Why Medicare Advantage Plans Are Bad: An Agents Perspective

Having worked with Medicare beneficiaries since 2010, I highly recommend that all beneficiaries choose a Medigap or Medicare Supplement plan for their rich, comprehensive benefits compared to Medicare Advantage.

However, I do understand that it’s not always an easy decision based on the cost of a Medicare Supplement premium compared to Medicare Advantage.

Hi, my name is Mark Prip. I’ve been a licensed insurance broker for 15 years. I want to show you what I have witnessed firsthand in the Medicare world. I will provide proof of what my office has experienced working with thousands of Medicare beneficiaries over the last 15 years.

I think there are seven important moving parts of a Medicare Advantage plan that affect every single beneficiary:

- Prior authorizations = denied care

- Advertising freebies

- Goverment reimbursement roller coaster

- Frequent provider disputes

- High out-of-pocket costs

- Annual plan changes

- 12-month contracts

Full disclaimer: I have both Medicare Supplement and Medicare Advantage clients.

Let’s jump right in.

-

A note about sources:

I’m going to list all sources at the bottom of this page for you to click on and view if you want – or you can take my word for what I’m referencing. I’ll always provide resource links for everything that I’m showing you.

#1. Prior Authorizations = Denied Care

#1 is a hot-button topic right now; prior authorizations = denied care.

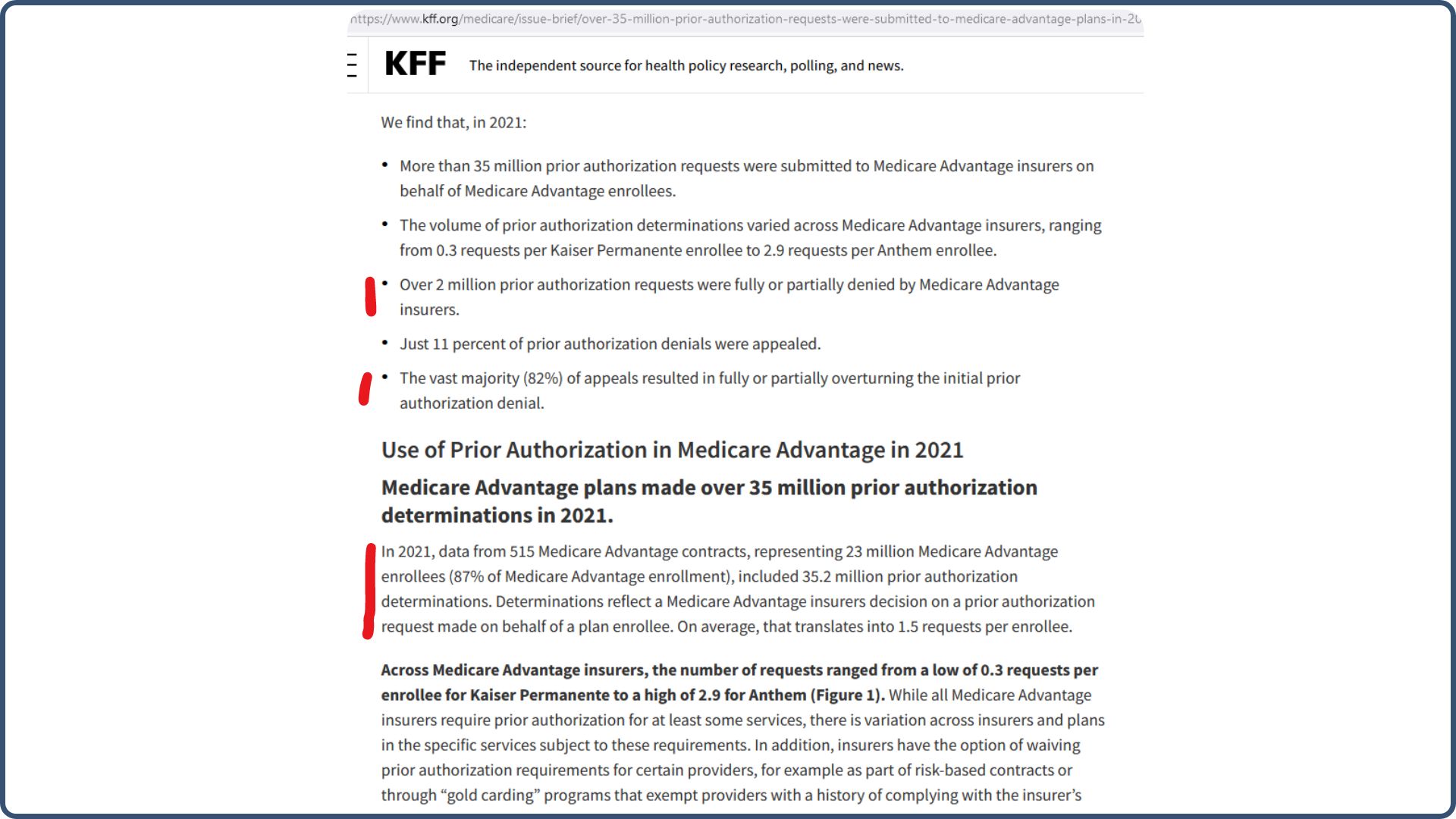

The first screenshot below is from the Kaiser Family Foundation, a very reliable source. They conduct in-depth studies on the Medicare market and provide extensive supporting evidence for their reports.

The first thing I’ve highlighted above is that over 2 million prior authorization requests were fully or partially denied by Medicare Advantage insurers, which are basically Medicare Advantage insurance companies. Only 11% of prior authorization denials were appealed.

That means more than 35 million prior authorization requests were submitted, over 2 million were denied, and just 11% of denials were appealed (fought against). On paper, that looks good, right? 35 million went through, 33 million were approved, and 2 million were rejected.

Okay, here’s the problem with that: when a prior authorization request is required, that equals delayed care and time delays; let me explain why with the below scenario:

Something happens to you. You go in the hospital. They say, okay, we figured out what’s wrong. Let’s go ahead and do this procedure.

Hit the brakes! You got a prior authorization.

So now you’re sitting in a hospital bed (or wherever you may be) waiting for that prior authorization process to go through. Even if it goes through and is approved, it means delayed care at some level.

According to Kaiser, prior authorization requests are more common among certain Medicare Advantage firms or companies. Again, most prior authorizations are approved. However, the waiting and the fact that they’re there as gatekeepers will cause time delays for you.

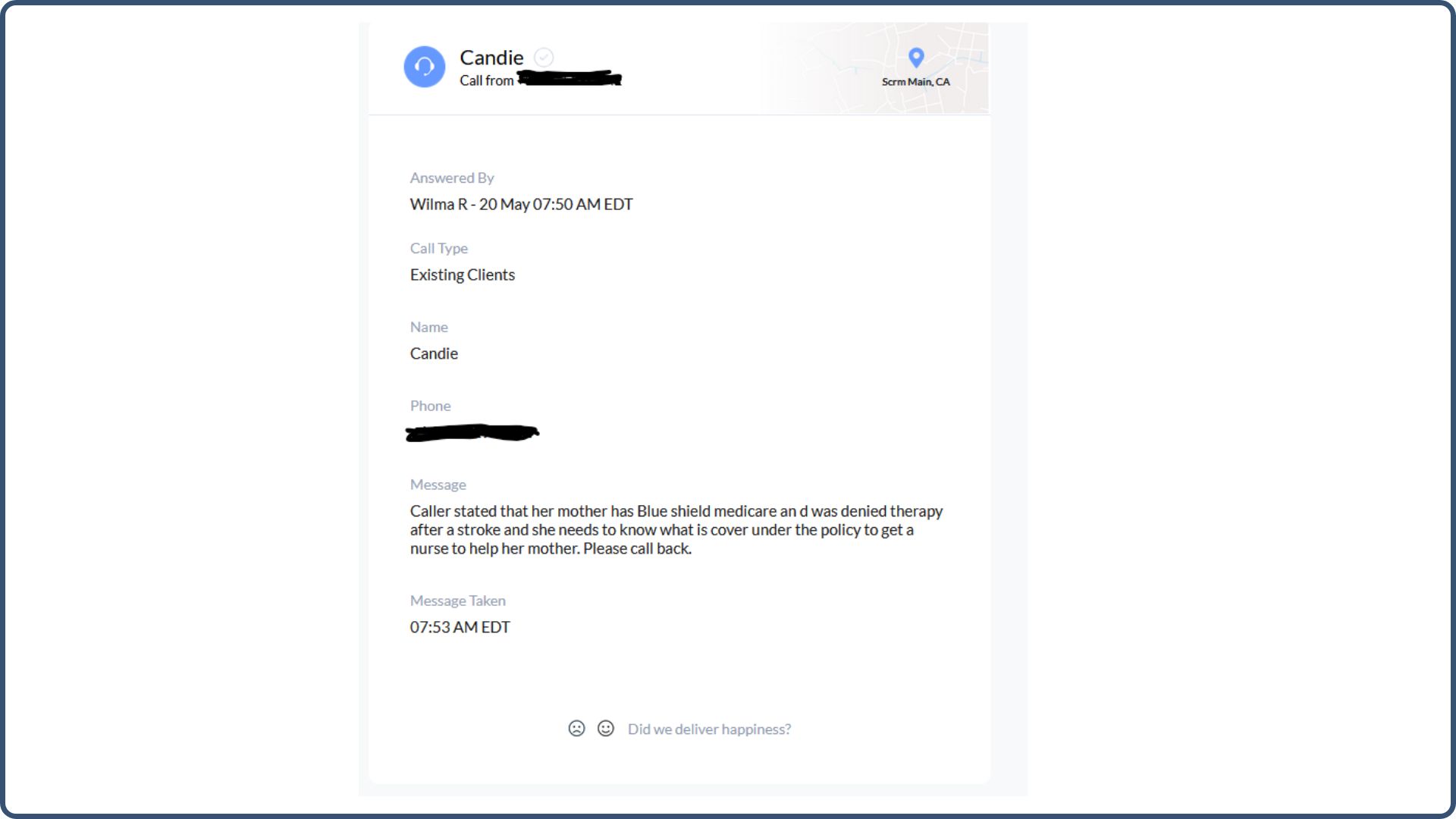

Coincidently as I was writing this article, we received this call at our office, and I wanted to share the details with you:

The caller stated that her mother has Blue Shield Medicare and was denied therapy after a stroke. She needs to know what the policy covers to get a nurse to help her mother.

It doesn’t say what Medicare plan she has, but I’m 95% certain it’s Medicare Advantage because Medicare Supplement plans do not have or require prior authorizations.

Please note I blocked out confidential information from the caller.

This call is a perfect real-life example of how prior authorizations negatively affect people. The delays and complications they cause only lead to unnecessary stress and frustration.

#2. Advertising Freebies

#2 on the list is that many Medicare Advantage companies offer their members freebie benefits that are very alluring.

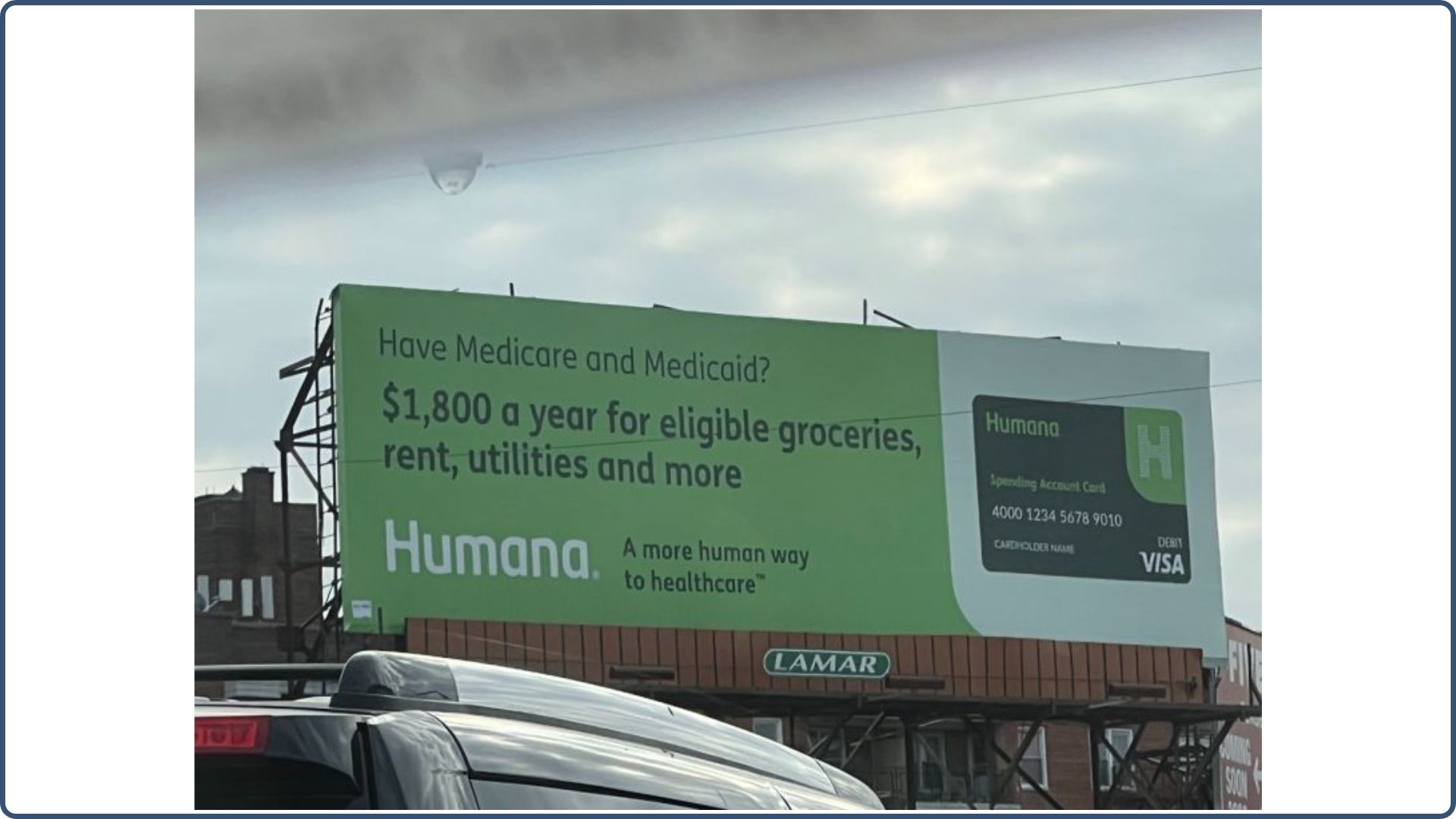

Here’s a billboard advertisement from Humana:

If you have Medicare and Medicaid, you can get up to $1,800 a year for eligible groceries, rent, utilities, and more? What’s not to love?

Don’t get me wrong. These free grocery benefits can benefit many low-income beneficiaries. However, I strongly advise: do not select a plan just because the plan offers these free ancillary benefits.

We’re trying to get people to enroll in a health insurance plan geared towards initially catastrophic coverage, which is why health insurance was developed—to prevent people from going bankrupt.

Now, people are enrolling in these plans with no idea about prior authorizations or how Medicare Advantage plans work. They’re falling for Humana’s $1,800-a-year grocery benefit.

It’s the same with Aetna’s advertisements, offering a monthly allowance on a prepaid card to pay for healthy food:

At least Aetna is trying to encourage you to take care of your health in the process.

But here’s my suggestion: be aware that these benefits will be the first ones to get cut when the plans change yearly because that’s how Medicare Advantage plans work.

Every year, they receive notice of how much the government is going to reimburse them, and then they decide what benefits they can offer or what benefits they need to take away. So, these free things will most definitely be the first things to go.

I’ve been in annual insurance company training meetings for 14 years, so I’ve seen 14 years of companies saying:

- “This year, we have a grocery allowance!”

- The following year: “well, we did away with the grocery allowance, now we’ll give you a free ride to the doctor!”

- The next year: “well, we got rid of the free doctor rides, now we’re going to give you discounts on dental!”

So these low-hanging fruit perks—I cannot emphasize this enough—do not enroll in a plan because of this. It should not be the core foundation of your medical care. It’s just a free benefit. Moving on.

#3. Government Reimbursement Roller Coaster

My third point is the government reimbursement roller coaster ride. What does that mean?

Every year, around April, Medicare releases the reimbursement rates for the upcoming year that will be paid to insurance companies for member enrollment. This decision directly affects how much these companies receive. As a result, during the Annual Election Period (October 15th – December 7th), you’ll have the chance to evaluate how these new rates impact your plan.

If the reimbursement increases, your plan typically remains unchanged. However, if it decreases, you may encounter modifications to your plan, such as higher copays or an increase in your monthly premium—from $0 to $50, for instance.

-

Open Enrollment Tip:

- You can begin to shop Medicare plans for the first two weeks in October; you just can’t enroll until October 15th.

My greatest frustration with Medicare Advantage plans is that they are filled with moving parts that no agents are talking about. The advertisements are not talking about it. Everything is about enroll, enroll, enroll for a free plan with these silly free benefits.

No one is talking about the hard reality of the elderly population getting on these plans for medical care and then being denied, kicked off, or having their network changed. The government reimbursement roller coaster is very real. And it happens every year.

Sometimes, nothing changes, which is great. Other times, your premium may go up a little bit, your co-pays could go up, or a prescription may no longer be covered or moved to a higher tier.

In the end, it’s all about money behind the scenes.

#4. Frequent Provider Disputes

Let’s move on to discuss frequent provider disputes, another moving part of a Medicare Advantage plan that can affect its members in a huge, negative way.

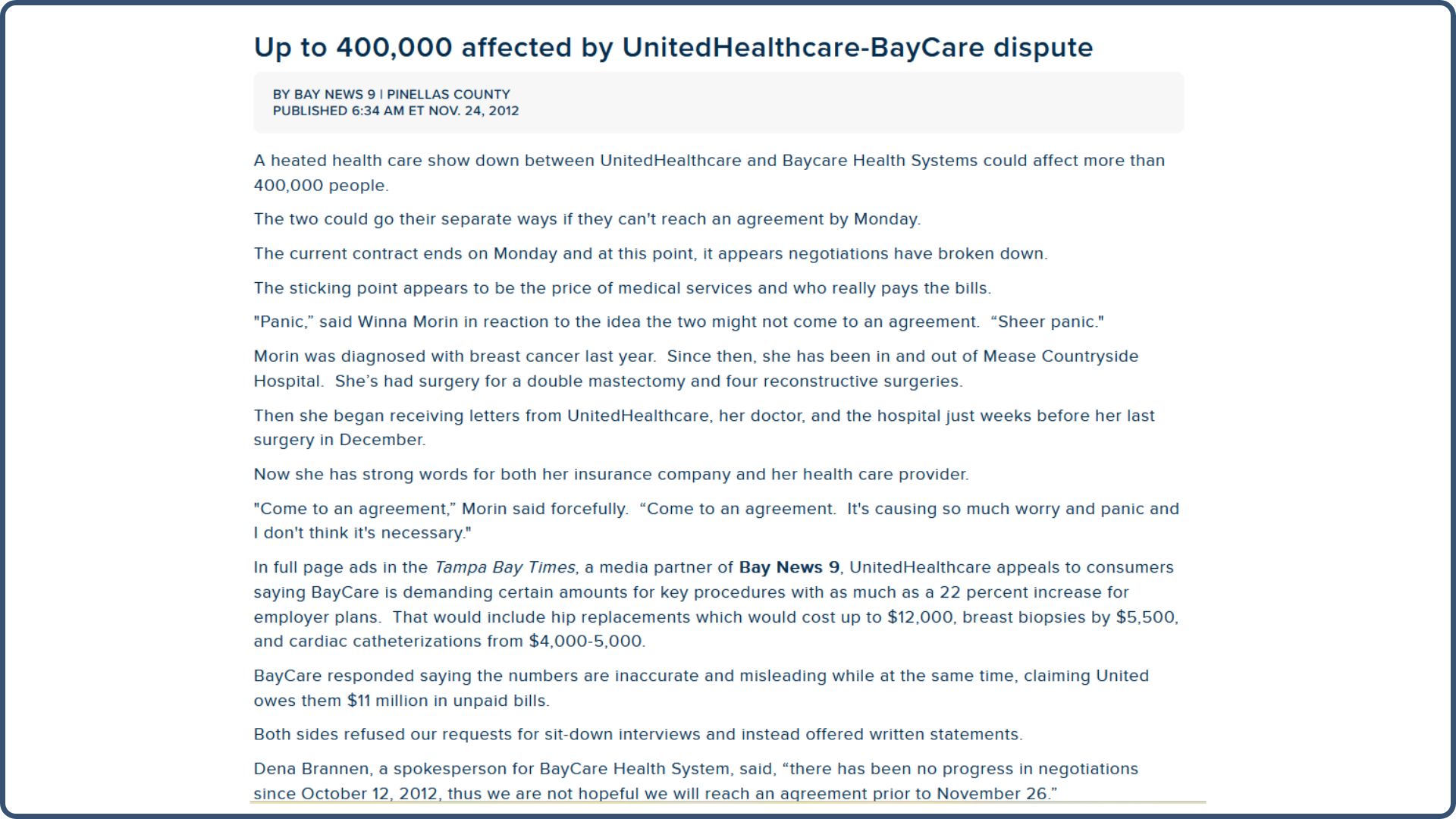

Back in 2012, we witnessed UnitedHealthcare and the BayCare system get into a claims dispute here in Florida. They sent letters to over 400,000 people saying, “We’re not going to be in network with UnitedHealthcare anymore.”

Here’s an article by Bay News 9 referencing the dispute:

“They are not paying us what they owe.” UnitedHealthcare is saying, “you’re not paying us enough”.

It becomes a tug-of-war in reimbursement money, and you, as the member, are sitting on the sidelines praying that the scheduled care you have, or all your doctors in medical care that you see in the network, will still be in network.

We moved 750 people in about three weeks from UnitedHealthcare to a Blue Cross plan, which was still a network with UnitedHealthcare.

That was the most chaotic year we’d ever seen. The phone rang 24 hours a day, with people needing to get off the UnitedHealthcare plan onto a plan that was still in the BayCare network.

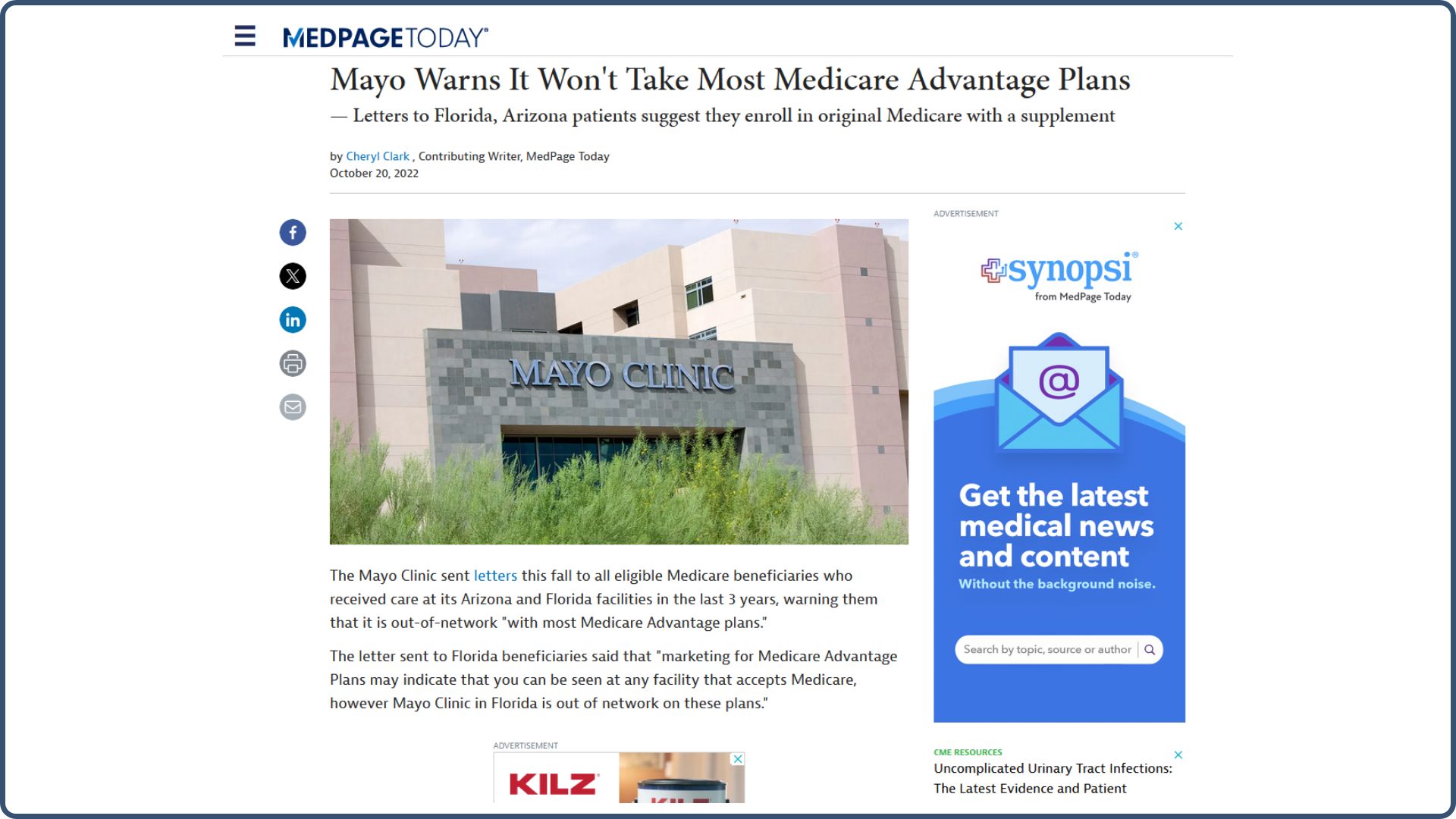

I’m going to jump forward to 2022. Below is from the Mayo Clinic. Mayo Clinic has never been fond of Medicare Advantage plans, but during the 2022 Open Enrollment Period, they sent reminder letters out to their members in Florida and Arizona to suggest they enroll in Original Medicare with a supplement:

January 2024: A Kentucky Hospital, Baptist Health, ends contracts with two more Medicare Advantage carriers (which were Humana and UnitedHealthcare):

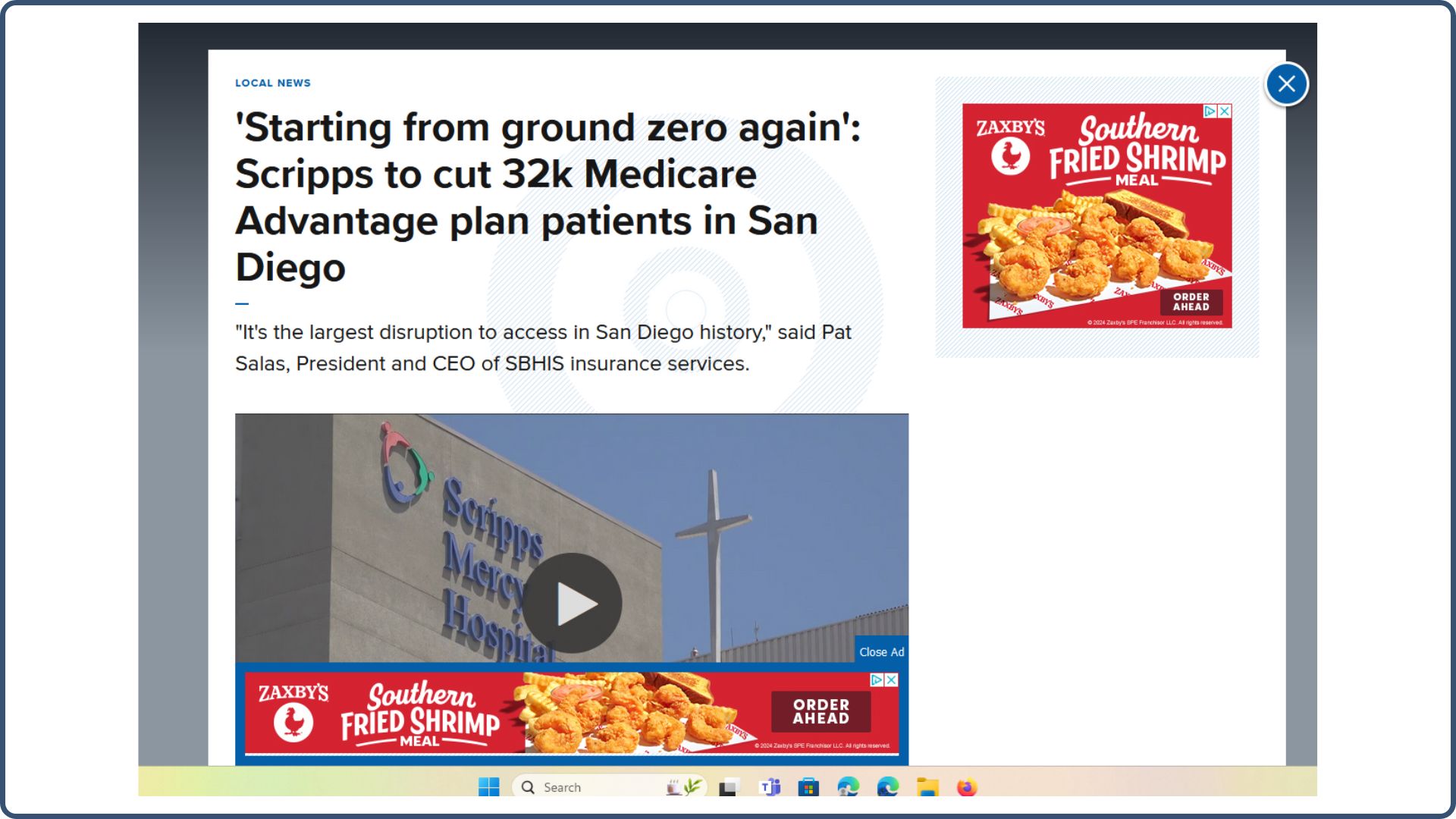

And probably the biggest news towards the end of 2023 was when Scripps Medical Group in San Diego, California, abruptly decided to stop taking all Medicare Advantage plans in all medical facilities:

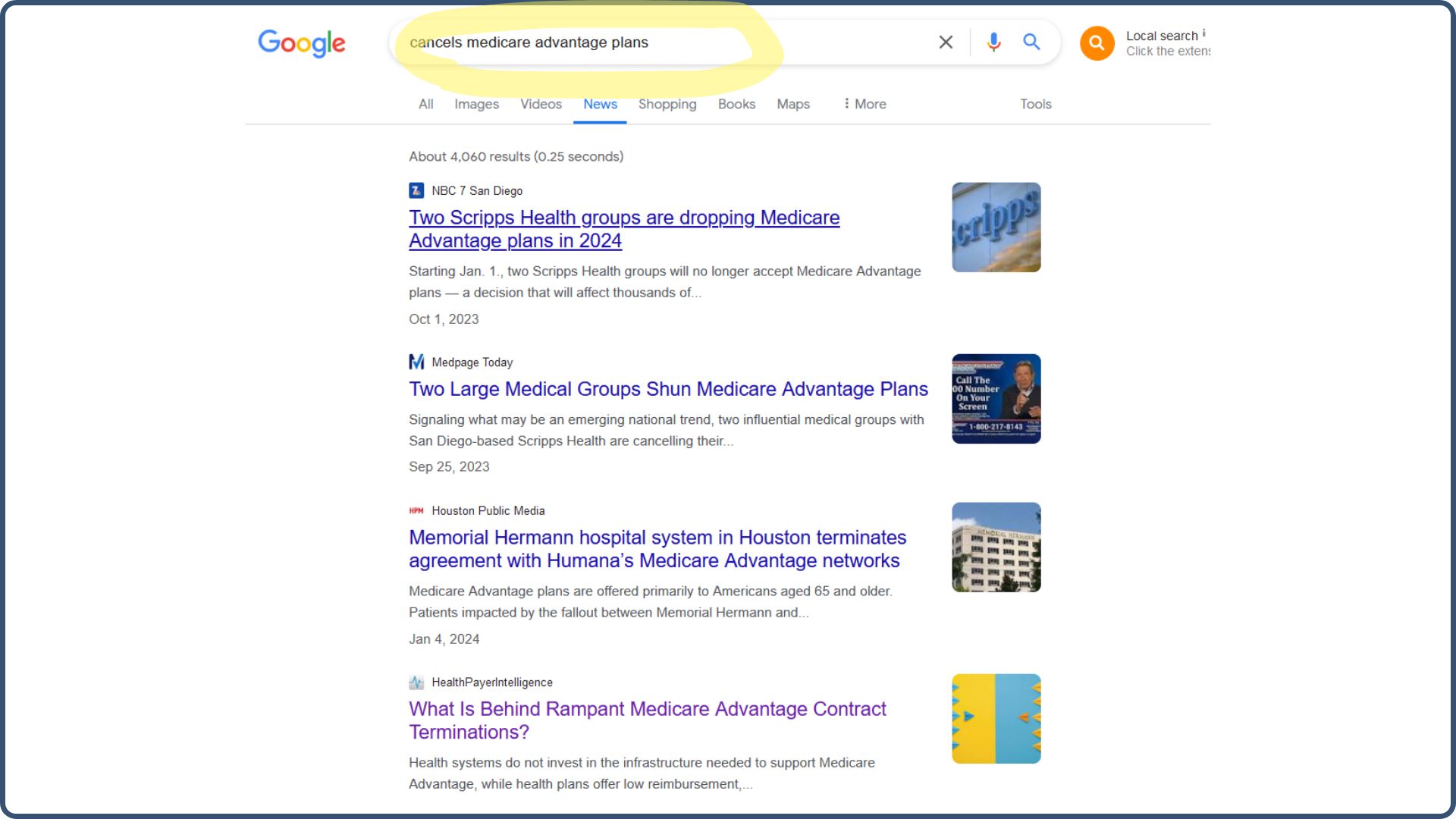

I use this example to encourage you not to take my word for it. I went to Google, typed in “cancels Medicare Advantage plans”, clicked the News tab, and here’s what you’ll get:

You’re going to see all the new headlines throughout the country. Two Scripps Health groups are dropping Advantage in California. A big, big thing.

So take some time to do that research and see what you come up with.

#5. High Out-Of-Pocket Costs

#5 on my list is high out-of-pocket costs. What does that mean to you?

No one talks about a Medicare Advantage plan having an out-of-pocket limit. These plans are sold because they’re free or low premium or have grocery benefits. What they don’t tell you about is that you have co-pays, or 20%, for many services.

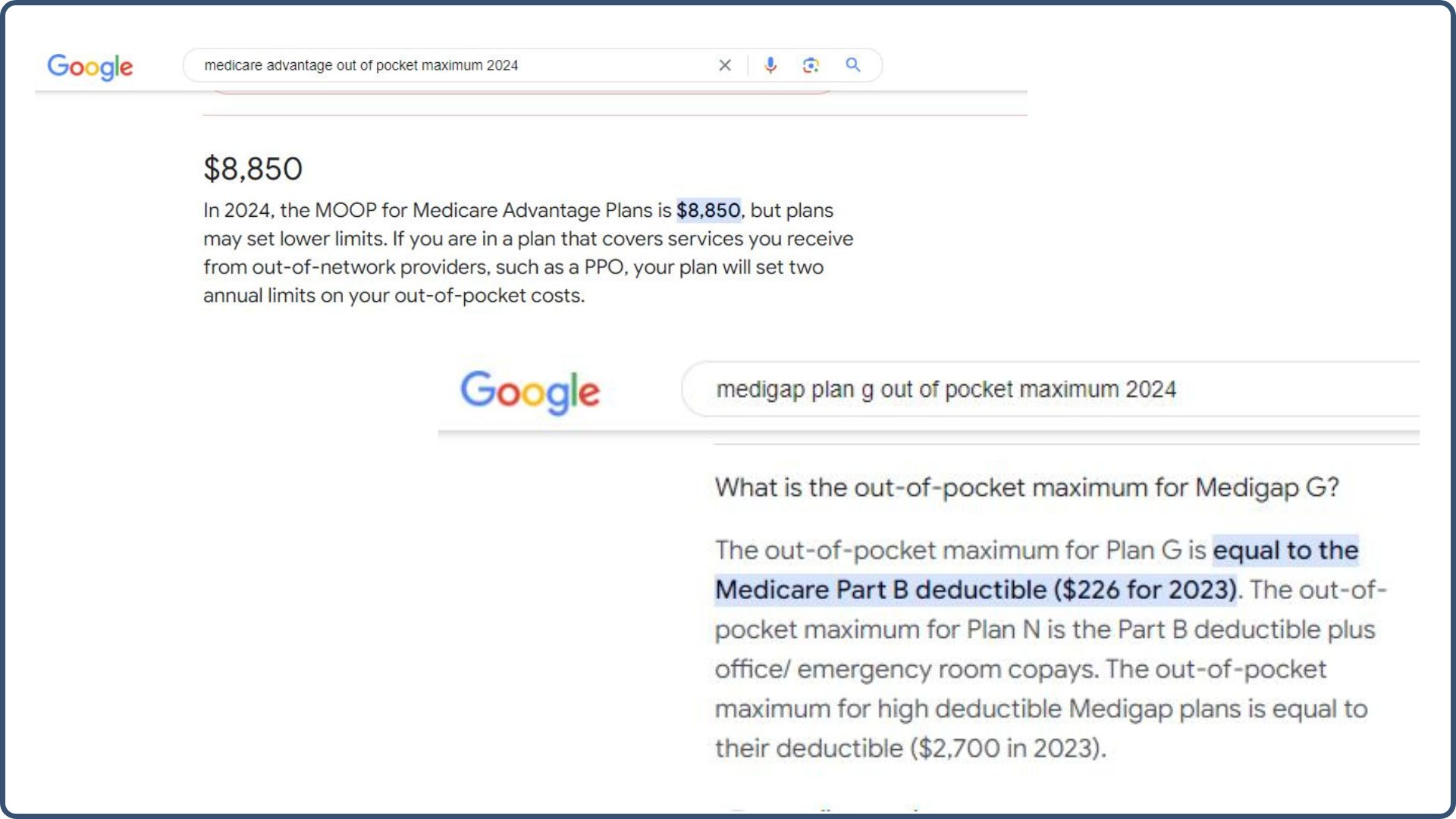

So if you have a catastrophic year, let’s say you have $200,000 in medical bills; in 2025, the maximum out-of-pocket for Medicare Advantage plans can be as high as $9,350 (that you’re responsible for).

You can always Google these out-of-pocket maximums to ensure you have accurate info:

You get there by paying your co-pays or percentages on the Advantage plan. On a Medigap plan, I took Medigap Plan G; the only out-of-pocket expense you have is your Medicare Part B deductible. The above screenshot shows the 2023 Part B deductible. It’s a little bit more now, but not much at all.

You may argue and say, “Medicare Plan G has better coverage, but it’s more expensive per month.” It is. It will cost you a monthly premium, but everything I’ve talked to up until this point will not be part of a Medigap Plan G benefit.

There are no prior authorizations, provider disputes, or government reimbursement rates. The only thing we ever talk to our Medicare Supplement clients about in ongoing reviews is rate changes. The reality is that all insurance premiums are going to go up—home, auto, boat, condo, health insurance, and life insurance—there’s no way around that.

The difference is that with a Medigap plan, you have network freedom to go anywhere Original Medicare is taken. You can travel. You can go anywhere you want in the country that takes Original Medicare Part A and B, and then the Supplement plan is automatically taken.

There are no networks unless you’re on the old select plans, which are not around very much anymore.

#6. Annual Plan Changes

I’ve touched on this before, so I won’t spend too much time here. People get on these Medicare Advantage plans and think:

“Okay, I’ve just turned 65, I got on Medicare, I picked an Advantage plan, and I’m gonna put it all in the file cabinet, and it’s all done.”

Not so fast on a Medicare Advantage plan. All the working parts that I’ve discussed—everyone is susceptible to those.

There are many moving parts behind the scenes with Advantage, and I can’t give you another example of an insurance policy with that many working components. It’s not like that with Medigap; it’s not like that with auto insurance, homeowners, dental, or vision—there’s nothing like it.

#7. 12-Month Contracts

As I mentioned previously, #7 on the list is that all Medicare Advantage plans are 12-month contracts.

Really, you’re dealing with a temporary 12-month policy with a Medicare Advantage plan because the policy goes from the Annual Election Period to the Annual Election Period.

Some people get on an Advantage plan and experience very little change, year after year. But you are still in that system and in that change process, so you do need to make sure you review.

-

Important!

- Continue to make sure your doctors are still in network, your prescriptions are still covered, your co-pays are still affordable, and your premium is still within your budget range.

Final Thoughts: Why Medigap Is the Smarter Choice (If You Can Afford It)

If you’ve made it this far, you can probably tell I have strong concerns about the structure, stability, and reliability of Medicare Advantage plans. But let’s shift gears now.

Let’s talk about the alternative.

Let’s talk about Medigap – and what makes it such a radically different experience for Medicare beneficiaries.

After walking you through the headaches and pitfalls of Advantage plans, this next part might feel… refreshingly boring. And that’s a good thing.

Medigap Isn’t Flashy – It Just Works

If Medicare Advantage is a maze of moving parts, Medigap is a straight line. There are no surprise authorizations, no doctor networks to navigate, and no fear your coverage will shift beneath your feet every year.

And here’s the thing: that simplicity is exactly why people love it.

Once you’re enrolled in a Medigap plan, especially something like Plan G, your entire Medicare experience becomes more predictable:

-

You know exactly what your out-of-pocket costs will be each year.

-

You know you can see any doctor or specialist nationwide who accepts Medicare.

-

You know that your plan isn’t going to change just because reimbursement formulas did.

There’s comfort in that kind of stability – especially when your health is on the line.

What You Pay vs. What You Get

Yes, Medigap plans come with a monthly premium – typically anywhere from $100 to $180 depending on your age, gender, and location. And I understand that not everyone can fit that into their budget.

But when you look at what you’re protecting yourself from – massive out-of-pocket maximums, surprise denials, changing networks, coverage uncertainty – that monthly premium becomes less of a burden and more of a shield.

You’re not just buying insurance.

You’re buying freedom, consistency, and peace of mind.

And unlike Advantage plans, which are funded and shaped annually based on CMS reimbursements, Medigap plans are built on a solid foundation: Original Medicare. If Medicare covers it, your Medigap plan will pick up the rest (minus your small Part B deductible on Plan G).

That’s it. No gotchas. No guesswork.

The Only Ongoing “Change” with Medigap? Premium Increases

And let’s be honest here – every type of insurance has premium increases. Home, auto, boat, business – none of them are immune. Medigap is no different. But at least you’re not dealing with:

-

Surprise co-pays

-

Annual provider network shakeups

-

Shifting formulary drug tiers

-

Lost “extra” benefits like dental or vision

Instead, your only job with a Medigap plan is to review your premium occasionally. That’s it.

For People Who Want Less Insurance Drama

What I tell clients who are trying to decide between the two options is simple:

“If you want to save money up front and are okay navigating the system every year, Medicare Advantage might work – until it doesn’t. But if you want predictable coverage, network freedom, and a system that just works when you need it, Medigap is worth every penny.”

For folks who travel, who see specialists, who don’t want to spend their retirement fighting insurance denials or researching plan changes every October – Medigap is the stress-free way to go.

Why Most People Don’t Hear About This

If you’re looking at the difference between Medicare Advantage and Medigap, I hope everything I’ve shared gave you some behind-the-scenes insight you’re not going to get from a mailer or TV ad.

When someone calls our office and says, “I’m new to Medicare; I need help finding a plan,” 99% of people are confused and unsure about what’s right for them. And frankly, I get why – it’s not a level playing field.

Medicare Advantage plans are marketed heavily because they’re more profitable for insurance companies. There’s more advertising, more perks, and more commission in it for the agent.

Medigap? Far less commission. Less advertising. And yet, for the right person, it’s the better long-term solution.

That’s why, when you work with our team, we focus on asking the right questions – not pitching the flashiest plan:

-

How often do you go to the doctor?

-

Are you okay with referrals?

-

Do you travel often or spend time out of state?

-

Are you comfortable with care limited to your county or region?

-

What medications are you on?

-

And ultimately, once we’ve laid it all out – which approach feels right to you?

That’s the difference between selling and advising.

Quick Comparison: Medigap vs. Medicare Advantage

To drive it home, here’s a side-by-side breakdown of the differences – because sometimes seeing it laid out this makes the choice even easier:

| Category | Medigap (Plan G) | Medicare Advantage (Typical PPO/HMO) |

| Monthly Premium | $100 – $180 (varies by age/location) | $0 – $50 (may be higher depending on plan) |

| Out-of-Pocket Maximum | ~$257/year (Part B deductible only) | Up to $9,350/year (2025 federal max) |

| Doctor & Hospital Access | Nationwide – any provider that accepts Medicare | Restricted to local/regional networks |

| Referrals Required? | No | Often yes (especially in HMO plans) |

| Prior Authorizations? | Never | Common for many services and procedures |

| Annual Plan Changes? | No changes to coverage once enrolled | Yes – benefits, copays, and network may change |

| Travel Coverage | Full U.S. coverage + some foreign emergency coverage | Usually limited to your service area |

| Coverage for Medicare-approved Services | 100% after Part B deductible | Copays and coinsurance apply for most services |

| Extra Perks (dental, vision, etc.) | Not included; separate plans available | Sometimes included, but not guaranteed annually |

| Plan Stability | High – same coverage year after year | Varies annually with government reimbursements |

You Deserve the Full Picture

This industry is biased toward Advantage plans – and it’s flat-out wrong. Medicare beneficiaries deserve to know all their options, not be funneled into Advantage plans based on a free perk or an eye-catching billboard.

You deserve to understand both paths clearly – so you can make the decision that works best for you.

Every agent should walk you through everything I’ve just shared every time they talk to someone about Medicare. That’s just how it should be done.

When you’re done with a call about Medicare, you should walk away feeling like a “brainiac” – smart in a simple, confident way.

If you have questions, reach out. We’re here to help however we can.

No pressure. No gimmicks. Just good, honest help for navigating Medicare the right way.

Thanks for reading – and I hope this helps you make the best decision for your Medicare journey.

If you have questions, call or email us. We’d be happy to help in any way. I hope this page helps you decide better on your Medicare journey. Thank you.

Sources

- Bloomberg Law | Kaiser Family Foundation | Bay News 9

- Medpage Today | Kentucky Lantern | KFMB San Diego

FAQs