Best Medicare Supplement Companies - 2025

If you’re looking for the biggest and most well-known Medicare Supplement insurance provider, you should pick UnitedHealthcare.

Although UnitedHealthcare is one of the biggest Medicare Supplement companies, it is not always the cheapest.

If you’re looking for the cheapest Medigap premiums, consider newer companies like Allstate and ACE. These companies recently entered the market with very competitive rates on Plan G and Plan N.

My name is Mark Prip, and I’ve been teaching people about Medicare for over 15 years. Today, I will share with you what I have learned about picking the best Medicare Supplement insurance company.

Here’s what I’ll cover in this article:

- Biggest Medigap companies

- A discussion on rate increase history

- Cheapest Medigap companies

- Medigap benefits

- Most popular plan options + comparison tips

- Average Medigap rates

- How to avoid getting overwhelmed

Tip: Comparing Medigap plans (or Medicare Supplement plans) and companies is far easier than you think because of their simple, straightforward benefits, and I’ll show you why in this article.

Let’s jump right in.

With all the insurance companies pushing Medicare Advantage plans, I want to first congratulate you on looking at a superior option that Medigap plans provide.

Let’s start with the largest Medigap companies.

What Are the Largest Medicare Supplement Companies?

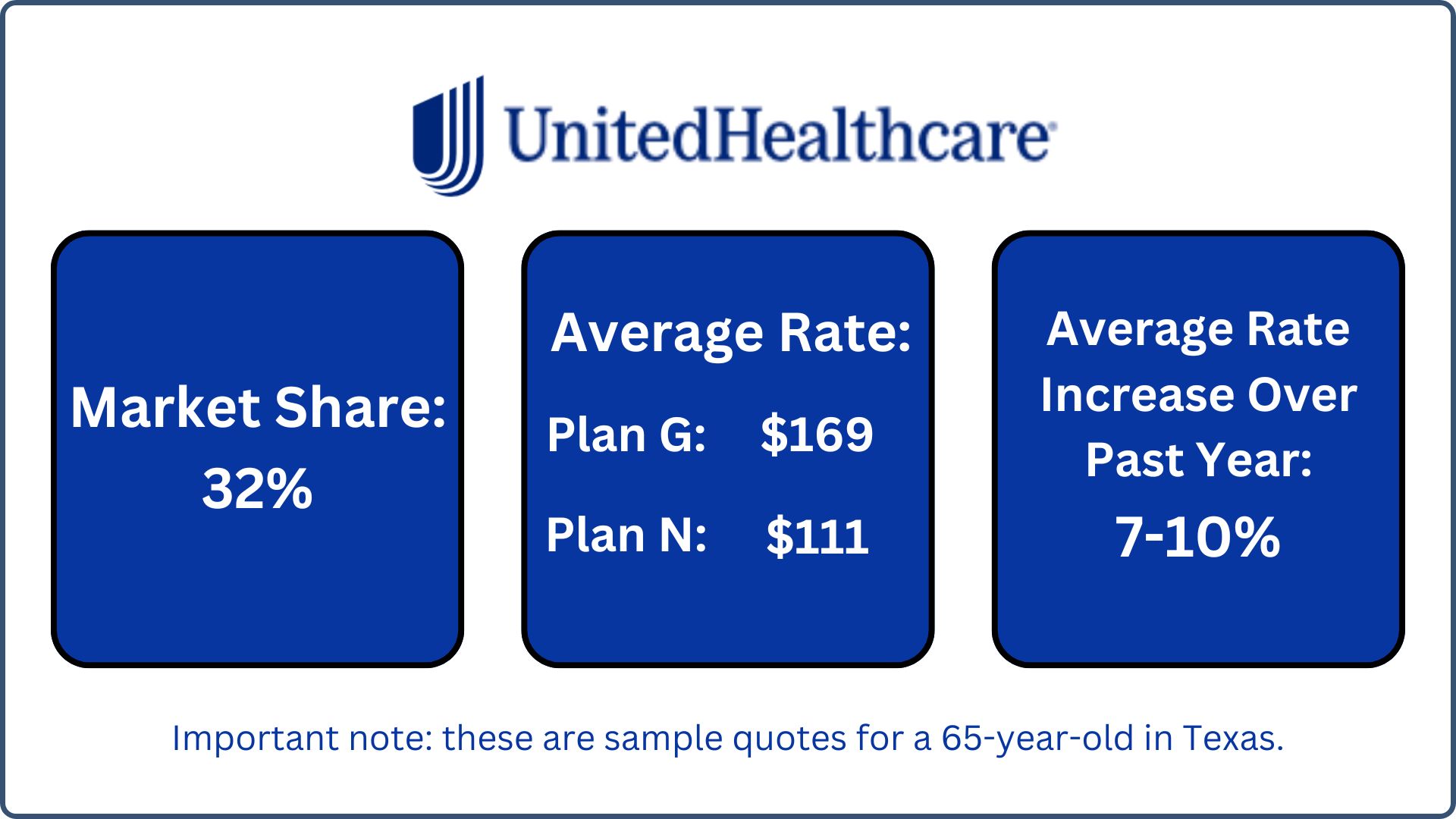

Starting first on the list is UnitedHealthcare (UHC).

#1. United Healthcare

UHC has a market share of 32%, and the average rate for Plan G is $169. Plan N’s average is $111. I used these sample quotes for a 65-year-old in Texas.

UnitedHealthcare has had an average rate increase of 7% to 10% over the past year, depending on where you are in the country.

UnitedHealthcare gives you the option to include a Renew Active health program, and they also have additional dental, vision, and hearing discounts.

Their rates are most competetive in these states:

- Florida

- Michigan

- California

- Illinois

- Arizona

UHC is a reliable and established company that has been in the Medicare market longer than most other companies combined.

Now, let me pause just a moment and discuss a very popular topic when it comes to comparing companies.

Everyone wants to know:

- #1. What is their starting rate

- #2. How to project future rate increases

- #3. Which companies are more favorable

Let’s take a deeper look at that subject.

Rate Increases

Medigap companies have consistent rate increases, so it’s important to look for a company with a lower rate increase percentage. The market average was roughly 4% every year from 2001 to 2010 (that’s a very old report).

Post-COVID, we are seeing rate increases from 7 to 10%, a significant jump.

This is partly due to people delaying care during COVID-19 quarantine. After quarantine ended, everyone returned to get the non-urgent medical care they needed. Hopefully, this should balance back out in time.

Basically, with COVID, everyone withheld from nonemergency needed care.

Once quarantine ended and life got back to normal, people went back to get the care that they had postponed that was nonemergency.

So, there was an influx of claims that came after the quarantine and after COVID died down.

I’m going to continue with all of the other companies, but you’ll see a very consistent trend with the other larger Medicare Supplement companies.

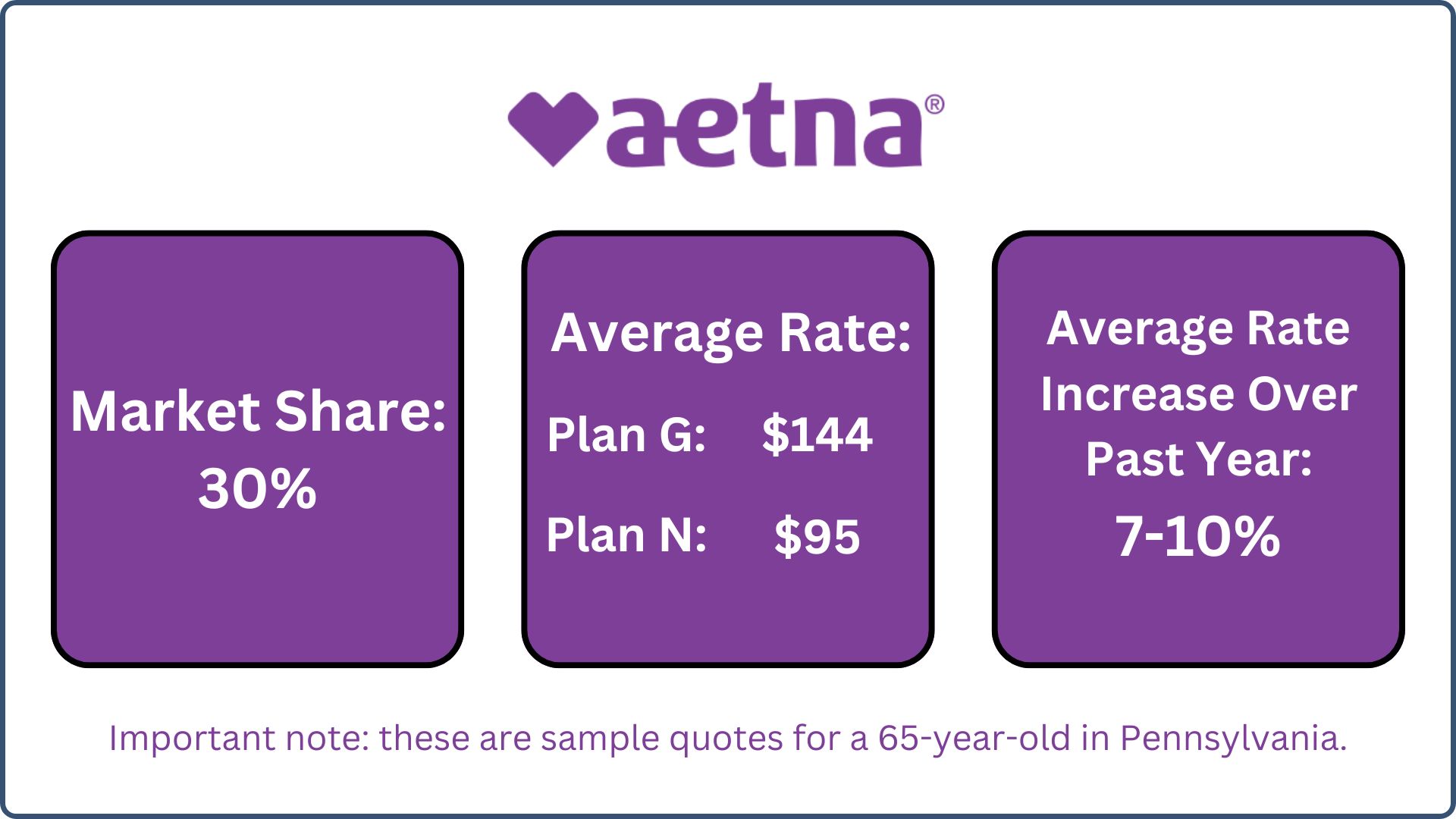

#2. Aetna

The second runner-up is Aetna.

Aetna has a market share amongst all of their affiliate names and brands of 30%.

Average rates for Plan G is $144, and Plan N is $95. These are sample rates I ran for a 65-year-old in the state of Pennsylvania.

We have personally seen an average rate increase over the past year of 7% to 10% (not much different than UnitedHealthcare).

Aetna offers seven standardized plans and up to a 7% household discount on the monthly premiums if you qualify.

They also have very strong optional dental and hearing policies that we have really come to love.

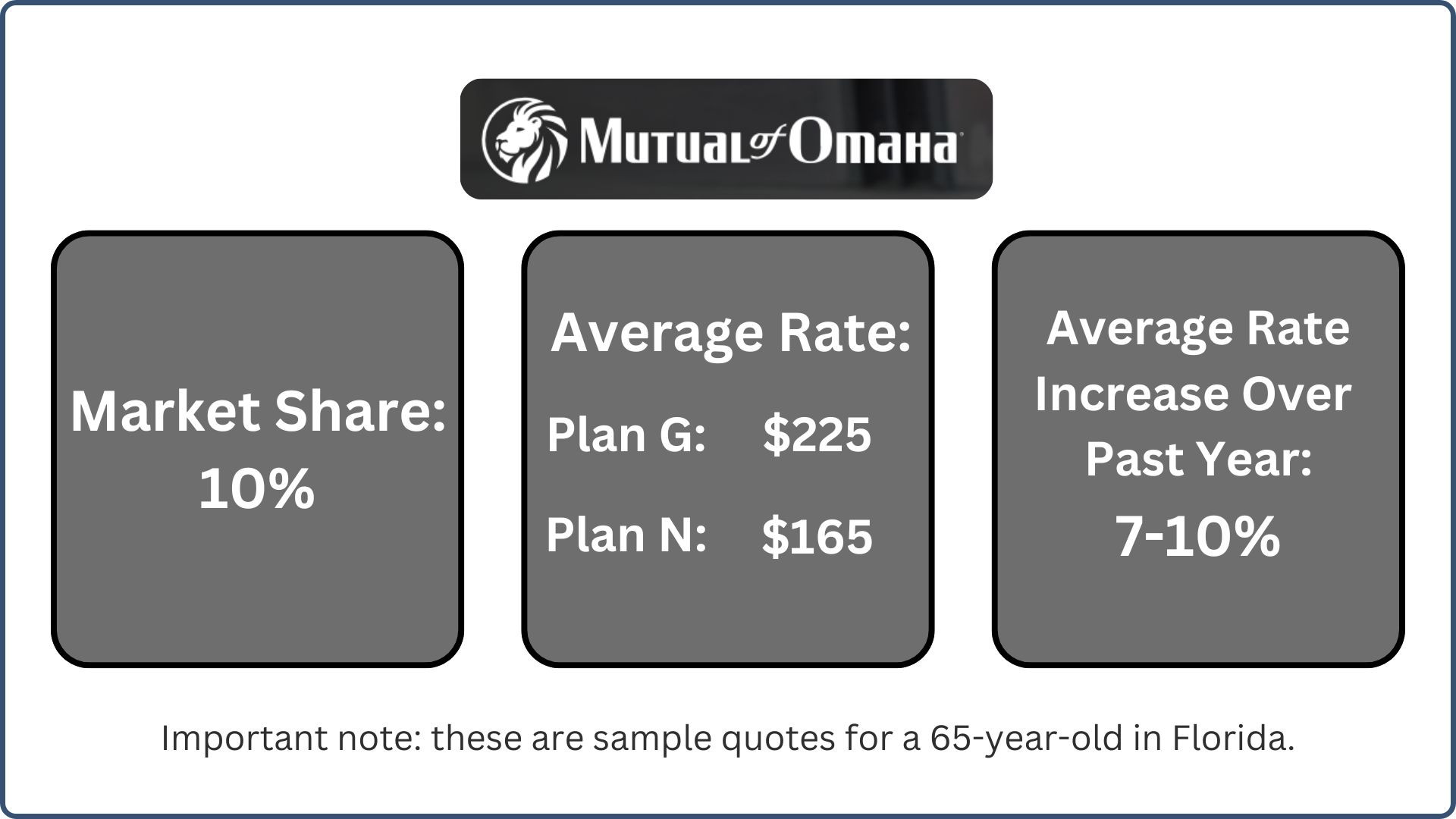

#3. Mutual Of Omaha

The third best Medigap company would be Mutual of Omaha.

They have a market share of 10%.

The average rate of Plan G is $225 and Plan N is $165. I picked Florida and a 65-year-old for these sample quotes.

Again, we’re seeing an average rate increase over the past year of 7% to 10%.

Mutual of Omaha offers eight standardized plans. They offer the same household discount, but theirs is up to 12%. They have dental policies with a 15% bundling discount.

They also offer access to the Mutually Well program.

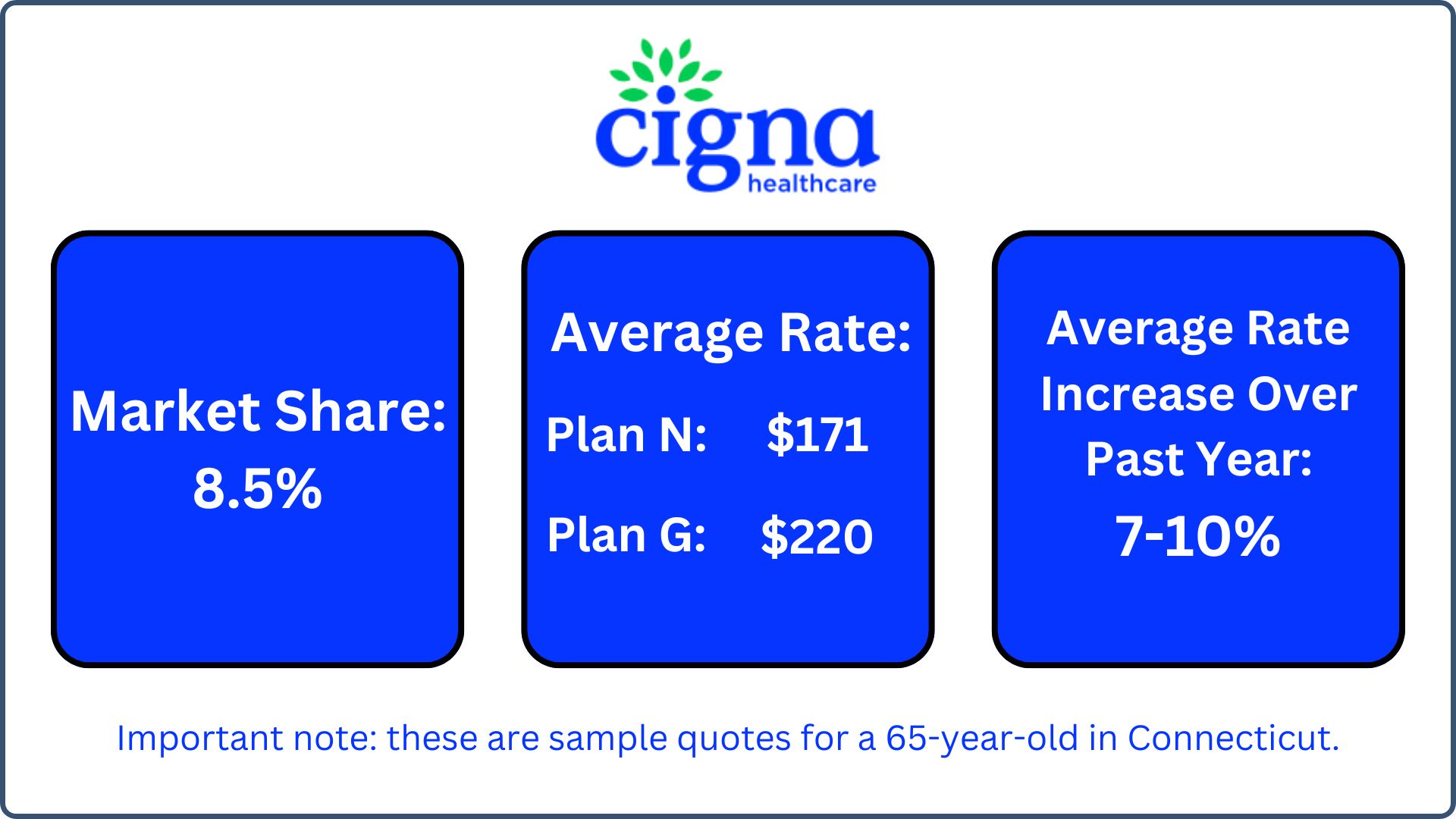

#4. Cigna

Moving on to Cigna.

You can see that the market share is a little lower, at 8.5%.

Average rates were run for a 65-year-old in Connecticut. Plan N is $171. Plan G is $220.

Again, the same on the rate increase history of 7% to 10%.

Cigna offers four standardized plans, which include F, G, and N, and up to 25% premium discounts.

They also offer a Healthy Rewards program, and 24/7 customer service.

Next, I’m going to switch gears and go over some smaller companies that are newer to the market.

What Are the Cheaper Options?

These companies are showing more favorable monthly premiums, but rate increases seem to be running in the same range.

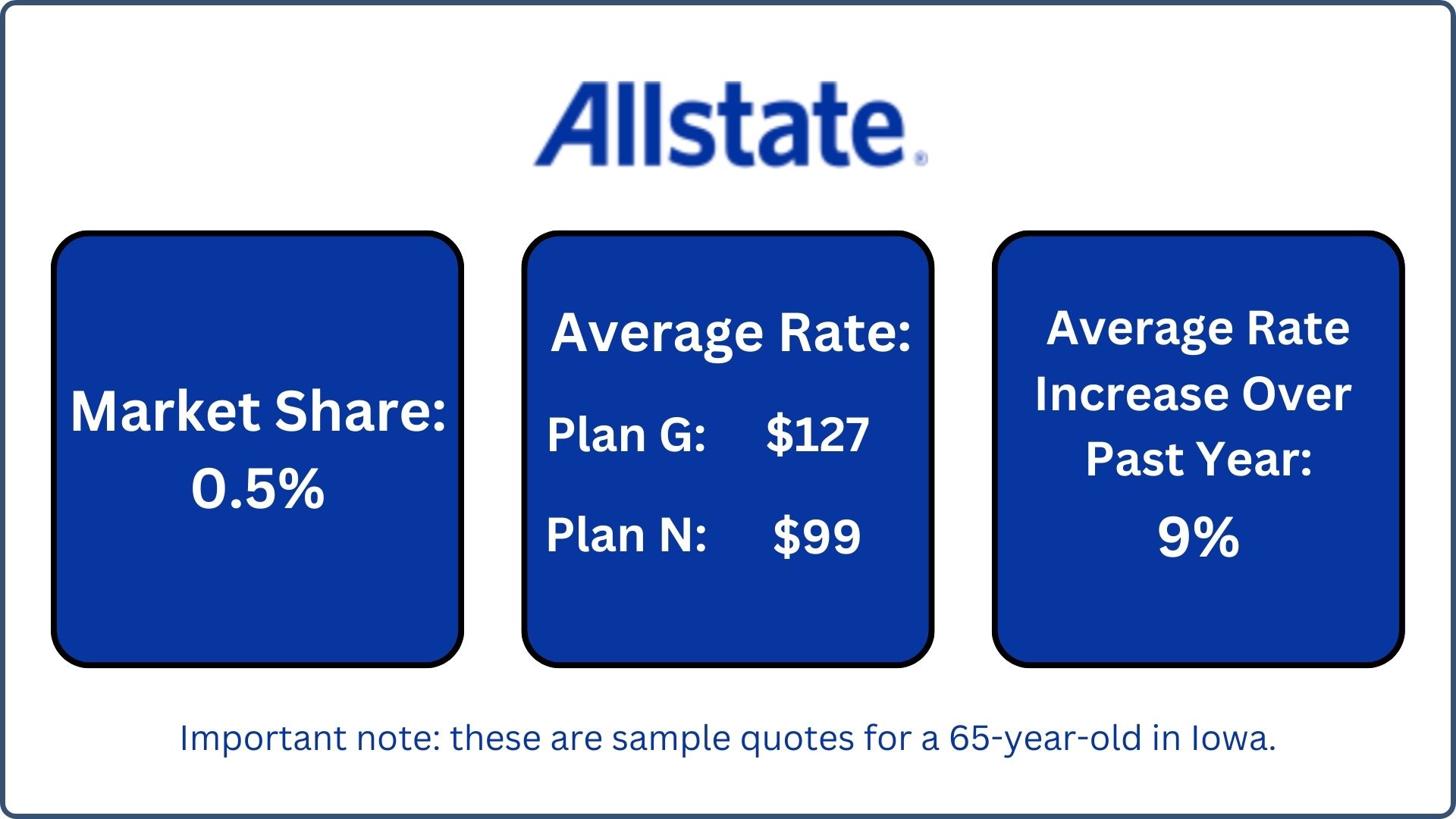

#1. Allstate

First, Allstate has a very small market share, roughly half a percentage point, because it has only been in the industry for a few years now.

The average rate on Plan G is $127, and the average rate on Plan N is $99. That was a quote run for a 65-year-old in Iowa.

We’re seeing an average rate increase over the past year of 9%.

One of the features that we really like about Allstate is that they offer all 10 standardized plans, but they also have a significant number of stackable discounts that you can qualify for (that add up to 25%).

We’re finding about a 12% more affordable premium on Plan N and G with Allstate to begin with, but again, keep in mind we’re seeing the same average rate increases.

They also offer an Active&Fit fitness program.

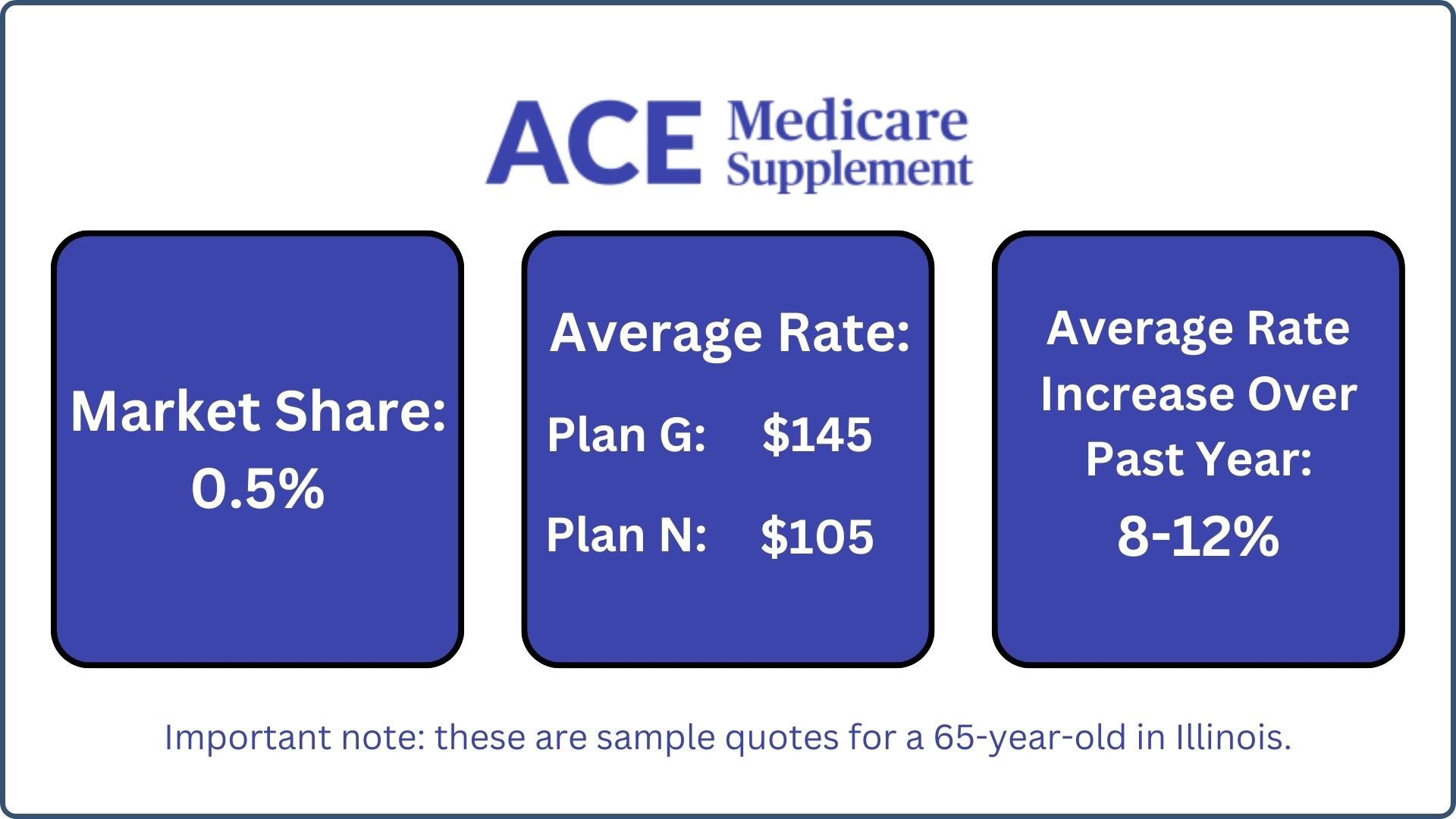

#2. ACE

Last but not least is ACE, which is owned by a large property insurance company called Chubb.

They’re, again, less than 1% of the market share.

The average rate on Plan G in Illinois for a 65-year-old is $145, and on Plan N is $105.

We’re seeing the same average rate increase in range over the past year of around 8% to 12%.

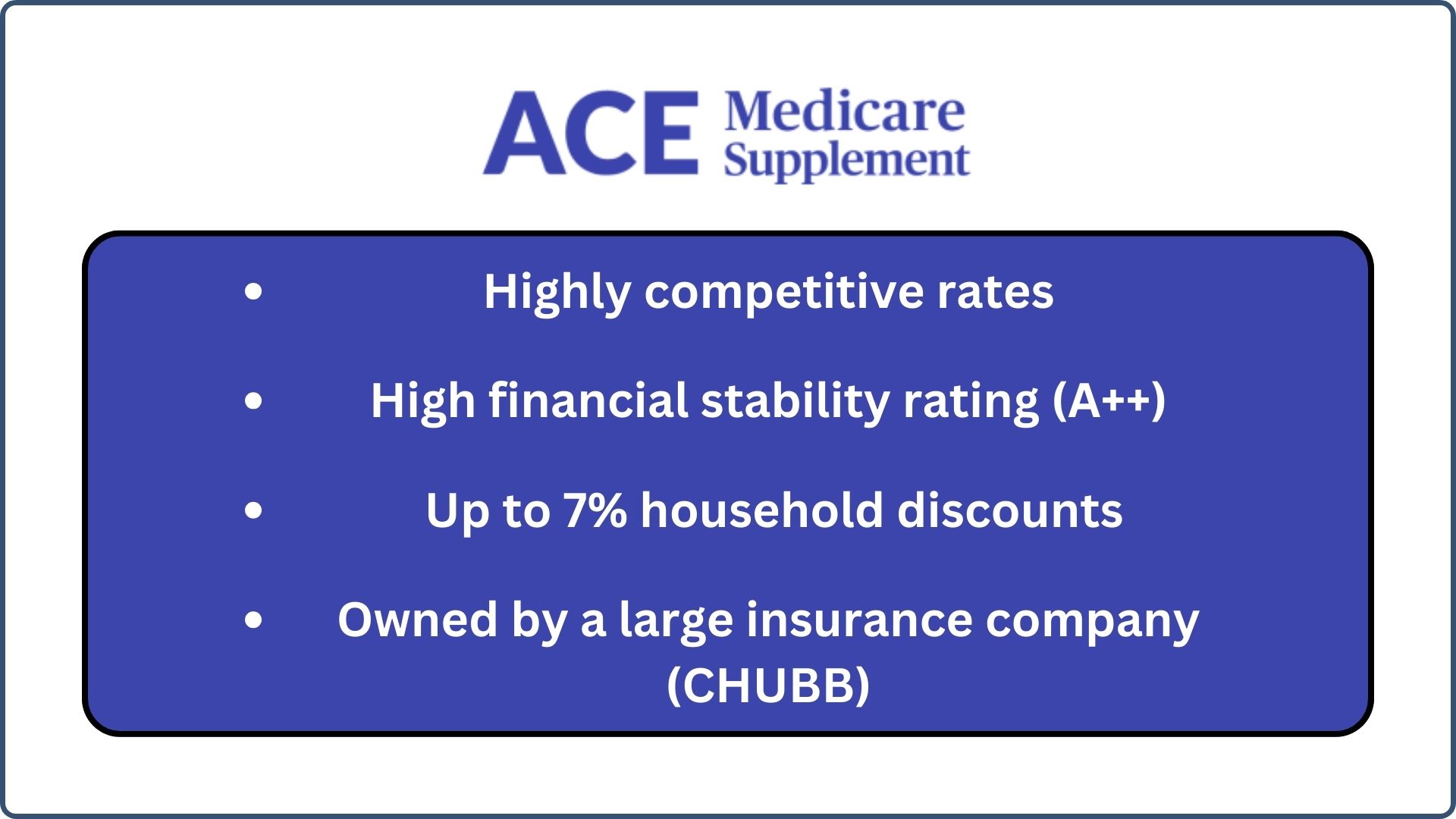

ACE is well known for its low premiums. They have highly competitive rates. Their financial stability rating is A++ (that’s because they’re a part of the Chubb organization).

They really only offer up to a 7% household discount, no other additional features or ancillary products.

So we’ve covered a lot. We’ve talked about some of the largest companies, their average premiums, and then what we have seen internally on average rate increases over the last year.

Again, as these claims from post-COVID start to calm down, we’re hopeful that rate increases should start to decrease over the next year or two, keeping the Medigap premiums more stable for most of the Medigap companies.

Now, I want to briefly cover some of the Medigap benefits.

Medigap Benefits

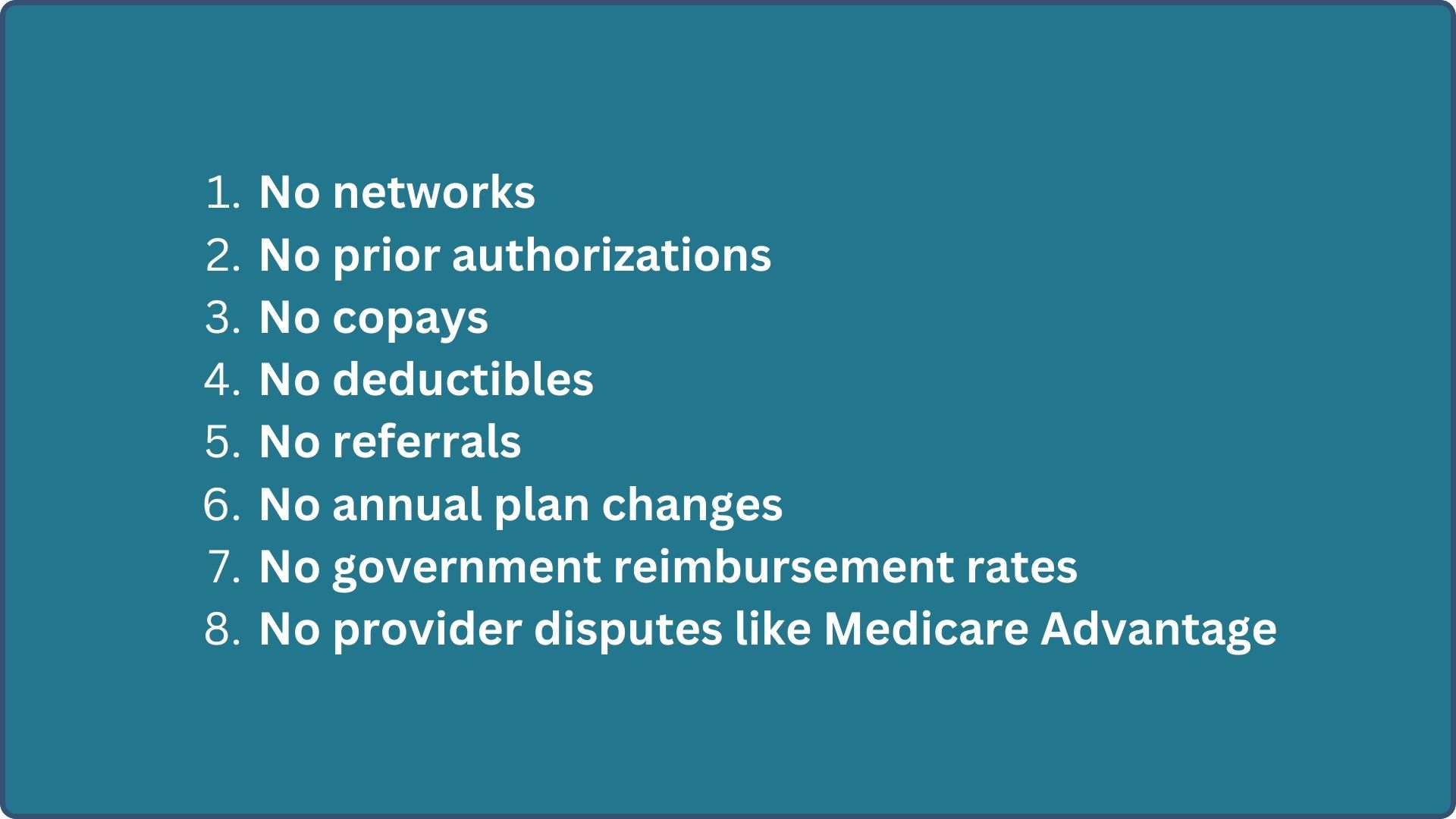

The nice thing about Medigap, also known as Medicare Supplement, is that when you compare plans, they’re very easy to understand.

- There are no networks to compare

- No prior authorizations

- No copays and no deductibles other than your Medicare Part B deductible (if you’re looking at Plan G, and small copays for Plan N)

- No referrals

- No annual plan changes

- No government reimbursement rates like Medicare Advantage

- No provider disruptions like Medicare Advantage

Next up, let me give you some tips and pointers on how to compare Medigap plans and companies.

Medigap Comparison Tips

When you’re out there doing your own research, this should help you streamline that process and remove some of the stress of comparing different companies.

Some of the highlights here are:

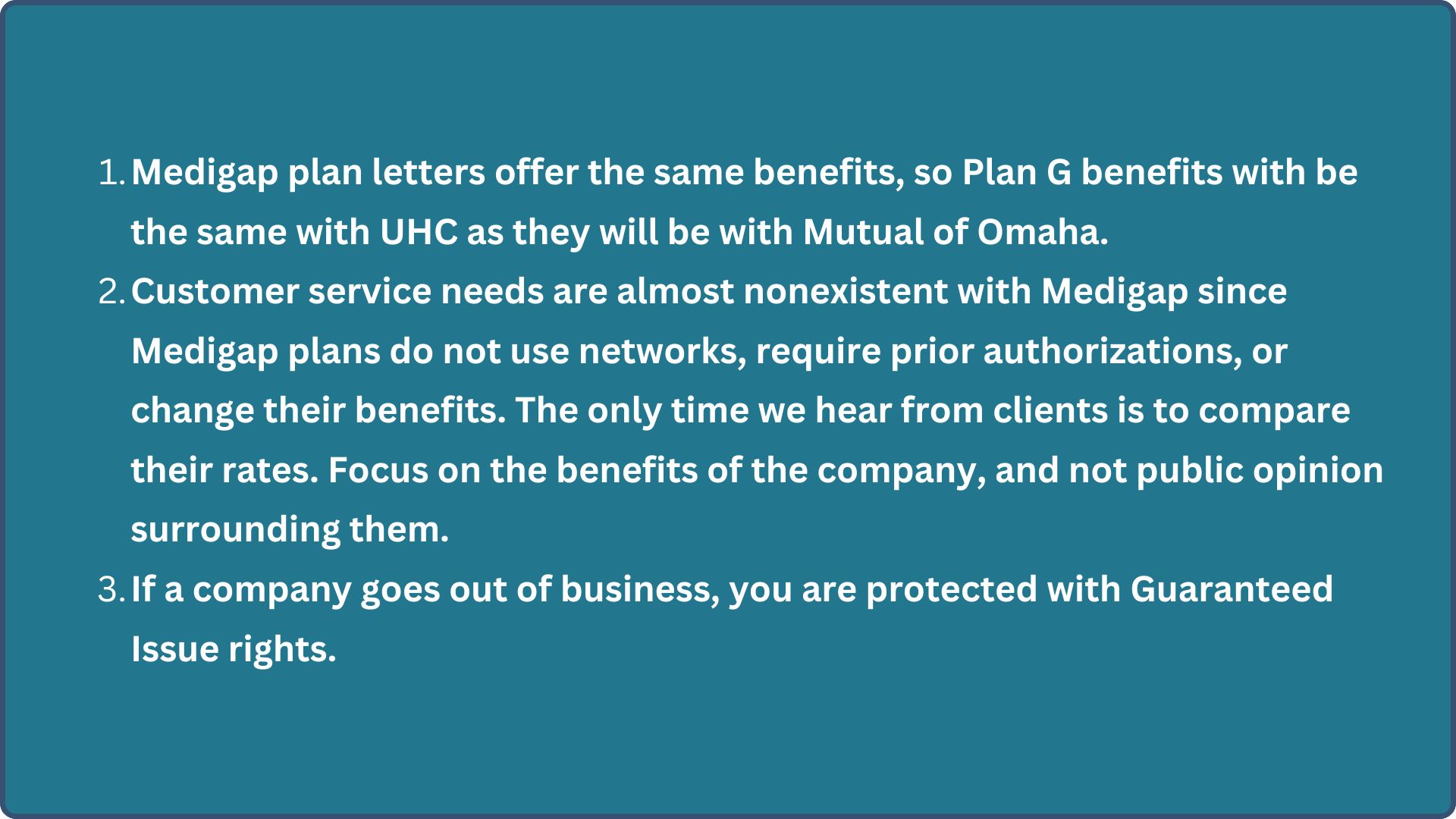

#1. Medigap plan letters offer the same benefits. So, Plan G benefits will be the same with UnitedHealthcare as, say, they will be with Mutual of Omaha.

#2. Customer service needs are almost nonexistent with Medigap since Medigap plans do not use networks, prior authorizations, or changes of benefits annually. The only time that we typically hear from a client is to compare their rates and see if there’s a more affordable option available.

#3. Let’s say you pick a company, and that company goes out of business. You are protected with guaranteed issue rights.

-

What Are GI Rights?

If you pick a smaller, lesser-known company, and that smaller company should become insolvent, sell, or go out of business, you’re protected with guaranteed issue rights.

This means that you can leave that company and go to another one without having to answer any medical questions.

So once you select a Medigap plan with any company, your benefits are fixed for life, and your coverage is guaranteed for life, even if you have to move from one company that goes out of business to another.

Again, as a reminder, Medicare Supplement rate increases are regulated by each state’s Department of Insurance.

What does that mean?

That means when a Medigap company requests a rate increase, the Department of Insurance for that individual state has to approve it. The company must provide proof or evidence that they’re not receiving enough premiums for how much they pay out in claims.

No company can raise its rates wildly without regulation. These plans are heavily regulated in your favor for your protection as the consumer.

We’ve talked about companies, but let’s look at the Medigap plans for just a moment.

What Are the Most Popular Medigap Plans?

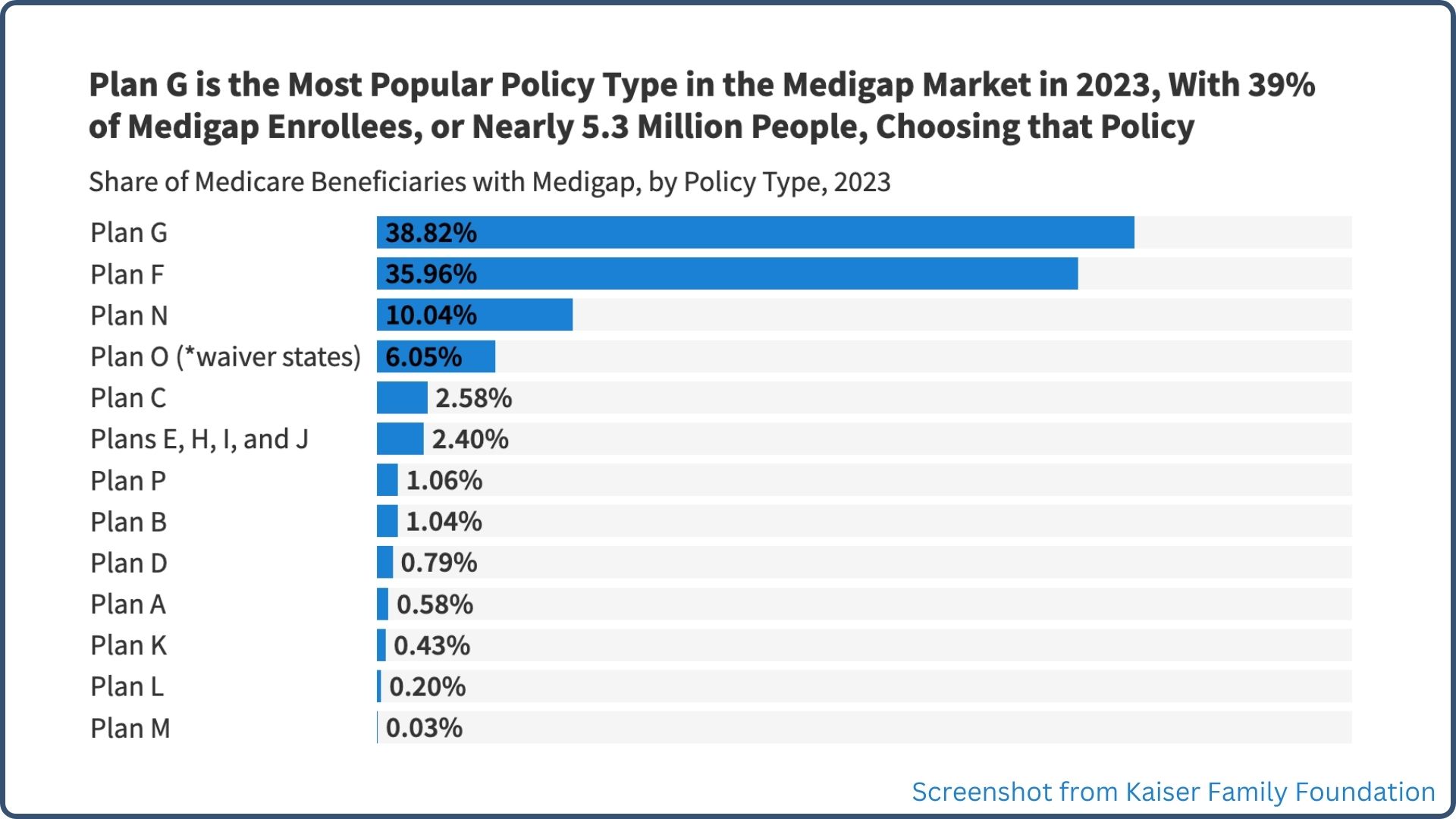

Plan G is the most popular policy type in the Medigap market.

This study is from 2023, with 39% of Medigap enrollees, or nearly 5.3 million people, choosing Medigap Plan G:

So, Medigap Plan G is predominantly the #1 plan, followed by Plan N. Plan G and N are the two most popular plans that you can compare and choose from.

All of the others are almost nonexistent in terms of enrollment popularity.

Average Medigap Plan Premiums

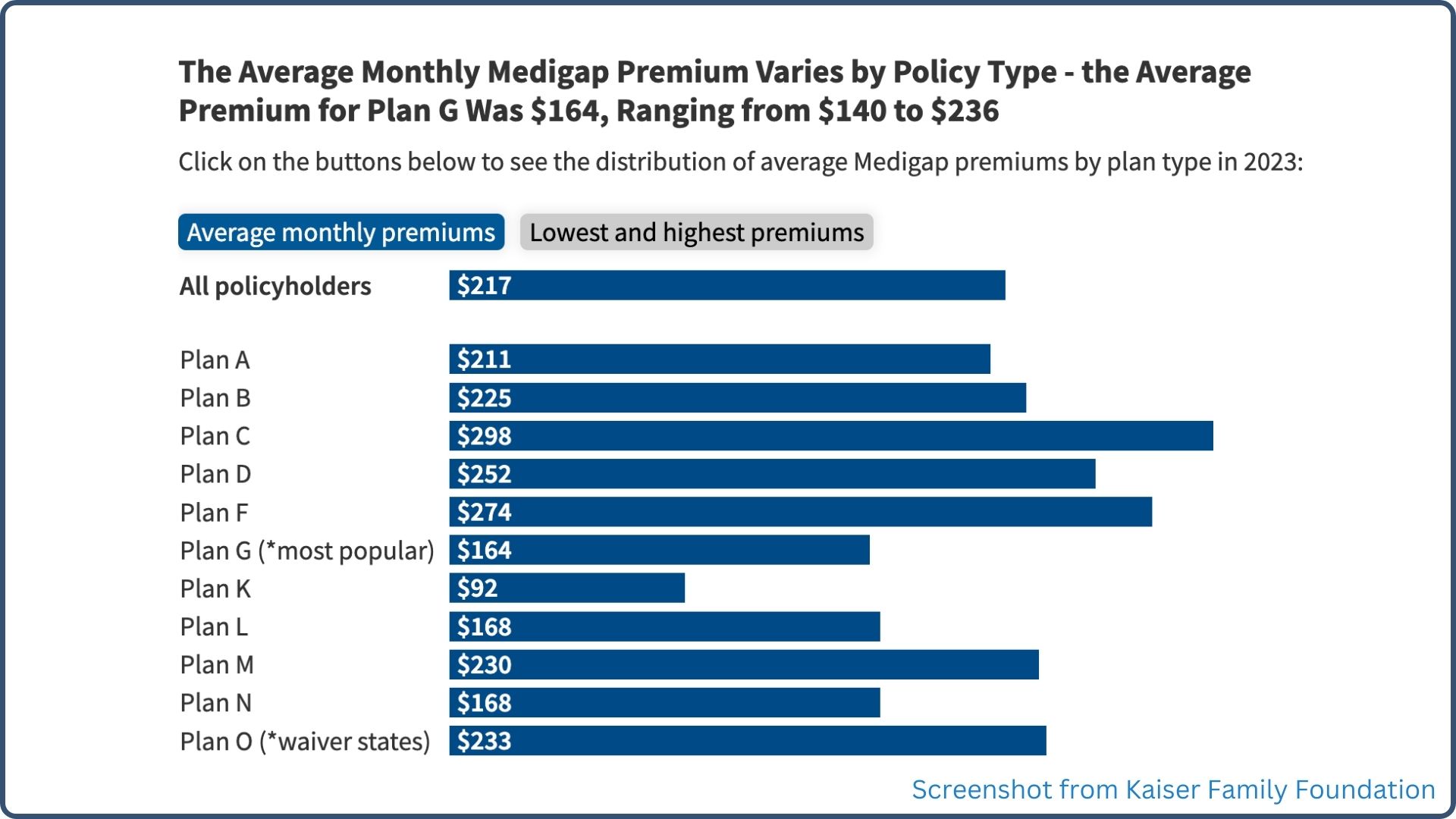

Let’s take a look at average Medigap rates on a national scale with Plan G. The average monthly Medigap premium varies by policy type.

The average premium for Plan G was $164 in 2023, ranging from $140 to $236. You can see on the chart here that Plan G is the most popular, coming in at $164:

Your individual rate will vary by the company you choose, the state you live in, the age at which you enroll, and any household discounts that you are eligible for.

This was just a snapshot showing that the average for Plan G is $164, but your individual rate will vary depending on the factors I’ve just listed.

Don't Get Overwhelmed!

My last tip for you is: don’t get overwhelmed.

Medigap comparison is much easier than comparing Medicare Advantage. Most people will go to the internet and review the best Medicare Supplement companies and this happens:

They’ll start with Google. They’ll look at the results in Google, which are not always accurate. Those are companies like Investopedia or Forbes that are just compiling data.

They really don’t offer any unique insight because they’ve never personally worked with these companies one-on-one like we have.

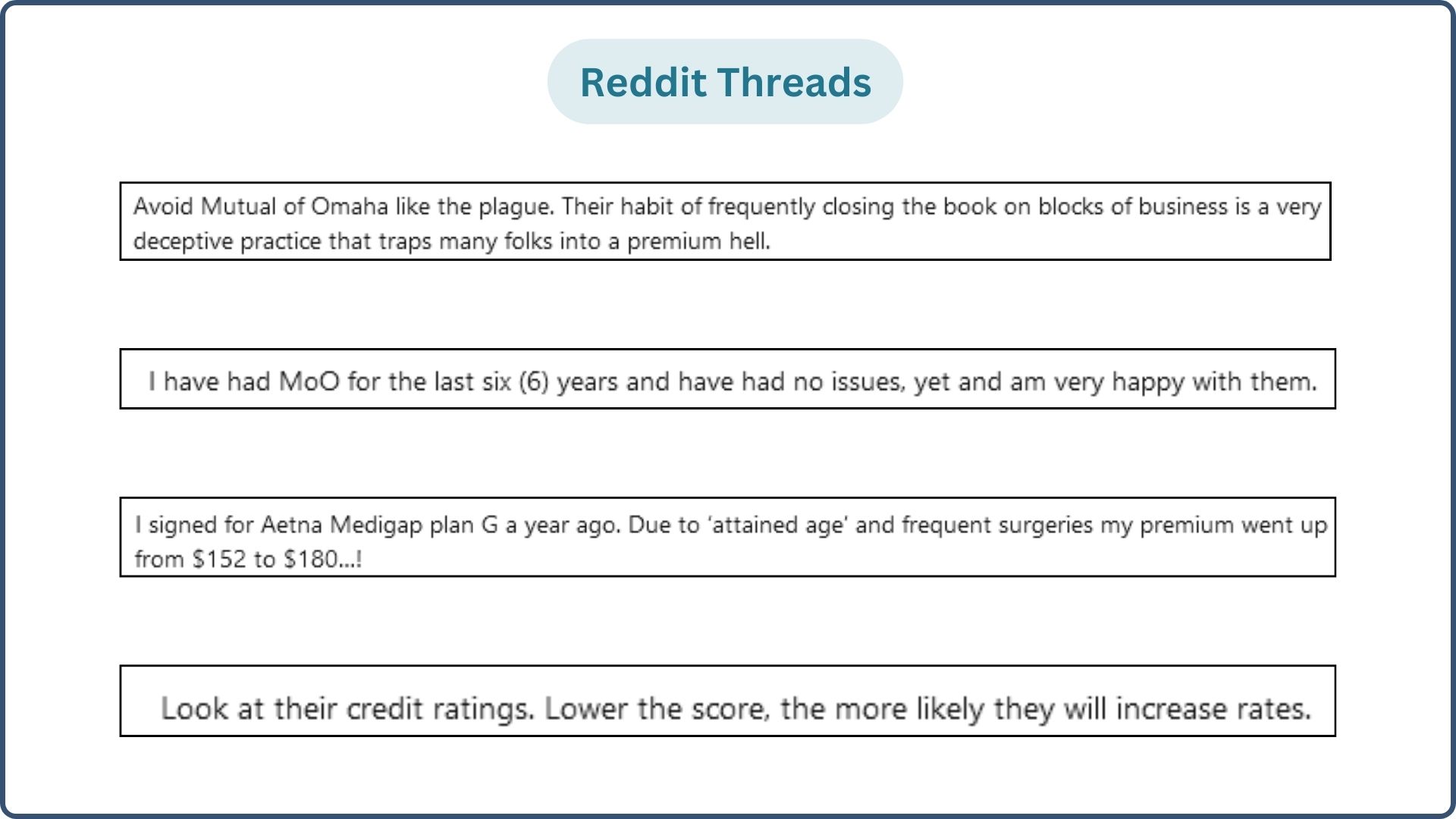

Let’s take a look at some Reddit comments I screenshotted.

Warning: Gathering information on Reddit is not only dangerous but often gives you, the reader, a lot of misinformation and makes the comparison process even more stressful.

#1. “Avoid Mutual of Omaha like the plague. Their habit of frequently closing the book on blocks of business is a very deceptive practice that traps many folks into a premium hell.”

All Medicare Supplement companies will start and close a block of business. That’s how they remain competitive for newcomers. If you’re on a Medicare Supplement and they close your block of business, you are not trapped in a “premium hell”. You can still switch companies.

That’s not a practice of Mutual of Omaha. That’s a practice for all companies, and that’s just the nature of the business.

The next one basically contradicts the first one. It says:

#2. “I’ve had MOO (or Mutual of Omaha) for the last six years, and have had no issues yet, and I am very happy with them.”

The next one is:

#3. “I signed up for Aetna Medigap Plan G a year ago. Due to attained age and frequent surgeries, my premiums went up from $152 to $180.”

Frequent surgeries or claims have nothing to do with premium rate increases. That is a myth. Premium rate increases are not individualized per person or per their actions. They are based on the risk of the whole group, not one individual claim.

And lastly, here’s another bit of really bad advice:

#4. “Look at their credit ratings. The lower the score, the more likely they will increase your rates.”

That is just not accurate information. That is not based on factual ways that companies increase Medigap rates.

Let me just point this out to you here:

Whatever Medicare Supplement company you select, you are doing better than half of Medicare beneficiaries out there on a Medicare Advantage plan.

Yes, premiums will increase, but you will not be trapped in a “premium hell” like these individuals discuss.

You cannot escape rate increases, just like you cannot escape them with auto, homeowners, or the price of milk, or the price of bread and gas.

Final Thoughts

Unfortunately, healthcare costs rise. It’s just the nature of the beast. But with Medigap, you’ll still have the same exact benefits.

The premiums may vary, but as you’ve seen, rate increase history tells us that there’s no magic silver bullet company that can keep rates lower for longer than others. It just doesn’t work that way. They all march to the beat of the same drum.

I congratulate you and commend you for looking at a Medigap plan because, despite the rate changes that you may experience, it is still the most comprehensive coverage you can get, with the most freedom and the most flexibility. You’re in control. You do not have to pick doctors and hospitals.

You do not have to worry about doctors leaving your network because you don’t have a network. You can visit up to 95% of doctors in the United States who take Original Medicare with your Medicare Supplement, no matter which company it is.

Your benefits are fixed for life, and there are no annual plan changes like that of Medicare Advantage.

I know I’ve covered a lot of information in this article. I hope this has been helpful. If you have questions or if you need help picking a plan or company, feel free to call us directly. We’d be happy to do a needs analysis with you.

Thanks!

Sources: Kaiser | Department of Health

FAQs

- What is Medigap Plan G, and why is it so popular?

- How are Medigap plan premiums determined?

- What should I be cautious about when researching Medigap plans online?

- Will my benefits change annually with a Medigap plan?

- How do Medigap plans compare to Medicare Advantage plans?