Blue Cross Blue Shield of Texas Medicare Supplement Review

When it comes to finding the best Medicare Supplement company in Texas, you have many choices.

However, I will focus today on Blue Cross Blue Shield of Texas and compare its plans, benefits, and rates against four other well-known Medicare Supplement companies in Texas.

I’ve been teaching people about how Medicare works for over 15 years. In this article, I’ll cover Blue Cross Blue Shield of Texas. I’m focusing primarily today on:

- BCBS Overview

- Plan G and Plan N premiums (the two most popular plans)

- BCBS premium comparison (to other leading providers)

- Available premium discounts

- Pros and cons of BCBS vs. competitors

Last, but not least, I’m going to get into everyone’s favorite topic: rate increases. So, let’s jump right in.

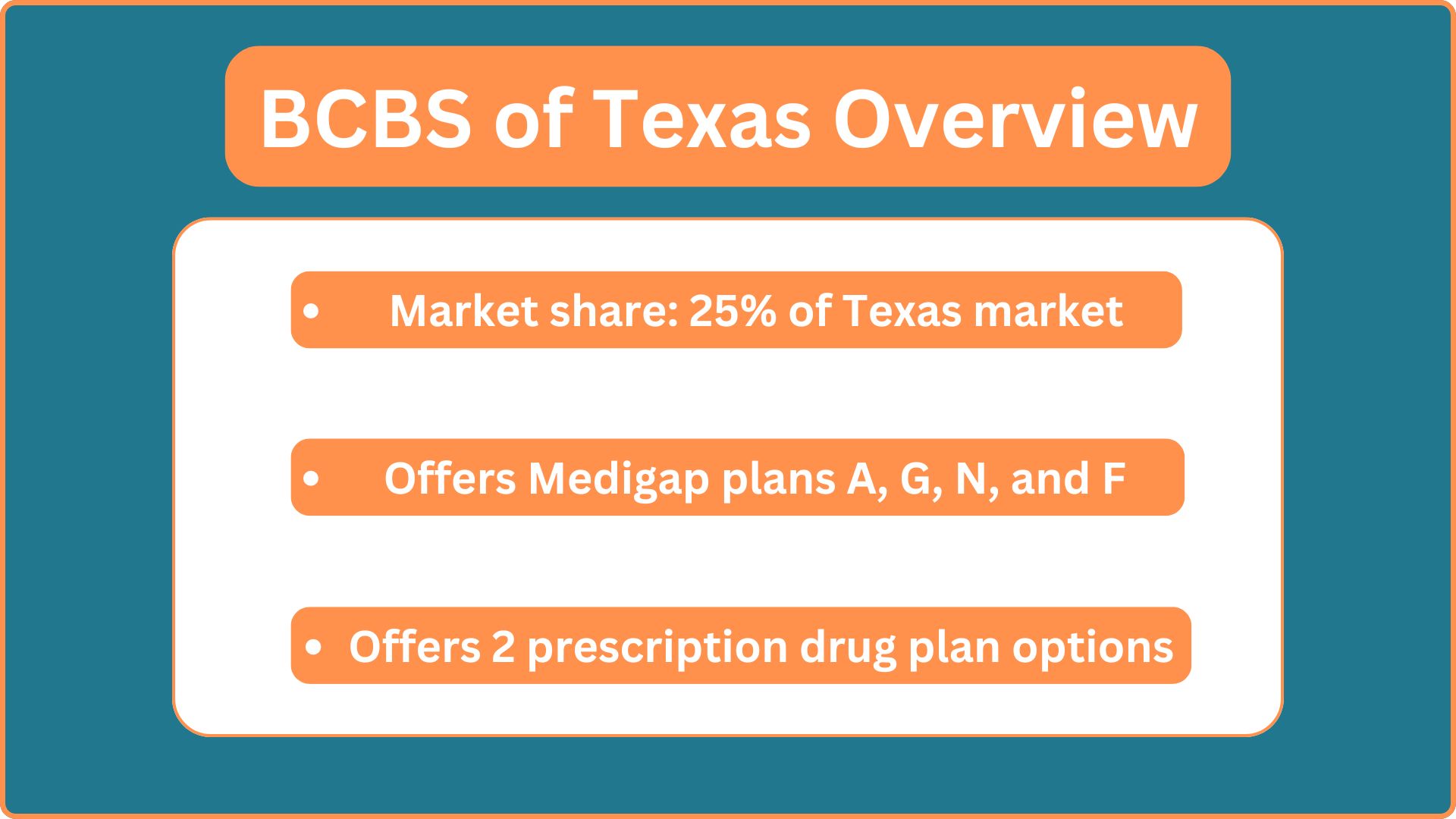

Blue Cross Blue Shield of TX Medigap: Overview

Let’s start off with just a brief overview.

Blue Cross Blue Shield of Texas has a very large market share of 25% of the overall health insurance market.

They offer Medigap plans A, G, N, and F. But as I mentioned before, I’m going to focus primarily on Plan G and N because Plan F is no longer available to new beneficiaries, and Plan A is seldom selected because of its limited benefits.

Blue Cross Blue Shield offers two prescription drug plan options, which is unique because most Medicare Supplement companies may only offer a Medicare Supplement plan and force you to pick up a drug plan with a different company.

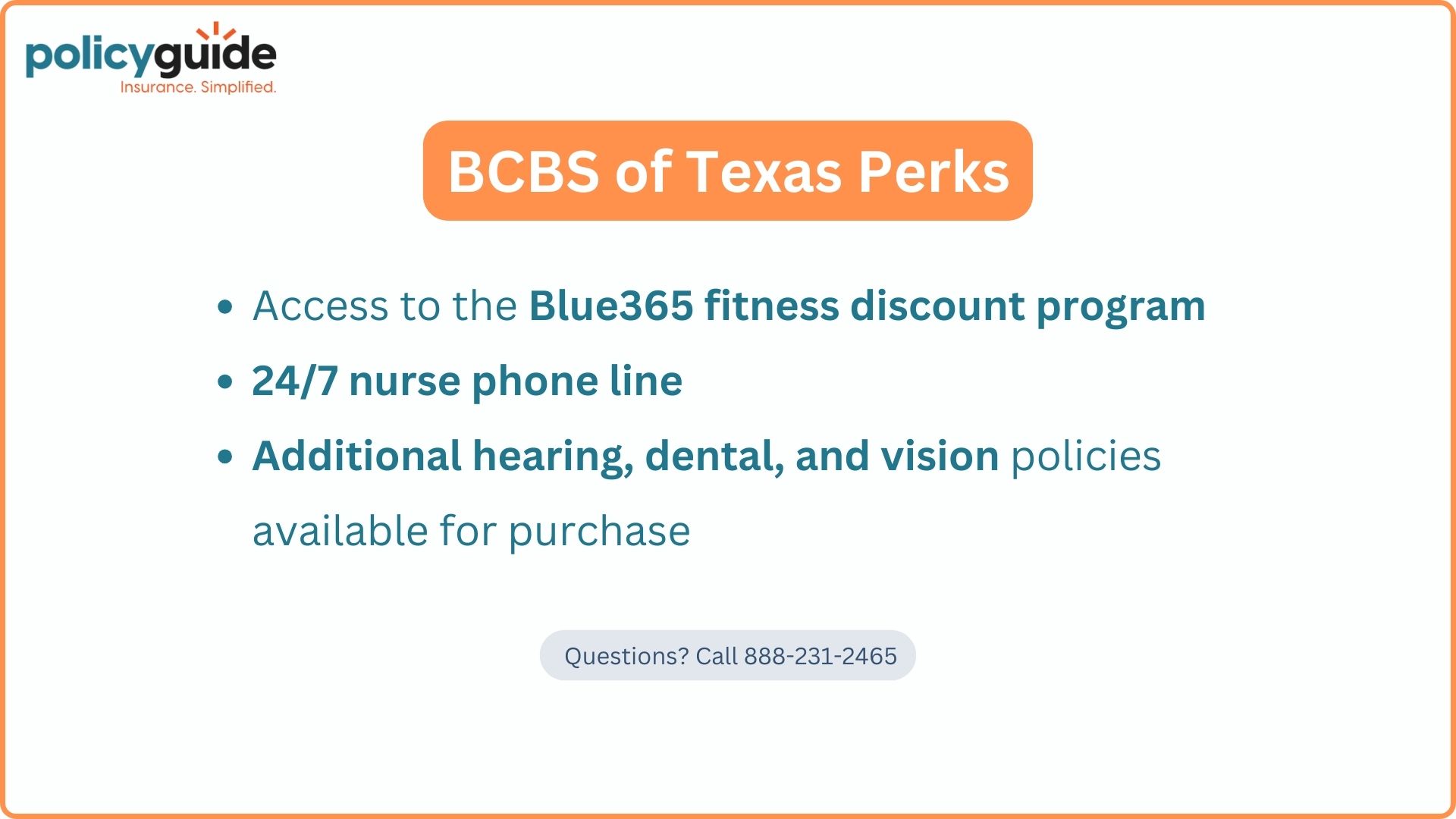

BCBS Of Texas: Perks

Next, let’s jump right into Blue Cross’s perks; they give you access to their Blue365 fitness discount program, offer a 24/7 nurse phone line, and offer additional hearing, dental, and vision policies available to purchase alongside your Medicare Supplement plan.

Now, I will show you some of the rates for Blue Cross Blue Shield’s Plan G and Plan N.

How Much Does Blue Cross Blue Shield of TX Medigap Cost?

We’ve got Plan G at about $160 per month and Plan N at around $130 a month. Keep in mind these are just their standard rates. I’ve not included their household premium discounts in my samples.

Note: I’m using a 65-year-old female in Dallas County, and she would also be a non-tobacco user.

Let’s take a look at Blue Cross Blue Shield of Texas’s Plan G and Plan N rates and how they stack up to a few other top medigap companies.

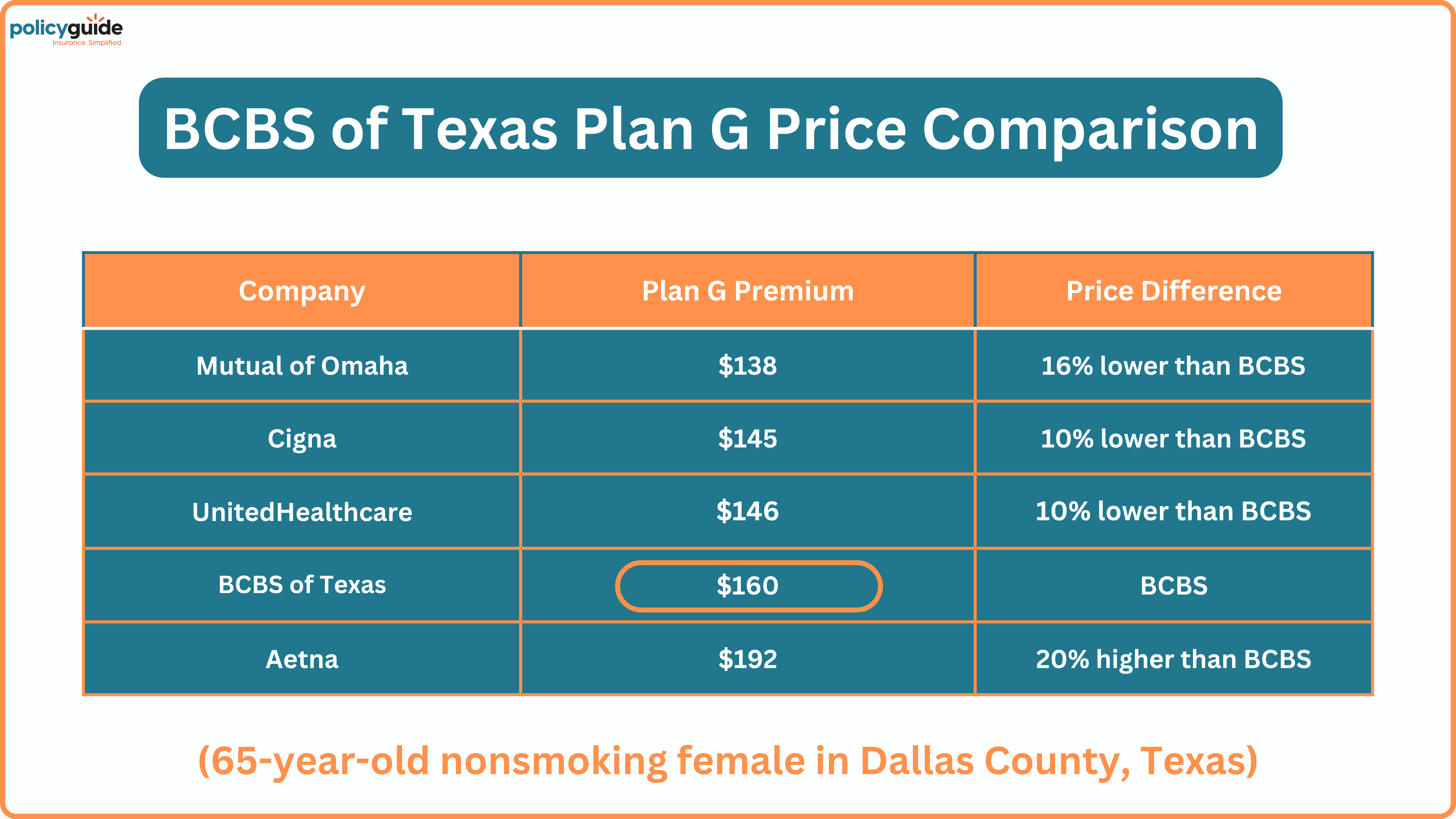

BCBS of Texas Plan G Premium Comparison

Below, I’ll compare the Plan G rates of BCBS against some top competitors. I chose Mutual of Omaha, Cigna, UnitedHealthcare, and Aetna.

As you can see:

Mutual of Omaha is coming in at $138 per month, roughly 16% lower than Blue Cross Blue Shield.

Cigna is coming in at $145, which is roughly 10% lower.

UnitedHealthcare is coming in at $146, also 10% lower than Blue Cross Blue Shield.

And then, obviously, we have our original Blue Cross of Texas quote at $160.

Last but not least is Aetna, coming in at $192, 20% higher than Blue Cross Blue Shield.

What Medigap Plan G Covers:

Medigap Plan G is one of the most comprehensive Medicare Supplement plans. It helps cover out-of-pocket costs that Original Medicare (Parts A and B) doesn’t pay for, such as:

- Medicare Part A Coinsurance & Hospital Costs – Covers the full cost of hospital stays after Medicare pays its share (up to 365 extra days).

- Medicare Part A Deductible – Covers the full Part A deductible ($1,676 in 2025).

- Medicare Part A Hospice Coinsurance & Copayments – Covers costs related to hospice care.

- Medicare Part B Coinsurance & Copayments – Covers the 20% of outpatient and doctor visit costs that Medicare doesn’t pay.

- Medicare Part B Excess Charges – Covers the extra 15% that some doctors charge above the Medicare-approved amount.

- Skilled Nursing Facility (SNF) Coinsurance – Covers SNF coinsurance costs from 21-100 days.

- Foreign Travel Emergency Coverage – Covers 80% of emergency medical costs outside the U.S. (up to plan limits).

- First 3 Pints of Blood – Covers the cost of the first three pints of blood in a medical procedure.

What Medigap Plan G Does NOT Cover:

While Plan G provides extensive coverage, it does not cover:

- Medicare Part B Deductible – You must pay the Part B deductible out-of-pocket ($257 in 2025).

- Prescription Drugs – It does not cover retail prescription drugs; you need a separate Part D plan.

- Routine Vision, Dental, and Hearing – No coverage for eye exams, glasses, dental work, or hearing aids.

- Long-Term Care (Custodial Nursing Home Care) – Does not cover extended nursing home stays or assisted living.

- Non-Medicare Approved Services – Any services that Medicare itself does not cover (e.g., cosmetic surgery, most acupuncture, etc.).

-

A Note About Aetna:

Aetna can sometimes be much more competitive, but company rates fluctuate year in and year out. A couple of years ago, Aetna was the most competitive in Texas. And now, they’re not.

That could change in future years, but as of right now, they tend to have one of the highest Plan G rates in Texas.

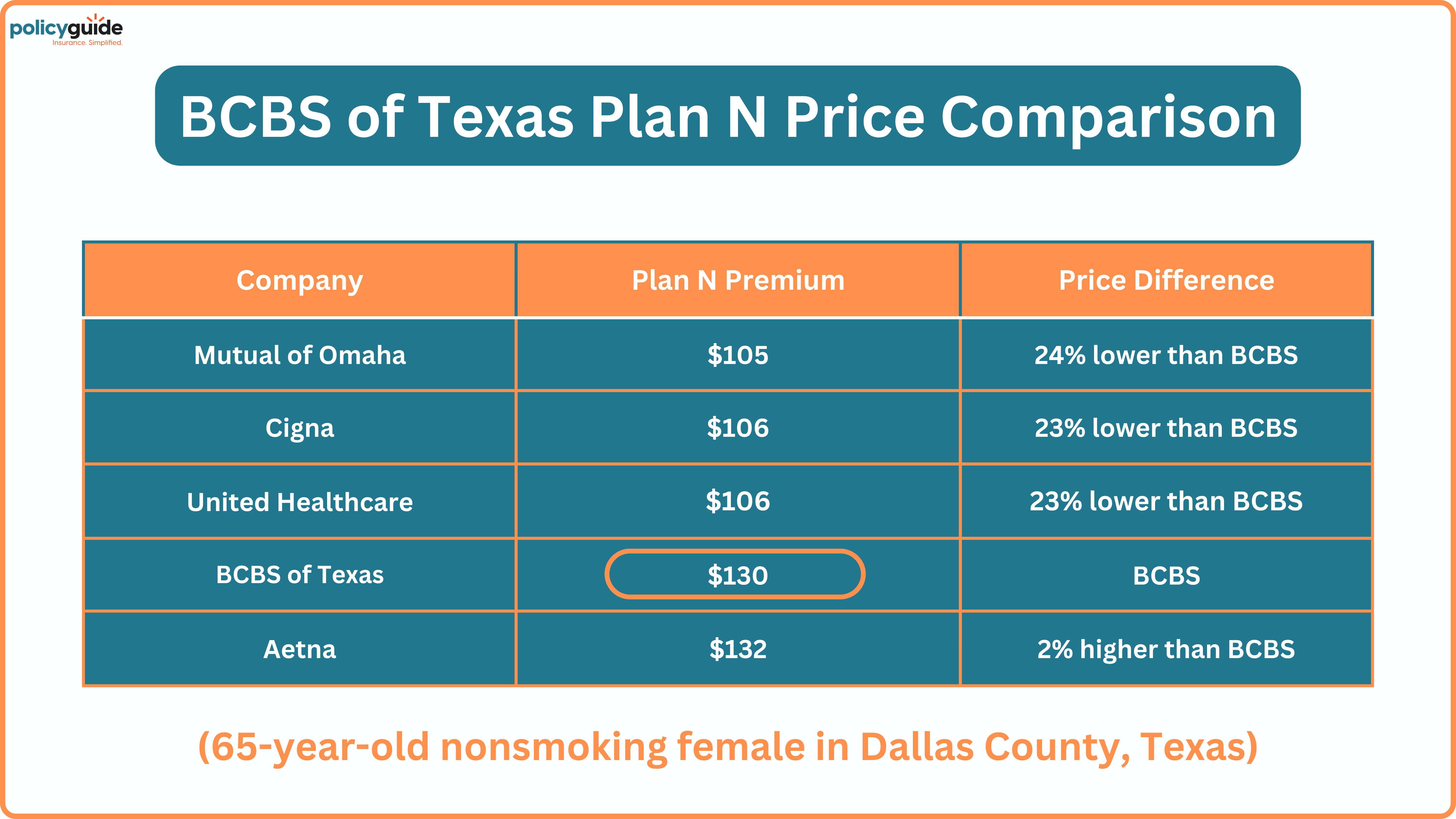

BCBS of Texas Plan N Premium Comparison

I’ve done the same thing for Medicare Supplement Plan N. So, let’s compare Blue Cross to the same companies.

Premium analysis:

Mutual of Omaha is coming in at $105 a month, 24% lower than Blue Cross Blue Shield.

Cigna is coming in at $106 a month, which is 23% lower.

United Healthcare is also coming in at $106, again 23% lower.

Of course, we have our original Blue Cross rate of $130.

And then Aetna is coming in at $132, which is only 2% higher.

What Medigap Plan N Covers:

- Medicare Part A Coinsurance & Hospital Costs – Covers the full cost after Medicare pays its share, including up to 365 extra days after Medicare benefits are exhausted.

- Medicare Part B Coinsurance & Copayments – Covers 100% of Part B coinsurance, except for small copays ($20 for doctor visits and $50 for ER visits that don’t result in inpatient admission).

- Blood (First 3 Pints) – Covers the cost of the first three pints of blood.

- Medicare Part A Hospice Care Coinsurance & Copayments – Fully covered.

- Skilled Nursing Facility (SNF) Coinsurance – Fully covered.

- Medicare Part A Deductible – Fully covered ($1,676 per benefit period in 2025).

- Foreign Travel Emergency – Covers 80% of emergency care received outside the U.S. (up to plan limits).

What Medigap Plan N Does NOT Cover:

- Medicare Part B Deductible – You must pay the annual Part B deductible ($257 in 2025).

- Medicare Part B Excess Charges – Not covered (Doctors who do not accept Medicare assignment can charge up to 15% more).

- Prescription Drugs (Part D) – Not included; you’ll need a separate Part D plan.

- Routine Dental, Vision, or Hearing Care – Not covered; requires separate private insurance.

- Long-Term Care (Custodial Nursing Home Care) – Not covered.

- Hearing Aids, Eyeglasses, and Routine Foot Care – Not included.

As you can see, Blue Cross Blue Shield of Texas seems to be in the middle when I compare it to these other companies.

So, as we progress in this article, I’ll show you what these other companies offer in addition to their premiums and what Blue Cross Blue Shield has to offer when you compare it to them.

Before I go there, I’ll highlight some strong points that Blue Cross Blue Shield of Texas is offering.

Blue Cross Blue Shield of TX: Premium Discounts

Let’s talk about premium discounts.

- BCBS has a spouse partner discount, which is 10%. This applies to policyholders who reside with a spouse or domestic partner.

- They also have what’s called Continuing with Blue discount of 7%. This applies to policyholders who were enrolled in a Blue Cross Blue Shield of Texas non-Medicare health plan prior to enrolling in a Blue Cross Blue Shield of Texas Supplement plan.

Now, here’s the deal if you are within one year of leaving a Blue Cross Blue Shield of Texas group or individual health plan:

- If you move to Medicare and then choose Blue Cross Blue Shield of Texas for your Supplemental plan, they’ll give you an additional 7% discount.

That is very unique to Blue Cross of Texas. No other company offers those types of premium discounts in Texas.

- Lastly, in terms of the premium discounts, they have what’s called a 12% Blue family discount. This applies to policyholders who meet the criteria for both the spouse discount and the Blue discount I just referenced.

That’s a big takeaway. Blue Cross Blue Shield of Texas offers far superior monthly premium discounts to the four other companies I listed.

The other companies also have discounts, which I’ll get to soon. But none have stackable discounts like Blue Cross Blue Shield of Texas’ offering. So, that would give you additional savings on the original premiums that I quoted you earlier.

BCBS of Texas vs. Other Medigap Providers

Now, let’s talk about how Blue Cross compares to these other four carriers.

You could call it a pros-and-cons comparison or just a comparison of these four other companies. I’ve created a chart that will quickly show you what features each company has when compared to Blue Cross Blue Shield of Texas.

We’ve got all the companies listed and whether they offer premium discounts, dental, vision, and hearing plans (again, those come at an additional premium), and prescription drug plans (also require an additional premium).

In these comparisons, we’re also looking at market longevity and Plan G pricing. So, starting with Blue Cross Blue Shield of Texas, we’ve discussed their premium discounts. They also have add-on dental, vision, and hearing plans and two prescription drug plans that you can add to your Medicare Supplement.

Their market longevity is probably the longest in the state because they have such a large footprint in the Medicare, group, and individual under-65 space. As I mentioned before, their premium for Plan G is $160 per month.

BCBS of TX vs. Mutual of Omaha

Mutual of Omaha offers an additional benefit rider for Medicare Supplement plans that give discounts on specific health services, along with household discounts of up to 12%. They also offer a fitness membership called Mutually Well, similar to SilverSneakers. Their Plan G premium is only $138 compared to Blue Cross’s $160.

However, Blue Cross Blue Shield of Texas has been in the state for a long time. They offer many premium discounts and added features, and their market longevity is the longest. So, their focus is not on trying to be the most competitive in the premium. Yes, they want to be competitive, but they’re also trying to be well-rounded with all of their offerings.

BCBS of TX vs. Cigna

Moving on to Cigna, we do see some premium discounts. We do see dental, vision, and hearing plans that could be added on. They do have prescription drug plans, but that varies by state.

Like Blue Cross, their market longevity is very solid. And they’re coming in at $145 per month for Plan G.

BCBS of TX vs. UnitedHealthcare

UnitedHealthcare does require a membership with AARP. The standard rate is $20 per year.

They also offer dental, vision, and hearing options and prescription drug plans in most states. Their market longevity is very long, one of the longest in the industry.

UnitedHealthcare has the largest membership of Medicare Supplement clients throughout all of the states. Their membership rivals all other companies combined, and they’re coming in at $146 for Plan G.

BCBS of TX vs. Aetna

Last on my list is Aetna. We do see some premium discounts. We do see dental, vision, and hearing options. Some states do have prescription drug plans.

Their market longevity is also very trustworthy. They’ve been at it for many, many years. However, their Plan G premiums are lacking, coming in at $192 per month.

In Summary:

Blue Cross premiums are in the middle of the road with many offerings.

Mutual of Omaha tends to have lower premiums with good discounts and benefits.

Cigna and UnitedHealthcare would be the next closest to the well-rounded features that Blue Cross Blue Shield of Texas offers.

Aetna is a very good company with very good offerings, but at this time, it is just not very competitive with their premiums.

So the last topic we’ll discuss is Medigap rate increases – let’s jump in.

Blue Cross Blue Shield of TX Medigap: Rate Increases

Here’s everybody’s favorite question:

You show me how low the rates are, but how long is that going to last?

Well, here’s the short and long answer. Historically speaking, Blue Cross Blue Shield of Texas’s average rate increase has been between 3%-5% per year, leading up to about 2023.

In 2023, Medicare Supplement rate increases have been higher for all companies in all states due to the COVID-19 pandemic. Here’s what happened.

During the COVID pandemic, people delayed non-emergency care. When quarantine and the pandemic quieted down and things got back to normal, there was a large influx of people that rushed out to get non-emergency-related care done.

That drove the premiums up basically for all companies. And there’s about a one to two-year lag with those rate increases happening.

In 2024, rate increases varied from 7% to 10% to as high as 19%, depending on the plan and the company.

-

There's Hope!

The hope is that within the next year or two (when those claims calm down), we will get back to the 3%- 5% average rate increase.

Pros and Cons of Blue Cross Blue Shield of Texas (BCBS TX) Medigap Plans

I know I have covered a lot in this article, but I wanted to leave you with a quick recap of the pros and cons of BCBS TX Medicare Supplement plans.

Pros

-

Strong Market Presence & Stability

BCBS TX holds a 25% market share, making it one of the most stable and reliable Medigap providers in Texas.

Long history in the Medicare, individual, and group insurance markets.

-

Comprehensive Plan Offerings

Offers Medigap Plans G, N, A, and F (for those eligible before 2020).

Includes two prescription drug plan (Part D) options, unlike many competitors.

-

Competitive Discounts

10% Spouse/Partner Discount – If living with a spouse or domestic partner.

7% Blue Discount – If transitioning from a BCBS TX group or individual plan within a year.

12% Blue Family Discount – Combination of the two discounts above, offering one of the best discount structures in Texas.

-

Extra Perks

Access to Blue365 fitness discount program.

24/7 nurse line for health-related questions.

Option to purchase dental, vision, and hearing coverage.

-

Reasonable Rate Increases (Pre-Pandemic)

Historically, 3%-5% average annual rate increases, which is on the lower end compared to competitors.

While 2024 saw higher increases (7%-19%) due to post-pandemic claim surges, rates are expected to stabilize.

-

No Network Restrictions

Like all Medigap plans, BCBS TX allows you to see any doctor or hospital that accepts Medicare – no referrals or prior authorizations required.

Cons

-

Higher Premiums Compared to Some Competitors

The premiums for Plan G ($160/month) and Plan N ($130/month) are higher than those of some competitors, such as Mutual of Omaha ($138 and $105, respectively) and Cigna ($145 and $106, respectively).

While not the highest, BCBS TX is not the cheapest option.

-

Rate Stability Concerns

Recent post-pandemic rate hikes (up to 19%) in 2024 have caused uncertainty in pricing stability.

Future increases expected to return to 3%-5% annually, but not guaranteed.

-

No Coverage for Part B Deductible, Drugs, or Routine Care

Like all Medigap plans, BCBS TX does not cover the Medicare Part B deductible ($257 in 2025).

Prescription drugs, routine dental, vision, and hearing care require separate policies at an additional cost.

-

Not the Absolute Cheapest Option

If you’re looking for the lowest possible premium, Mutual of Omaha offers Plan G at $138/month and Plan N at $105/month, both significantly lower than BCBS TX.

-

Less Competitive for Those Who Don’t Qualify for Discounts

While BCBS TX offers stackable discounts, those who don’t qualify will be paying higher base premiums compared to competitors like Mutual of Omaha or Cigna.

My Thoughts

- Best for: Those looking for a stable, well-rounded Medicare Supplement plan with strong discounts, extra perks, and long-term market presence.

- Not ideal for: Those who want the absolute lowest monthly premium and don’t care about additional benefits.

Because of all the perks Blue Cross Blue Shield of Texas offers, they are still a popular option, even though rates can be slightly higher.

Why Medigap Wins

Rate increases are unavoidable with Medicare Supplements. Yes, that’s true. However, keep in mind that a Medicare Supplement is the most superior option on the market.

It is far better than Medicare Advantage, which presents issues like:

- Referral requirements

- Network restrictions

- Prior authorizations (delayed care)

- Plan changes

- Doctors and hospitals leaving networks

There are many moving parts in Medicare Advantage. They’re lower cost per month, and you don’t deal with these rate increases, but you have far less comprehensive coverage, and you have far less freedom and flexibility.

You have more rules, more changes, and more surprises on Medicare Advantage.

So despite the rate changes, Medicare Supplement is still the Cadillac superior option.

I hope this has been informative. If you have questions, feel free to call us directly. We can do a needs analysis, gathering your information, including your age, your county, your preferences, what type of plan you’re looking for, and your budget.

Are you new to Medicare? We will then look at these different companies based on your circumstances.

If you have questions about anything I’ve discussed today, feel free to give us a call. We would be happy to help. Thanks!

FAQs

- When can I enroll in a BCBS TX Medicare Supplement plan?

- Can I be denied coverage for a BCBS TX Medicare Supplement plan?

- Do I need to renew my BCBS TX Medicare Supplement plan every year?

- What happens if BCBS TX discontinues my Medicare Supplement plan?