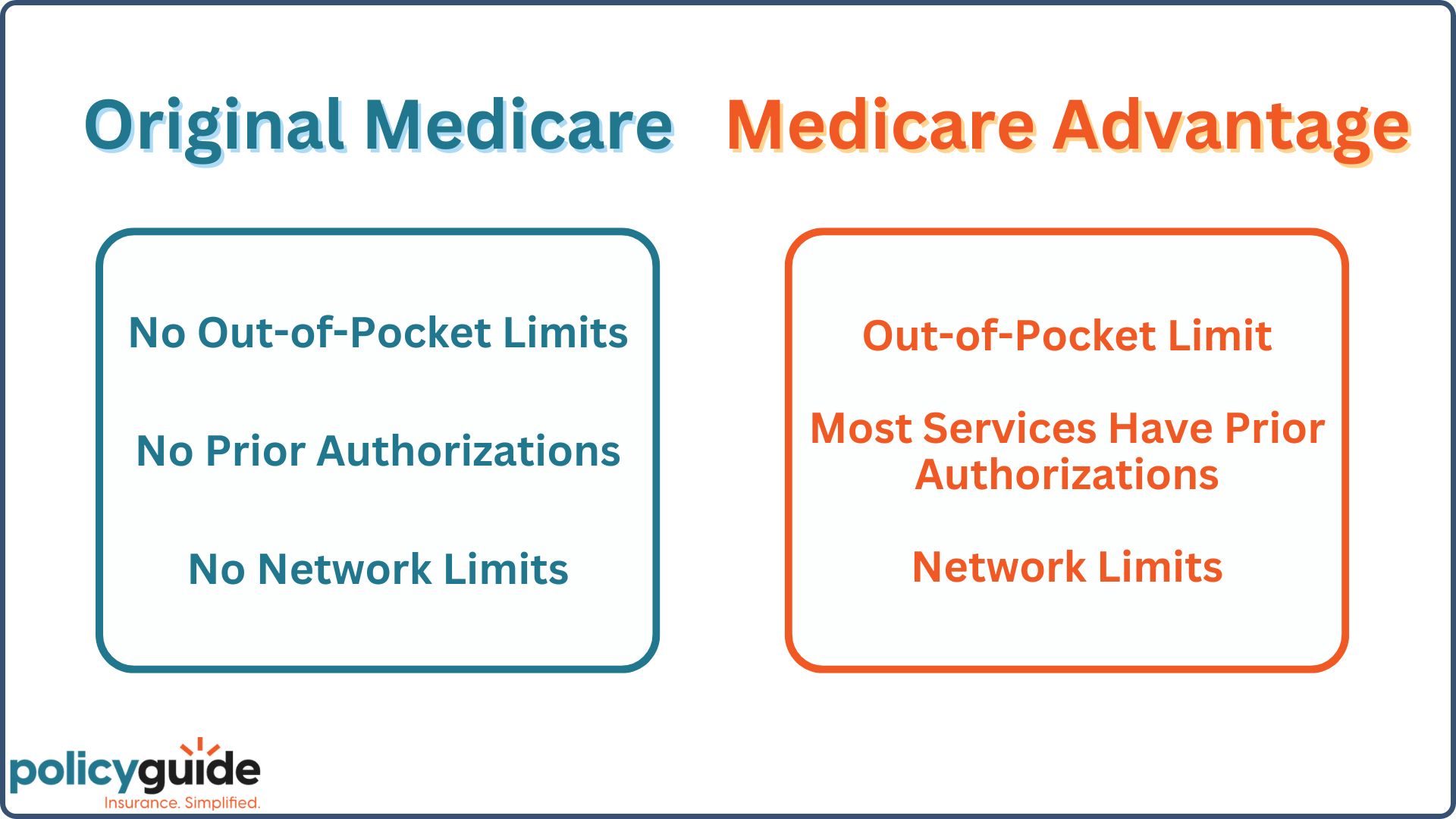

Out-of-Pocket Limits

With Original Medicare, there is no out-of-pocket limit. What does that mean?

That means Original Medicare will pay 80% of your medical bills, and you are responsible for the remaining 20%. Your 20% has no limit.

Here’s an example:

- If you have a $500,000 or a $1,000,000 bill, you are going to pay 20% of that. If your bills are even higher, that 20% will always be in the picture, and it will never have a cap to protect you from those higher claims.

Now, when it comes to your out-of-pocket limit with a Medicare Advantage plan, a Medicare Advantage plan is going to have an out-of-pocket cap.

- So, in that same scenario where you have a $500,000 or a $1,000,000 bill (or even something as low as $1,000), a Medicare Advantage plan will have an annual out-of-pocket limit, which can range from anywhere between $3,500 all the way up to $9,350.

The difference is that Medicare Advantage is going to protect you in those catastrophic events and put that cap on your shared responsibility. Original Medicare will not do that.

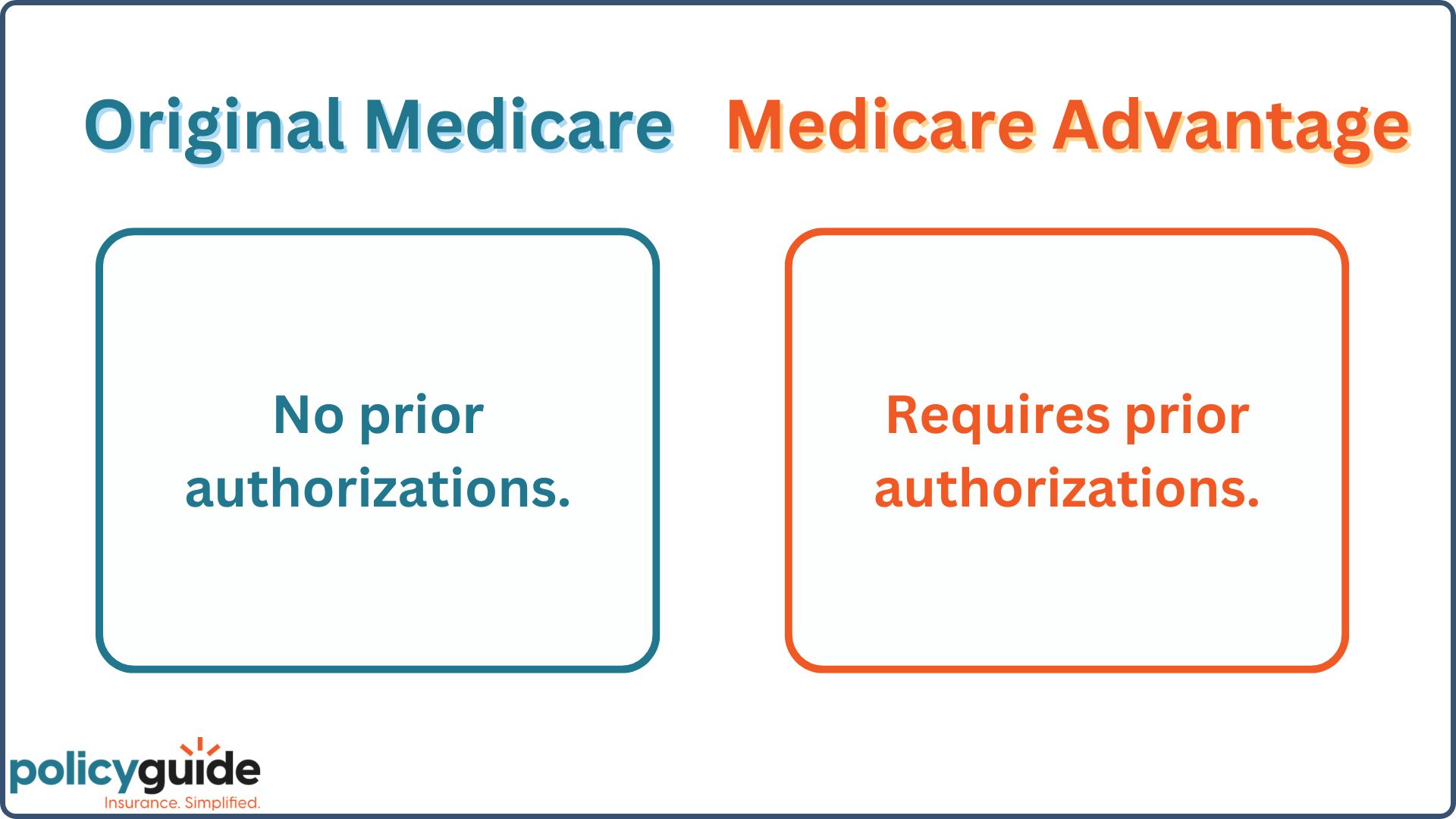

Prior Authorizations

The second difference is that Original Medicare has no prior authorizations.

That means if you need medical tests, surgery, or anything else done in the hospital (or anywhere in between), that service is usually covered, and the procedure can happen immediately.

With a Medicare Advantage plan, almost all services require prior authorization.

So, I’m going to give you a quick real-life scenario:

Let’s say you go into the hospital with Original Medicare only and have chest pains.

They’re going to walk you through all of the tests and procedures immediately to help determine what is wrong.

BUT, if you have a Medicare Advantage plan, in that same scenario, and you go in with chest pain, they may have to ask your insurance provider for prior authorization or prior approval before proceeding with the recommended testing.

I cannot emphasize enough that Medicare Advantage plans all have prior authorization requirements, which equal delayed care. Original Medicare (or Original Medicare with a Medigap plan) does not have prior authorizations.

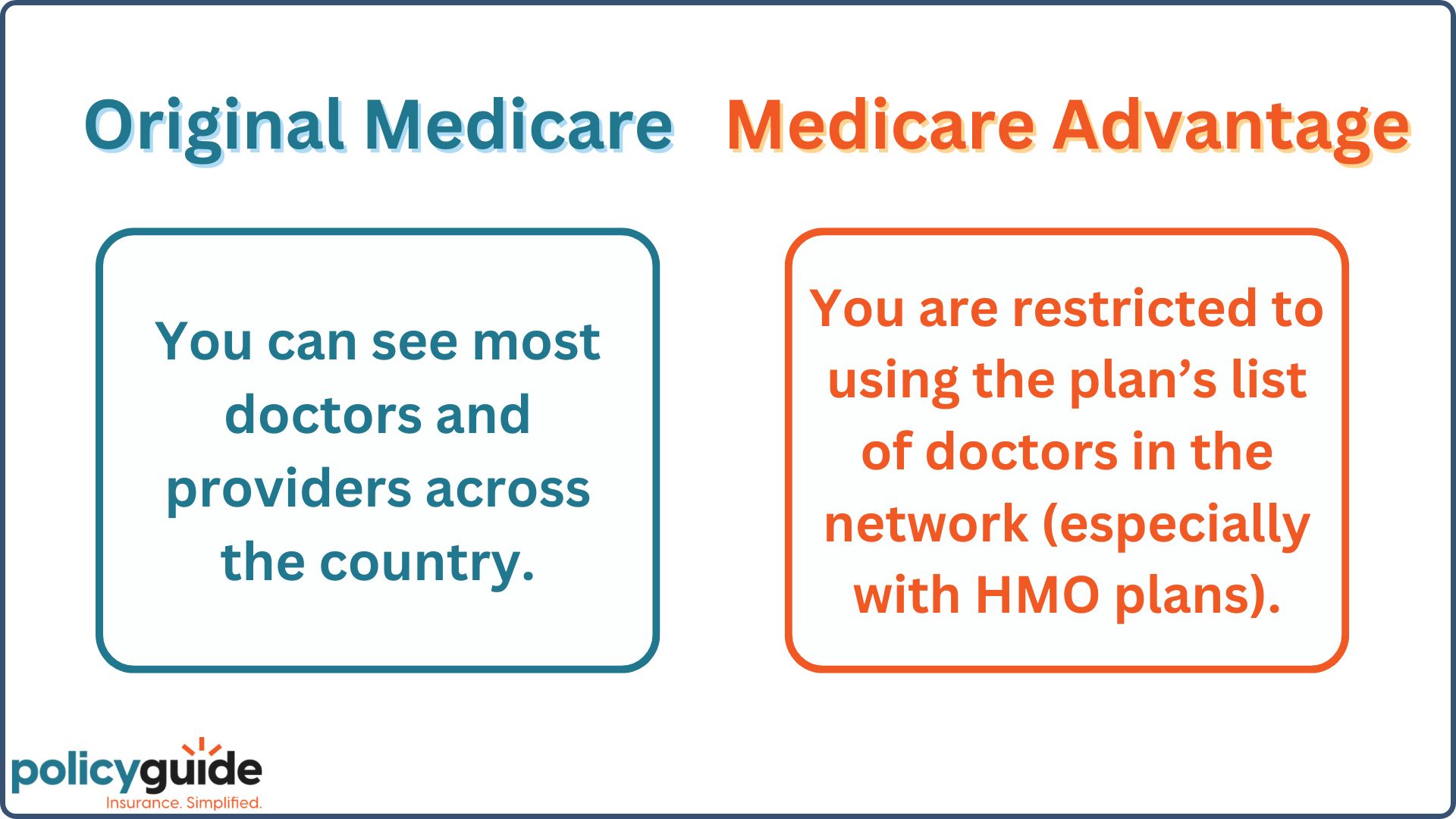

Provider Networks

Let’s break down the differences between the two regarding provider networks.

If you have Original Medicare only, you can see roughly 95% of doctors in facilities across the United States.

If you have a Medicare Advantage plan, especially an HMO, you will be restricted to a much smaller list of providers and hospitals. If you’re on a Medicare Advantage PPO plan, you will still be confined to a network; however, PPO networks seem to be a bit larger.

If you have Original Medicare with a Medigap plan, you can still see the 95% plus medical providers in the U.S. that I initially referenced.

-

Quick Recap!

- No out-of-pocket limit with Original Medicare; Medicare Advantage has a limit.

- No prior authorizations are needed with Original Medicare (or Original Medicare with a Medigap plan). However, most services require prior authorization with Medicare Advantage.

- With Original Medicare (or OM with Medigap), you can see about 95% of medical providers in the U.S. without referrals. Medicare Advantage keeps you in an HMO or PPO network with referrals.

Popularity

The question is – what do most Medicare beneficiaries do when choosing between Original Medicare, a Medicare Advantage plan, or Original Medicare with a Medigap plan?

Take a look at this report I pulled from the Kaiser Family Foundation:

I’ve linked this whole article in the sources below if you want to read it.

As you can see, most people opt for a Medicare Advantage plan. This report is a couple of years old, and today, more than 33 million people are enrolled in a Medicare Advantage plan.

If you look at those enrolled in Original Medicare with no other coverage, there are far fewer—only around 3 million people—who opt to stick with Original Medicare only.

The two choices we see most frequently are:

- #1. Enrolling in a Medicare Advantage plan

- #2. Selecting Original Medicare with a Medigap plan

A far smaller number of people use Original Medicare only, and the data shows that most people opt for Medicare Advantage or Original Medicare with a Medigap plan.

Next, let’s talk about some differences between the actual premium cost, and then we’ll break down the actual benefits.

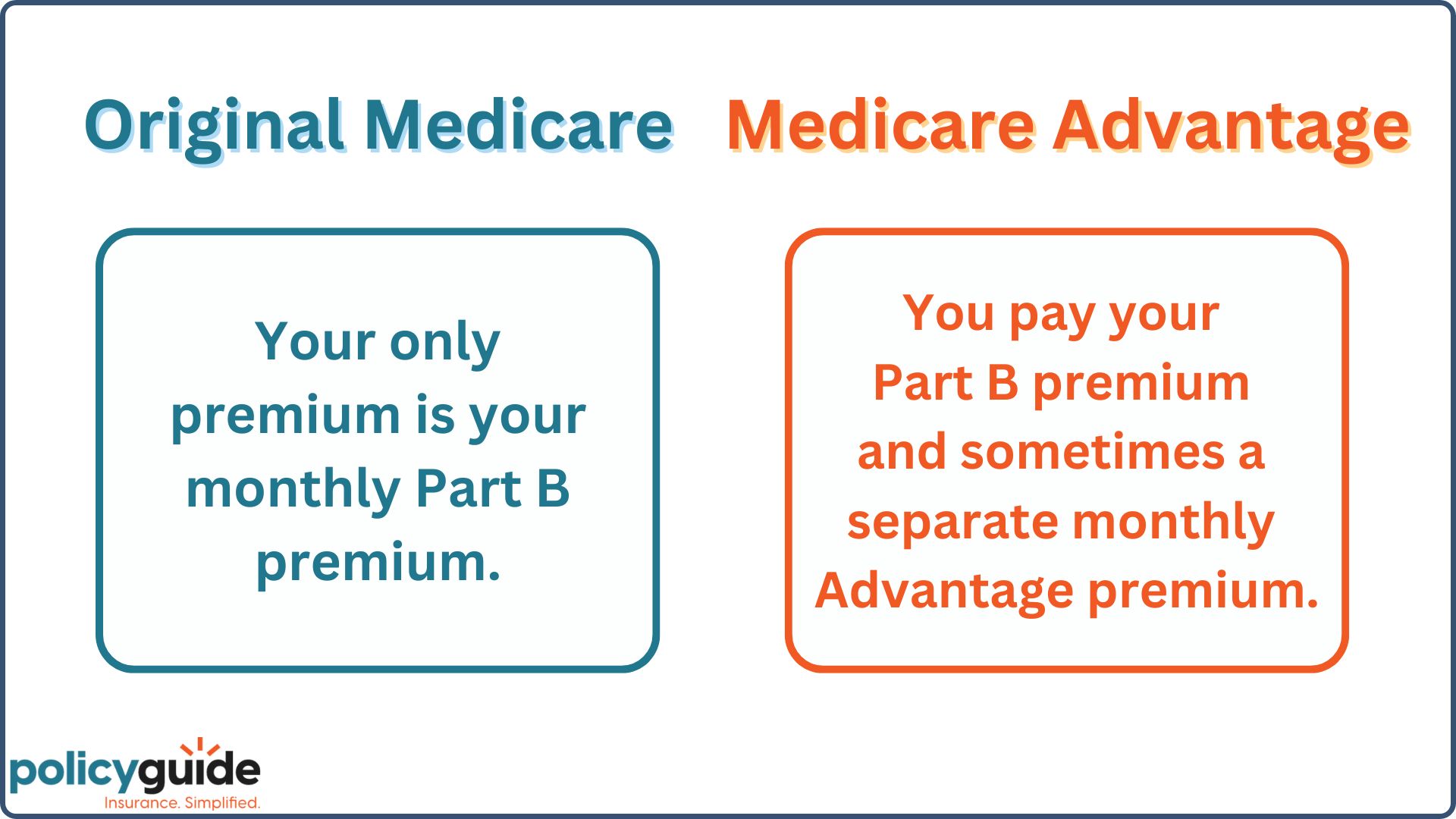

Premiums

So, right away, we know that your only Original Medicare premium is your monthly Part B premium.

If you choose a Medicare Advantage plan, you will still pay the Part B premium and sometimes a separate monthly Medicare Advantage premium.

Roughly 70% of beneficiaries nationally are enrolled in a $0 premium Medicare Advantage plan, and many of those individuals are most likely in an HMO plan.

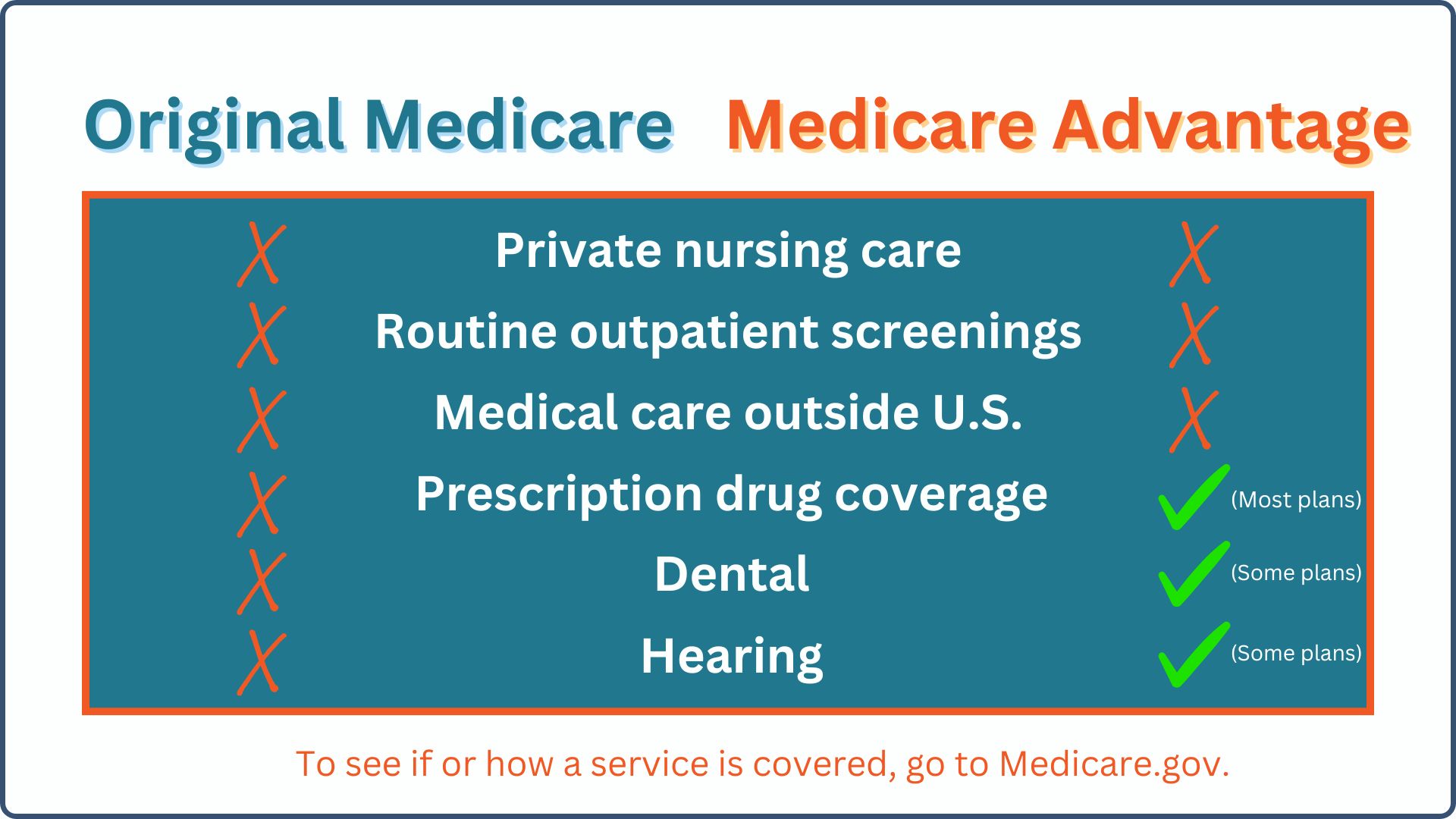

Coverage

Now, let’s look at the actual coverage between the two. These are baseline coverages of what services are covered. It won’t necessarily include the actual cost you’re responsible for.

If you go from Original Medicare to Medicare Advantage, you are not losing or giving up any benefits.

Medicare Advantage companies must pay for at least the same benefits as Original Medicare or more. They cannot offer fewer or lesser benefits than Original Medicare.

The actual services that are covered will remain consistent for:

- Outpatient care

- Emergency transportation

- Emergency room services

- Lab work and clinical services

- Diagnostic testing

- In-patient hospital care

- Hospital x-rays

- Skilled nursing facility care (with certain limitations)

- Home health services

- Durable medical equipment

- Hospice benefits (with certain limitations)

-

For more information:

I would encourage you to visit Medicare.gov to get a complete list of benefits and costs.

Now, when it comes to things like private nursing care, routine outpatient screenings, and medical care outside the US, Original Medicare and Medicare Advantage may not cover them or may be extremely limited.

One selling point in many Medicare Advantage advertisements is that most plans include prescription drug coverage, and some offer dental and hearing coverage as well.

When you have Original Medicare, you do not have prescription drug coverage. You would need to also enroll in a separate Part D drug plan.

The same would apply if you pick Original Medicare with a Medigap plan; you would also need a Part D prescription drug plan.

Final Thoughts

Here are my final thoughts: roughly half of people will choose a Medicare Advantage plan, and the other half will choose Original Medicare with Medigap.

We work with Medicare beneficiaries all over the country. After 15 years, we’ve worked with, educated, and enrolled people in thousands of different Medicare plans.

What’s right for you? We do a needs analysis to help you determine that.

You have one camp of people that like the low premium or $0 premium, plus the added dental, vision and prescription benefits that come with Medicare Advantage.

Some people prefer paying a monthly premium for a Medicare Supplement Plan G with Original Medicare because of the comprehensive coverage, far less out-of-pocket costs, no prior authorizations or referrals, and a broader selelection of doctors and hospitals.

To summarize:

- Medicare Advantage is less costly per month but can cost you more as you use it. Again, I cannot emphasize enough how critical it is to be aware of prior authorizations with Medicare Advantage. They can burn you at the wrong time.

- Medigap has a higher premium—like a Cadillac that you want to “set it and forget it”. You want to go where you want to go and do not want to deal with prior authorizations. If you want the most freedom and flexibility, that would be a Medigap plan.

If you have questions, feel free to give us a call. We would be happy to conduct a needs analysis to help you determine which avenue would be best for you. Thanks!

Source: Kaiser Family Foundation

FAQs

- Do I need a separate prescription drug plan if I have Original Medicare?

- Do I still have to pay for Original Medicare if I enroll in a Medicare Advantage plan?

- What is the difference between Medigap and Medicare Advantage?