Colonial Penn $9.95 Life Insurance Review: Buyer Beware

The Colonial Penn $9.95 life insurance plan has piqued the interest of many shoppers in the life insurance market, and it’s easy to see why:

- The company boasts a guaranteed acceptance plan at a low monthly rate.

However, there are some coverage terms and exclusions. The company imposes a “two-year limited benefit period,” meaning that your beneficiary will not collect the death benefit if your death is non-accidental and occurs within the first two years of the policy.

This means that if the death is:

- Accidental in the first two years: If the death occurs within 90 days of the accident, the insurer pays the total policy amount.

- Non-accidental in the first two years: the insurer will not pay a death benefit to your beneficiary. Instead, the designated beneficiary receives a refund of all premiums paid plus interest compounded annually.

- Any cause after the first two years: the insurer will pay the total policy amount to the beneficiary.

Hopefully, this review will help you determine whether the Colonial Pen $9.95 plan is your situation’s best life insurance plan.

-

Pro Tip:

You only need a “guaranteed acceptance life insurance policy” if you are at a higher risk of death.

Many other companies offer first-day coverage (with health questions) and do not impose a two-year limited benefit period.

What Is the Colonial Penn $9.95 Life Insurance Plan?

The Colonial Penn $9.95 plan is a guaranteed acceptance life insurance policy marketed to seniors aged 50 to 85.

Unlike traditional life insurance policies that offer a straightforward death benefit amount, this plan operates on a unit-based pricing model, which can be confusing and misleading for many consumers.

Key Features of the Colonial Penn Plan

- Guaranteed Acceptance: No medical exams or health questions are required.

- Fixed Premium Per Unit: Each unit costs $9.95 per month, but the actual death benefit varies based on the policyholder’s age and gender.

- Lifetime Coverage: As long as premiums are paid, coverage remains in effect for life.

- Limited Death Benefits: The maximum number of units that can be purchased is 15, capping the total possible payout at a relatively low amount.

- Two-Year Waiting Period: If the policyholder dies of non-accidental causes within the first two years, the insurer only refunds premiums plus interest rather than paying out the full benefit.

When you apply for Colonial Penn’s guaranteed acceptance life insurance coverage, you can request one or multiple units. The maximum allowable purchase is 15 units.

This structure makes the Colonial Penn plan significantly less valuable than many other final expense or whole-life policies. The coverage amount per unit decreases with age, making it difficult to obtain adequate financial protection without dramatically increasing premium costs.

-

Here's an example:

If one unit equals a death benefit of $1,000, the most coverage you can buy is $15,000.

In that case, at $9.95 per month per unit, your monthly premium would be $149.25 ($9.95 x 15).

Why Is the Colonial Penn $9.95 Life Insurance Plan So Popular?

The Colonial Penn $9.95 plan has gained significant popularity due to its widespread advertising, simple messaging, and appeal to seniors looking for an easy way to secure life insurance.

Here are the main reasons why this plan continues to attract buyers:

#1. Heavy Advertising and Celebrity Endorsements

Colonial Penn invests millions in national TV, radio, and online ads, often featuring well-known celebrities to build trust with their audience.

Their messaging focuses on affordability, guaranteed acceptance, and ease of enrollment, making it sound like the perfect solution for seniors who may struggle to qualify for traditional life insurance.

#2.Guaranteed Acceptance – No Medical Exam Required

One of the biggest selling points is that no medical exams or health questions are required. This is highly attractive to seniors with pre-existing health conditions who have been denied coverage elsewhere.

#3. Low Advertised Price of $9.95 Per Month

The “$9.95 per month” price point catches consumers’ attention, but many don’t realize this amount only buys one unit of coverage, which may be significantly less than they expect.

#4.Perceived Simplicity

Colonial Penn markets its plan as easy to understand, simple to enroll, and hassle-free, which appeals to seniors who may not want to deal with complex insurance policies.

However, the unit-based pricing system is actually quite complicated, making it difficult for policyholders to determine how much coverage they are really getting.

#5.Appeal to Seniors Who Fear Leaving Loved Ones with Expenses

Many seniors worry about burdening their families with funeral and burial costs, and Colonial Penn’s marketing plays into this concern.

While it does provide some coverage, the low payout amounts often fall short of covering full final expenses, leading families to cover the remaining costs themselves.

#6.Availability for Seniors Aged 50-85

Many traditional life insurance policies become difficult or impossible to obtain past a certain age, making Colonial Penn’s acceptance range (50-85) attractive to older applicants.

While the Colonial Penn plan is very popular, we don’t believe that its actual value matches the marketing hype.

Problems With the Colonial Penn $9.95 Plan

Let’s look at some problems we believe are important to know about the Colonial Penn $9.95 plan.

The Two-Year Waiting Period – A Major Drawback

The two-year limited death benefit period is one of the most significant issues with Colonial Penn’s $9.95 plan. If a policyholder passes away due to natural causes within the first two years, their beneficiary will not receive the full death benefit.

Instead, they will only be refunded the premiums paid plus a small interest. This policy detail is often buried in the fine print, leaving many buyers unaware of the true risks until it’s too late.

Real Life Scenario:

Imagine a 72-year-old widow, Margaret, who signed up for Colonial Penn’s plan, believing it would ensure her children wouldn’t be burdened with funeral costs. Tragically, she passed away from a heart attack just 18 months after purchasing the policy.

Instead of receiving the expected $10,000 in benefits, her children were left with only a refund of the premiums she had paid—amounting to roughly $179.

The family, still grieving, now faced the overwhelming task of gathering thousands of dollars to cover funeral expenses, burial costs, and unpaid medical bills. With limited savings, they were forced to take out loans and rely on crowdfunding.

Had Margaret chosen a competitor offering immediate coverage, her family could have avoided this unnecessary financial hardship.

Many reputable life insurance companies offer first-day coverage, meaning beneficiaries receive the full death benefit immediately, regardless of how soon after purchasing the policy the insured passes away.

However, with Colonial Penn’s plan, seniors are essentially paying for a policy that may not provide coverage when their family needs it most.

Misleading Pricing – The $9.95 Per Month Gimmick

At a glance, low-rate guaranteed acceptance life insurance sounds appealing, but a closer look reveals the fine print.

As advertised, it is not readily apparent that the $9.95 price tag is a starting price.

Unlike traditional life insurance, where a set monthly premium guarantees a specific payout, Colonial Penn life insurance pricing is based on the purchase of “units.” A unit represents a specific amount of coverage or benefit. Pricing on these units varies by age, gender, and state of residence.

Because of this unit-based pricing model, policyholders must buy multiple units to get meaningful coverage, often leading to monthly premiums of $100 or more—a far cry from the advertised $9.95.

For example, let’s say you are a 63-year-old male who wants to leave $10,000 to your beneficiary.

If the $9.95 monthly premium buys you a $1,000 death benefit (one unit), you will buy ten units ($1,000 x 10 = $10,000) and pay a monthly premium of $99.50 ($9.95 x 10).

You can see where the $9.95 advertised premium is quickly irrelevant.

Real-Life Scenario:

Take, for example, John, a 72-year-old retiree who wanted to leave enough money to cover his funeral expenses and a small legacy for his grandchildren. Seeing Colonial Penn’s $9.95 commercials, he believed he could secure meaningful coverage for under $50 per month.

However, John only later realized that his $50 per month only got him around $3,000 in coverage. When he passed away unexpectedly, his family was left scrambling to come up with the remaining $8,000 needed for his funeral.

His daughter, Lisa, had to take out a high-interest loan to cover burial expenses, a situation that could have been avoided had John chosen a policy with transparent pricing and a higher benefit payout.

Other insurance providers, such as Mutual of Omaha and Aetna, offer simplified issue whole life insurance with straightforward pricing and higher coverage amounts.

A policyholder can pay a similar premium and receive a much larger death benefit without the confusion of unit pricing.

Low Coverage Amounts – Insufficient for Funeral Expenses

The Colonial Penn plan caps coverage at 15 units, which means the maximum possible payout is around $15,000 or less, depending on age and gender.

With today’s funeral costs averaging $7,000 to $12,000, this plan may not provide enough financial relief for beneficiaries.

Real-Life Scenario:

Consider the case of Mary, a 78-year-old woman who purchased Colonial Penn’s policy, hoping it would cover all her final expenses. She believed that 15 units would be enough.

However, when she passed away, her family was shocked to learn that the total payout was only $11,000—far short of the $15,000 she expected and significantly below the $14,500 cost of her funeral, burial, and outstanding medical bills.

Her children, already grieving, had to scrape together an additional$3,500to cover the costs. This led to financial strain, forcing one to take out a personal loan, adding more stress during an already difficult time.

Other life insurance providers offer higher maximum coverage limits, ensuring that families are not left with unpaid expenses.

For example, Mutual of Omaha’s Whole Life Insurance offers coverage up to $50,000 and clear, easy-to-understand pricing, and Aetna’s Final Expense Policy provides higher coverage amounts with first-day benefits, eliminating the risk of being underinsured.

Customer Complaints – A Huge Red Flag

According to the Better Business Bureau website, Colonial Penn has a history of delayed claim payouts, poor customer service, and misleading sales tactics.

Many policyholders or their beneficiaries report long waiting periods when trying to receive benefits, often during times of emotional and financial distress.

Let’s look at some examples from real customers.

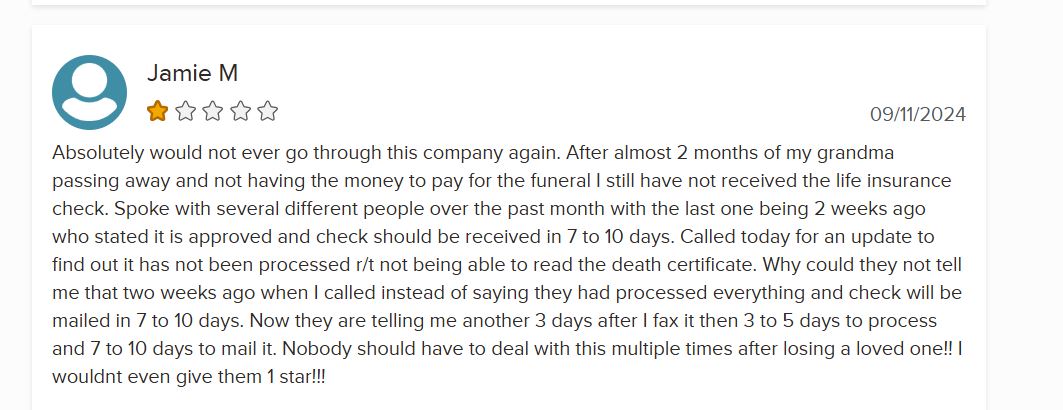

Long Delays and Poor Communication

Example: Jamie M. (1-Star Review)

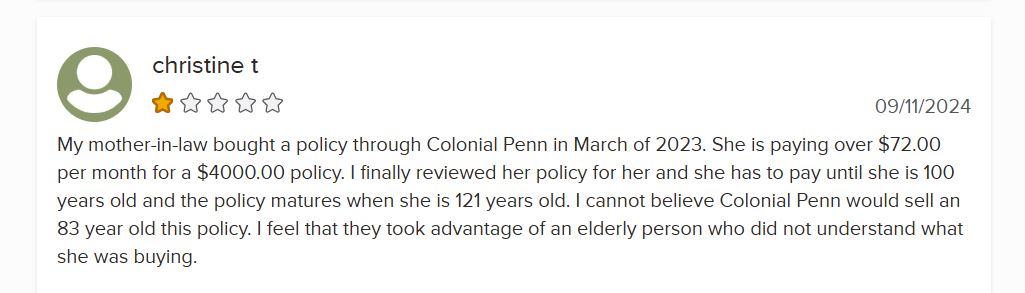

Overpriced Policies with Misleading Terms

Example: Christine T. (1-Star Review)

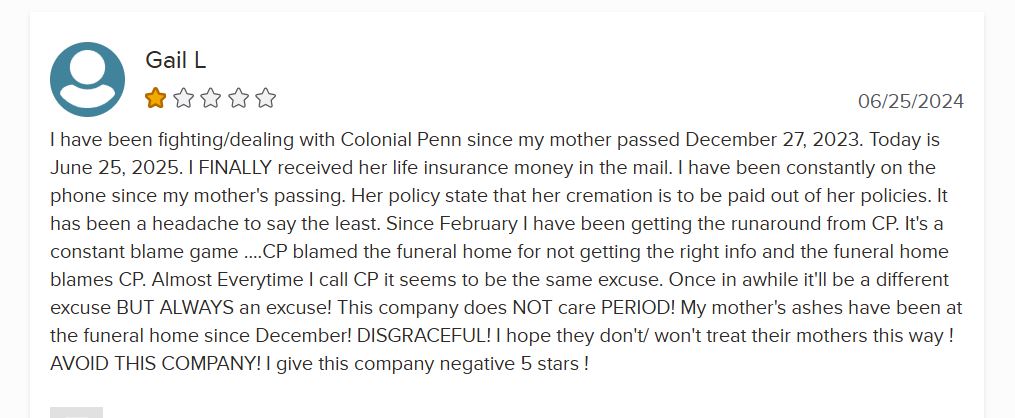

Endless Runarounds and Claim Delays

Example: Gail L. (1-Star Review)

In a nutshell, Families have raised concerns about long payout delays, inconsistent explanations, and confusing policy terms, leaving many frustrated with the process. Seniors, in particular, report unknowingly committing to policies with limited benefits.

How Much Do Colonial Penn Units Cost?

Colonial Penn sells units, which are predetermined increments of benefit instead of a fixed dollar amount on the policy.

The policyholder can decide on the number of units to buy depending on the coverage they need. Your age and gender will determine how much death benefit is provided per unit.

Check out the table below to see the death benefit amount paid for each unit you purchase.

| Age | 1 Male Unit ($9.95) | 1 Female Unit ($9.95) | Max Coverage (15 Units) |

| 50 | $1,669 | $2,000 | $30,000 |

| 60 | $1,167 | $1,515 | $17,505 |

| 70 | $689 | $1,000 | $10,335 |

| 75 | $549 | $762 | $8,235 |

| 80 | $426 | $608 | $6,390 |

| 85 | $418 | $468 | $6,270 |

For example, a 65-year-old male purchasing one unit of coverage can expect an $896 payout from that unit to his beneficiary.

In comparison, a 65-year-old female purchasing one unit can expect a payout of $1,258 from that unit.

Why the Unit System Can Be Misleading

As you can see, the advertised low rate may seem attractive, but if you would like a higher level of coverage, you will need to purchase the corresponding number of units and increase your monthly premium by that amount.

Most policyholders need multiple units to reach a reasonable death benefit, which drives up their premiums far beyond the advertised $9.95 rate.

For comparison, competitors’ final expense life insurance policies offer $10,000 to $25,000 in coverage for a similar monthly cost, often with full benefits on the first day and no waiting period.

Real-Life Scenario:

Harold is a 73-year-old retiree. He saw Colonial Penn’s TV ads and assumed he could get $10,000 in life insurance for $9.95 per month.

However, after purchasing the plan, he learned that each unit only provided coverage for $608 for his age group.

To get the $10,000 he needed, Harold had to buy 15 units, which cost him $149.25 per month—far more than he expected.

Unfortunately, when Harold passed away just a year later, his family only received a refund of the premiums paid plus interest due to the two-year waiting period. His wife was forced to take out a loan to cover his funeral expenses.

Pros and Cons of the $9.95 Plan

Let’s summarize the pros and cons of the Colonial Penn $9.95 life insurance plan.

-

Pros:

- There is no prerequisite medical exam, and the insurance carrier will not ask you health questions.

- Once coverage begins, health conditions do not impact your monthly rate or death benefit.

- Premiums do not increase with age (as long as you stay current on premium payments without interruption).

- The application process is simple: download and submit a one-page, seven-question enrollment form.

-

Cons:

- The $9.95 monthly premium advertised is only a starting price.

- Customer complaints on the BBB site indicate poor customer service.

- A two-year waiting period applies before benefits kick in unless you meet the criteria for accidental death.

- In most states, the policy is only available to applicants aged 50 to 85.

When weighing Colonial Penn’s guaranteed acceptance insurance’s pros and cons, it becomes clear that research is critical.

Other life insurance companies may offer coverage with no waiting period, a straightforward pricing approach, and better overall value.

Note:

Suppose your priority is easing the financial burden on your family by finding coverage for funeral costs and other final expenses.

In that case, you may want to explore final expense life insurance (also known as burial insurance).

Better Alternatives: Mutual of Omaha, Cigna and Aetna

If you’re looking for a better alternative to Colonial Penn, several life insurance providers offer higher coverage amounts, transparent pricing, and first-day benefits.

Let’s talk about the best options.

Colonial Penn vs. Mutual of Omaha

Mutual of Omaha, a trusted name in the insurance industry for over 100 years, provides straightforward, comprehensive policies with no waiting period, competitive pricing, and higher coverage amounts, making it an excellent choice for seniors seeking reliable protection.

Their final expense insurance is particularly noteworthy, with coverage amounts ranging from $10,000 to $50,000. This flexibility is ideal for funeral costs, outstanding debts, or leaving a legacy. Additionally, Mutual of Omaha is known for transparent pricing, high customer satisfaction, and financial stability, earning an A+ rating from A.M. Best.

Unlike Colonial Penn, Mutual of Omaha’s policies come with several key benefits, including immediate coverage for most applicants. This ensures families are not left financially vulnerable in the critical first years of coverage.

The company also offers a variety of riders to enhance coverage, such as a Chronic Illness Rider and a Terminal Illness Rider, which provide added flexibility.

Mutual of Omaha’s Key Offerings:

- Immediate Coverage: Most applicants qualify for coverage without a waiting period.

- Flexible Coverage Limits: Higher limits (up to $50,000).

- Competitive Pricing: Sample premiums include $47/month for $10,000 coverage for a 65-year-old female and $140/month for $25,000 coverage for a 65-year-old male.

- Customer-Centric Riders: Options like chronic illness and terminal illness riders enhance the value of policies.

Real-Life Scenario:

David, a 65-year-old retiree, purchases a $25,000 final expense policy from Mutual of Omaha to cover his funeral expenses and leave a small legacy for his grandchildren.

Tragically, three months after his policy takes effect, David passes away unexpectedly due to a heart attack.

Since Mutual of Omaha’s policies have no waiting period for most applicants, David’s family receives the full $25,000 death benefit immediately. This allows them to pay for his funeral and settle the remaining medical bills without financial strain.

If David had purchased Colonial Penn’s $9.95 policy, his family would not have received the full benefit due to the mandatory two-year waiting period for non-accidental deaths.

Instead, they would have only received a refund of the premiums he paid plus a small amount of interest, leaving them struggling to cover his funeral costs.

Colonial Penn vs. Aetna

Aetna’s simplified issue of whole-life policies requires no medical exam, allowing applicants to qualify by answering a brief health questionnaire. This process ensures a straightforward path to coverage for individuals with conditions such as diabetes or COPD who might struggle to secure insurance elsewhere.

With coverage up to $25,000, Aetna’s plans provide sufficient support for final expenses, such as funeral costs, outstanding debts, or small financial legacies.

Furthermore, Aetna’s commitment to affordability is evident in its competitive pricing. For instance, a 65-year-old male pays $77 per month for $10,000 in coverage, while a female of the same age pays $62 monthly for an equivalent policy.

Aetna’s Key Offerings:

- No Medical Exam: Simplified application process with just a health questionnaire.

- Immediate Coverage: Once approved, applicants are covered without delays.

- Affordable Premiums: A 65-year-old male pays $77/month for $10,000 coverage, and a female pays $62/month.

- Reliable Insurer: Strong financial stability (A rating from A.M. Best) and a commitment to high-risk applicants.

Real-Life Scenario:

Diane, a 72-year-old retiree, wants to ensure her family isn’t burdened with the costs of her funeral and other final expenses. She chooses Aetna’s final expense policy, which offers a coverage amount of $25,000, the maximum.

Diane likes that she doesn’t have to undergo a medical exam and that the application process is straightforward. She feels confident knowing the policy provides enough to cover her needs.

When Diane passes away four years later, her family uses the $25,000 death benefit to cover the $10,000 cost of her funeral and burial, settle $5,000 in remaining medical bills, and put $10,000 into a savings account for her granddaughter’s college education.

If Diane had opted for Colonial Penn, the maximum coverage she could have purchased would have been $15,000, which might have been insufficient for her expenses.

The unclear unit pricing structure also might have confused during the application process, making it harder for Diane to plan effectively.

Colonial Penn vs. Cigna

Designed for individuals aged 50 to 85, Cigna’s whole life insurance policies provide straightforward benefits with lifetime coverage and consistent premium rates, making it easier for policyholders to budget effectively.

Cigna policies offer coverage amounts ranging from $2,000 to $25,000, which can cover funeral costs, outstanding debts, or even small financial legacies. Unlike Colonial Penn, where benefits are determined by units that vary based on age and gender, Cigna provides predictable coverage with clear terms.

Additionally, policyholders benefit from a cash value component that grows over time and can be accessed through loans or withdrawals, adding financial flexibility. They are also known for their customer-first approach, boasting a very low complaint ratio and an A rating from A.M. Best.

Cigna’s Key Offerings:

- Fixed Premiums: The monthly costs remain constant throughout the policy’s life, making it easier for seniors on a fixed income to budget.

- Cash Value Growth: Policies accumulate value over time, which policyholders can access through loans or withdrawals.

- Affordable Coverage: For a 65-year-old male, a $10,000 policy is $85/month, while a $25,000 is $197/month.

- Rider Options: Includes a Terminal Illness Accelerated Benefit Rider, allowing access to a portion of the death benefit in dire circumstances.

Real-Life Scenario:

Roger, a 68-year-old widower, is looking for a straightforward life insurance policy to cover his funeral expenses. He appreciates that Cigna clearly outlines its whole life policy terms: premiums are fixed, the coverage amount ranges from $2,000 to $25,000, and policies include a cash value component.

There are no hidden fees or confusing pricing systems. Roger chooses a $15,000 policy with a fixed premium of $85/month, confident that he knows exactly what he’s paying for and what his family will receive.

When Roger passed away six years later, his family filed a claim and promptly received the $15,000 death benefit without any confusion or delays. Because Roger was fully aware of the policy’s terms, he was able to prepare his family for what to expect financially.

If Roger had chosen Colonial Penn, he might have been misled by the $9.95-per-unit pricing. The actual coverage amount per unit depends on age and gender, and at 68, Roger may have only received around $1,000 per unit. Roger’s family could have been surprised by the limited payout without clear explanations.

In summary, here is a chart showing how Colonial Penn stacks up against these other leading providers.

| Feature | Mutual of Omaha | Aetna | Cigna | Colonial Penn |

| Max Coverage | Up to $50,000 | Up to $25,000 | Up to $25,000 | Up to $15,000 (units) |

| Waiting Period | None | None | None | 2 years (non-accidental) |

| Medical Exam | No | No | No | No |

| Cash Value | Yes | Yes | Yes | No |

| Sample Premium (65 y/o Male) | $59/month for $10K | $77/month for $10K | $85/month for $10K | $9.95/unit (coverage varies) |

| Transparency | High | High | High | Low |

| Customer Satisfaction | Excellent | Good | Excellent | Poor |

Bottom Line

After weighing Colonial Penn’s guaranteed acceptance insurance’s pros and cons, it pays to shop for better value elsewhere.

Colonial Penn’s $9.95 life insurance plan may be appealing as you research your options, but several drawbacks make it less attractive than other products.

The two-year waiting period for non-accidental death benefits and customer complaints regarding poor service should give potential customers pause when considering this policy.

You may consider contacting one of our licensed insurance agents, who can help you explore other options and insurance carriers. We are here to help.

Sources: The Annuity Expert | Final Expense Direct

FAQs

- What is the death benefit on the Colonial Penn $9.95 Plan?

- What is a "unit" with the Colonial Penn $9.95 Plan?