Best Medicare Plans for Travelers - Medigap Wins

From my experience as a Medicare agent, I highly recommend Medicare Supplement Plan G for anyone traveling inside the US and outside the US and its territories. Plan G offers extensive benefits, including coverage for foreign travel emergencies.

Medigap Plan G covers:

- Emergency care during the initial 60 days of your trip (if Medicare does not cover it).

- 80% of the billed charges for medically necessary emergency care outside the US after you’ve met the $257 annual deductible.

Good healthcare coverage is a must when traveling. Unfortunately, Original Medicare usually doesn’t cover you outside the US, except in specific situations. This can leave many people with significant gaps in their healthcare.

That’s where Medicare Supplement plans, or Medigap, come into play. These plans help fill in the gaps left by traditional Medicare.

As noted on Medicare.gov, most Medigap plans include emergency healthcare coverage when traveling outside the US, with a lifetime limit of $50,000.

How Does Foreign Travel Coverage Work?

Medigap plans that include foreign travel emergency benefits typically cover 80% of the costs for emergency care abroad (provided that care begins during the first 60 days of your trip), leaving the remaining 20% for you to pay out of pocket.

Before you receive coverage, you’re responsible for a $257 yearly deductible, and a $50,000 lifetime limit applies to foreign travel emergency coverage.

If you have a Medicare Supplement plan, it will offer coverage for emergency health services during foreign travel. However, if you only have Original Medicare, this additional coverage will not be available outside the United States.

Top Medigap Plans for Travelers

I recommend three Medigap plans for frequent travelers. Let’s walk through each plan together.

#1. Medigap Plan G

Plan G is the most comprehensive option out there, covering all the gaps in Original Medicare except for the Part B deductible. It’s a great choice if you’re looking for maximum coverage with minimal out-of-pocket expenses.

If you love to travel, you’ll appreciate the foreign travel emergency benefits—they cover 80% of emergency costs abroad after a $257 deductible, with a lifetime max of $50,000.

Plus, there are no network restrictions, so you can see any doctor or specialist nationwide who accepts Medicare.

Plan G Key Takeaways:

- 100% coverage for Medicare Part A deductible and coinsurance.

- 80% coverage for foreign travel emergencies after a $257 deductible, up to a $50,000 lifetime limit.

- No network restrictions—access any doctor or specialist nationwide who accepts Medicare.

- Best for travelers who want premium coverage without worrying about out-of-pocket costs for non-deductible expenses.

#2. Medigap Plan N

Plan N offers lower premiums for a more affordable option while offering excellent foreign travel emergency coverage.

Like Plan G, it covers 80% of emergency costs abroad after a $257 deductible. However, it requires small copayments for doctor and emergency room visits and does not cover the Part B deductible or excess charges (providers that charge more than Medicare-approved rates).

This plan is well-suited for travelers who don’t mind paying minor out-of-pocket costs in exchange for reduced premiums.

Plan N Key Takeaways:

- Foreign travel emergency coverage is identical to Plan G (80% of emergency costs after a $257 deductible).

- Lower monthly premiums make it a budget-friendly option for travelers who are comfortable with small copayments.

- There is no coverage for the Part B deductible and excess charges.

#3. High Deductible Plan G

High Deductible Plan G provides the same comprehensive benefits as standard Plan G but with significantly lower monthly premiums due to a higher annual deductible ($2,870 in 2025).

This plan is an excellent choice for travelers looking to keep things affordable while still getting solid emergency coverage. After meeting the deductible, you’ll still receive 80% coverage for emergencies abroad.

It’s perfect for anyone who wants to save on upfront costs but still stay protected from significant medical expenses while traveling.

High Deductible G Key Takeaways:

- Offers the same comprehensive coverage as Plan G but significantly lower premiums due to a higher annual deductible ($2,870 in 2025).:

- Covers foreign travel emergencies, including 80% of costs after a $257 deductible and up to a $50,000 lifetime limit.

- Best for travelers seeking comprehensive emergency coverage with lower upfront costs.

Next, I’ll highlight our top recommended companies for these Medigap plans, breaking down their benefits and pricing and explaining why they stand out among the competition.

Top Medigap Companies

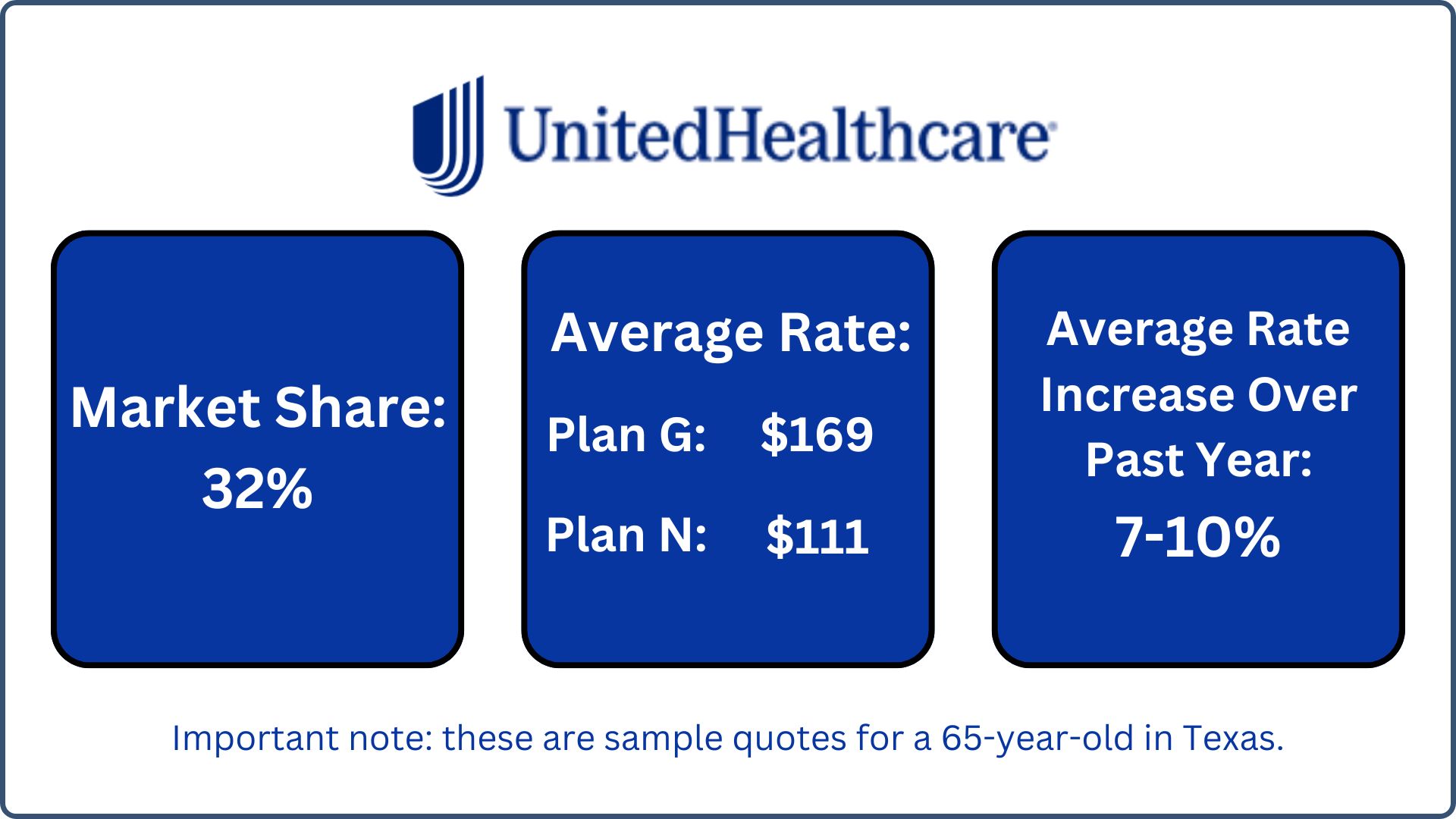

#1. UnitedHealthcare: Large provider network

From my experience, UnitedHealthcare stands out for its large provider network and added benefits tailored to active lifestyles.

Their average premium for Plan G is around $169, and Plan N is $111, making them competitive in several states, such as Florida, Michigan, and California.

The Renew Active program is particularly appealing for travelers as it provides access to nationwide fitness facilities, ensuring you stay healthy no matter where you are.

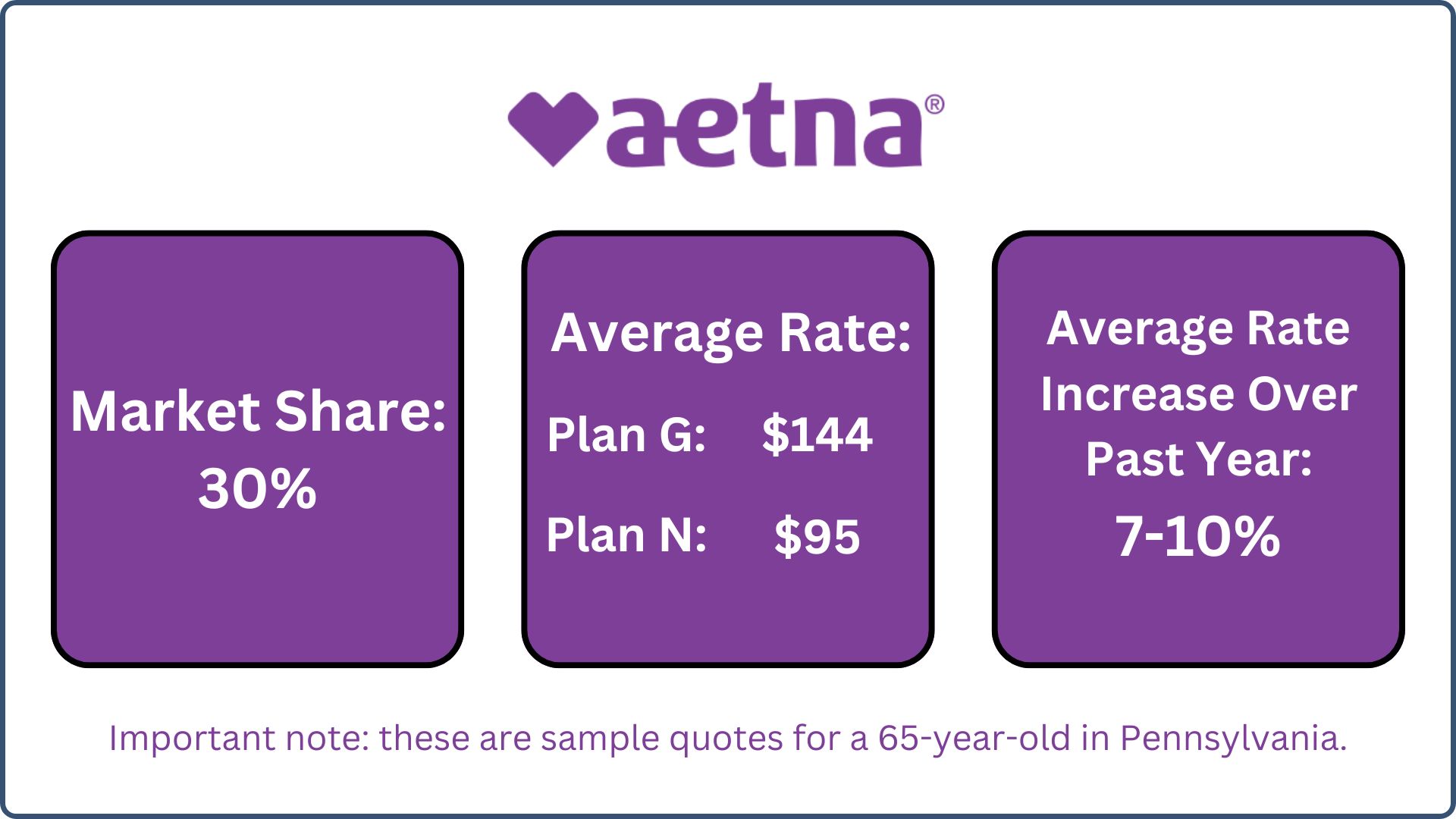

#2. Aetna: Competitive premiums

Many of my clients prefer Aetna for its reliable coverage and competitive pricing. The average premiums are $144 for Plan G and $95 for Plan N.

Also, their household discount of up to 7% can make a significant difference for couples.

Aetna’s optional dental and hearing coverage has been highly appreciated by travelers who want comprehensive care, even while on the move.

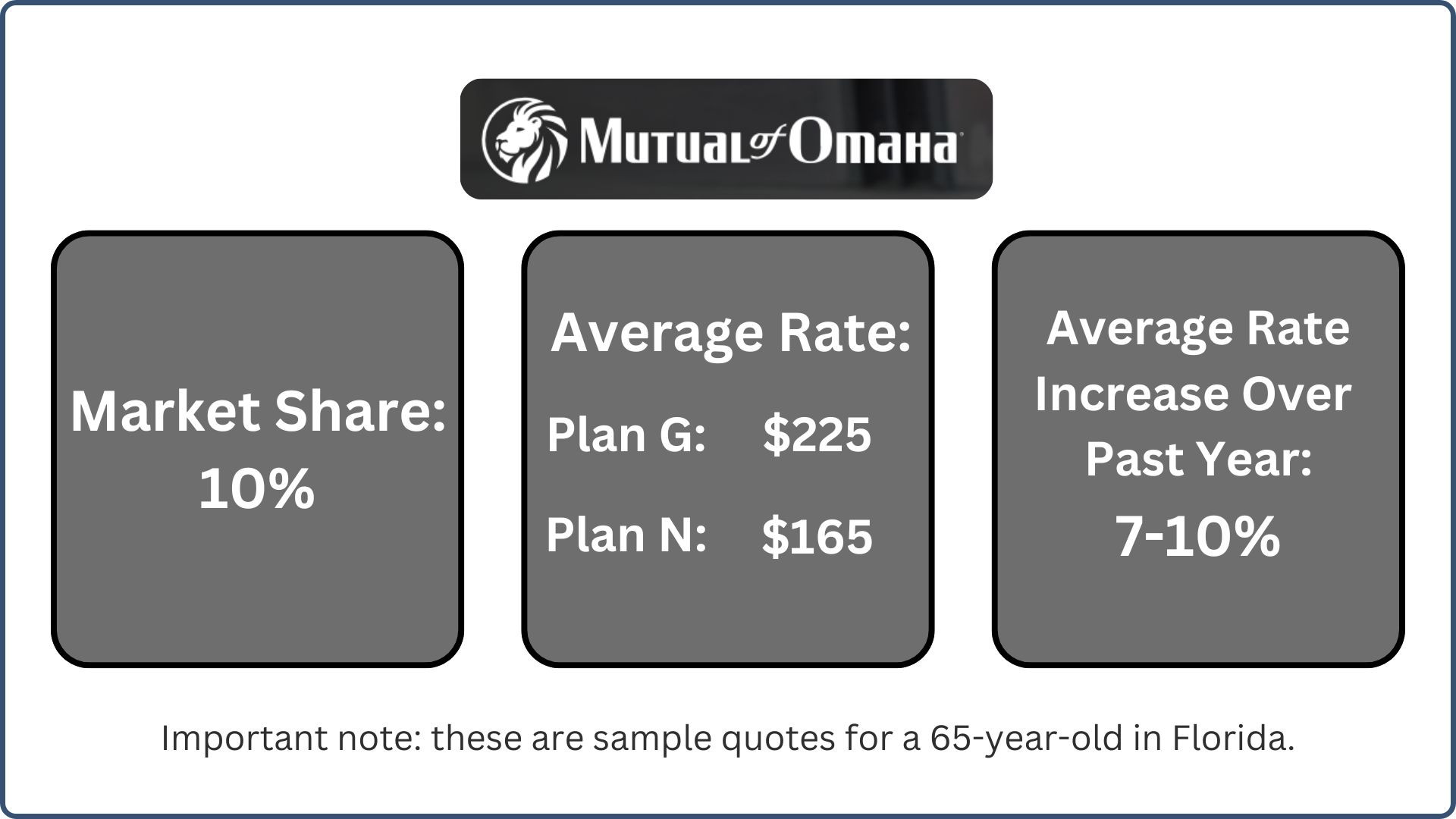

#3. Mutual of Omaha: Several discount options

Mutual of Omaha is popular in the Medigap market, with an average premium for Plan G at $225 and Plan N at $165.

They offer a 12% household discount and access to the Mutually Well program. This program provides discounts on wellness services and fitness, making it easier to maintain a healthy lifestyle no matter where your travels take you.

Are Medigap Plans Accepted Everywhere?

Yes, Medigap plans are accepted everywhere in the United States that accepts Medicare. These plans work alongside Original Medicare (Part A and Part B) to help cover costs like deductibles, copayments, and coinsurance.

Since they are tied to Medicare, healthcare providers who accept Medicare will also accept your Medigap plan, regardless of the insurance company that issued it.

Note: This nationwide acceptance is one of the key advantages of Medigap plans over Medicare Advantage plans, which typically have restricted provider networks.

Medigap’s broad acceptance makes it an excellent choice for individuals who value the flexibility to see any doctor or specialist without worrying about network limitations—especially beneficial for travelers or those living in multiple locations throughout the year.

Next, if you’re considering enrolling in a Medigap plan, let’s walk through what the process will look like.

How to Apply for a Medigap Plan

Applying for a Medicare Supplement plan is simple, and it’s best to do so during your Medigap Open Enrollment Period. The Medigap OEP starts the first day of the month that you are 65 or older and are enrolled in Medicare Part B. This period lasts six months, so taking advantage of this period ensures the best outcome for your Medicare coverage.

This six-month period offers the advantage of guaranteed issue rights, ensuring that insurance providers cannot deny coverage, even if you have pre-existing conditions.

You can apply online, over the phone, or in person with any private insurance company that sells Medicare Supplement plans.

For frequent travelers considering a Medicare Advantage plan, it’s important to understand why this option might not be the most suitable choice for your needs. Let me explain further.

Medicare Advantage Plans: Not Ideal for Frequent Travelers

I’ve guided countless individuals in finding the best Medicare coverage for their unique needs. While Medicare Advantage plans have their place for some beneficiaries, they often fall short for those who love to travel, whether for leisure or a lifestyle on the move. Here are a few reasons why.

#1. Emergency Coverage Is Not Enough

It’s true that Medicare Advantage plans cover emergencies nationwide. However, emergencies represent only a tiny fraction of travelers’ healthcare needs. Routine doctor visits, specialist consultations, and non-urgent care outside your plan’s network can result in significant out-of-pocket expenses.

Here are some real-life scenarios:

- Scenario 1: A Retiree Vacationing in Florida

Samantha, a Medicare Advantage beneficiary from Ohio, spends winters in Florida. While there, she develops a persistent cough and decides to see a local doctor. Unfortunately, because her plan is an HMO, she’s required to see her primary care physician in Ohio for a referral—something impossible while she’s out of state.

Without a referral, Samantha’s visit to an out-of-network doctor results in a hefty bill she must pay out of pocket.

- Scenario 2: A Couple Traveling Full-Time in an RV

Bob and Susan sold their home and live on the road, exploring the U.S. Their Medicare Advantage PPO plan allows some out-of-network coverage but at much higher costs. When Bob needs outpatient testing in Arizona, they discover that the nearest in-network facility is hundreds of miles away.

Bob uses an out-of-network provider with no other option and is hit with a bill totaling thousands of dollars after deductibles and coinsurance.

#2. Restricted Networks Cause Challenges

Medicare Advantage plans typically operate within regional networks. If you’re outside your plan’s service area, you’re limited to emergency care unless you’re willing to pay the higher out-of-network costs. This makes it difficult for snowbirds, RV travelers, or anyone who splits their time between multiple locations to access affordable care.

- Scenario: Patricia, a snowbird from New York, discovered her Medicare Advantage plan’s in-network specialists didn’t extend to her winter home in Arizona. To manage her chronic condition, she had to schedule all her medical appointments for the months she was in New York, making her travel plans stressful and inconvenient.

In contrast, Medigap plans work seamlessly for travelers. These plans allow beneficiaries to see any doctor or specialist who accepts Medicare, regardless of location. Whether you’re dealing with a sudden illness or need routine care while away from home, Medigap plans ensure you’re covered without the hassle of network restrictions.

- Consider this scenario: John, a Medigap Plan G beneficiary, spends the summer in Colorado and winter in Florida. While hiking in Colorado, he injures his ankle and visits a local orthopedist. Since the orthopedist accepts Medicare, John’s Medigap plan covers the costs after his Part B deductible, with no network worries or surprise bills.

#3. Out-of-Pocket Costs Can Add Up Quickly

Although Medicare Advantage plans often have lower premiums, they can incur higher out-of-pocket costs for frequent travelers.

Co-pays, coinsurance, and deductibles for out-of-network care can quickly surpass the predictable costs of a Medigap plan.

For instance, a Medicare Advantage enrollee might pay $1,500 for diagnostic testing out-of-network, followed by additional charges for follow-up care.

In contrast, a Medigap Plan G policyholder would pay only the Part B deductible for similar care, and the plan would cover the rest.

Bottom Line

For travelers, we highly recommend Medicare Supplement Plan G, Plan N, and High Deductible Plan G as the top choices. These Medigap plans offer the most comprehensive benefits, including foreign travel coverage.

When choosing a Medigap plan, consider these top-rated companies:

- UnitedHealthcare: known for its extensive market presence, competitive premiums, and additional perks like the Renew Active program for nationwide fitness access.

- Aetna: offers strong household discounts, competitive premiums, and optional dental and hearing coverage.

- Mutual of Omaha: provides exceptional customer benefits like the Mutually Well program and significant bundling discounts.

Unlike Medicare Advantage plans, which can limit access to routine or specialist care outside your home region, Medigap plans provide consistent coverage across the U.S. and abroad. This makes them especially beneficial for frequent travelers, vacationers, or those embracing a nomadic lifestyle.

Consulting with a licensed Medigap insurance agent can help you explore your options and select the policy that best fits your needs.

As a Medicare agent, my advice is simple: if travel is an integral part of your life, a Medigap plan can save you time, stress, and money—allowing you to travel without worrying about health coverage limitations.

Sources: NCOA | AARP | Medicare.gov

FAQs

- Does Medigap Plan G cover international travel?

- Does Original Medicare cover international travel emergencies?

- What happens if I need medical services not covered by my Medigap plan?