Cigna's Cutting Medicare Advantage in 2025: Who's at Risk?

If you are currently on a Cigna Medicare Advantage plan and live in the state of Florida, I have some important news to share with you.

During this upcoming Medicare Annual Election Period, Cigna (one of the biggest names in the Medicare industry) is not renewing some of its Medicare Advantage plans with the federal government.

This change could impact up to 6,000 people in the state of Florida.

So, if you have a Medicare Advantage plan with Cigna, you should keep a close eye on your mailbox for this change notification, which you should be receiving any day now.

Each year, all Medicare Advantage companies are required to send an ANOC (or Annual Notice of Change). This simply lists changes to your Medicare Advantage plan for the upcoming year. Unfortunately, most people do not notice this letter because they’re happy with their current coverage and throw it away.

This year is different. Definitely look for that letter, as it could be a non-renewal notice instead of an Annual Notice of Change.

As a reminder: the Annual Election Period runs from October 15th through December 7th. That is when you will want to find a replacement should you receive a notification that your plan is not renewing

I’ve been helping people understand Medicare and the system’s complexity for over 15 years. Today, I want to share with you some of the information that we’re seeing coming from Cigna and how it pertains to certain states with Medicare Advantage plans.

Cigna's Announcement

Take a look at this statement I pulled from an article that Healthcare Dive did on the Cigna changes:

“Every year, Cigna Healthcare Medicare evaluates service areas for viability, network adequacy, and provider engagement.

If any gaps are identified in these areas that cannot be resolved, it can result in Cigna Healthcare reducing these service areas and/or not renewing the plans.”

*All of the information I provide on this page, I’ll put a link in the sources below so you can read the full articles.

Now we’re all asking: why is this happening?

Why Is This Happening?

Cigna is not able to sustain the medical loss ratio, or claims amounts in certain areas of the country where people have their Medicare Advantage plans. Cigna (and all Medicare Advantage companies) receive a reimbursement rate from the federal government for every member they’ve enrolled.

When they receive that amount, it helps them:

- Maintain the plan

- Set up the network

- Pay the claims

They’re receiving that money from the federal government, and then they’re paying a lot out in medical claims when you use your plan.

We’re seeing this happen all over the country with companies including Aetna, Cigna, and Humana. 2025 is going to be very turbulent for the Medicare Advantage space.

Companies are claiming that they’re spending too much on medical care versus how much they’re receiving from the federal government.

So they’re looking at smaller areas where plans are struggling to be profitable, and they’re choosing not to renew those plans.

Unfortunately, this article really is heavily weighted on the state of Florida.

Which Members Will Be Affected?

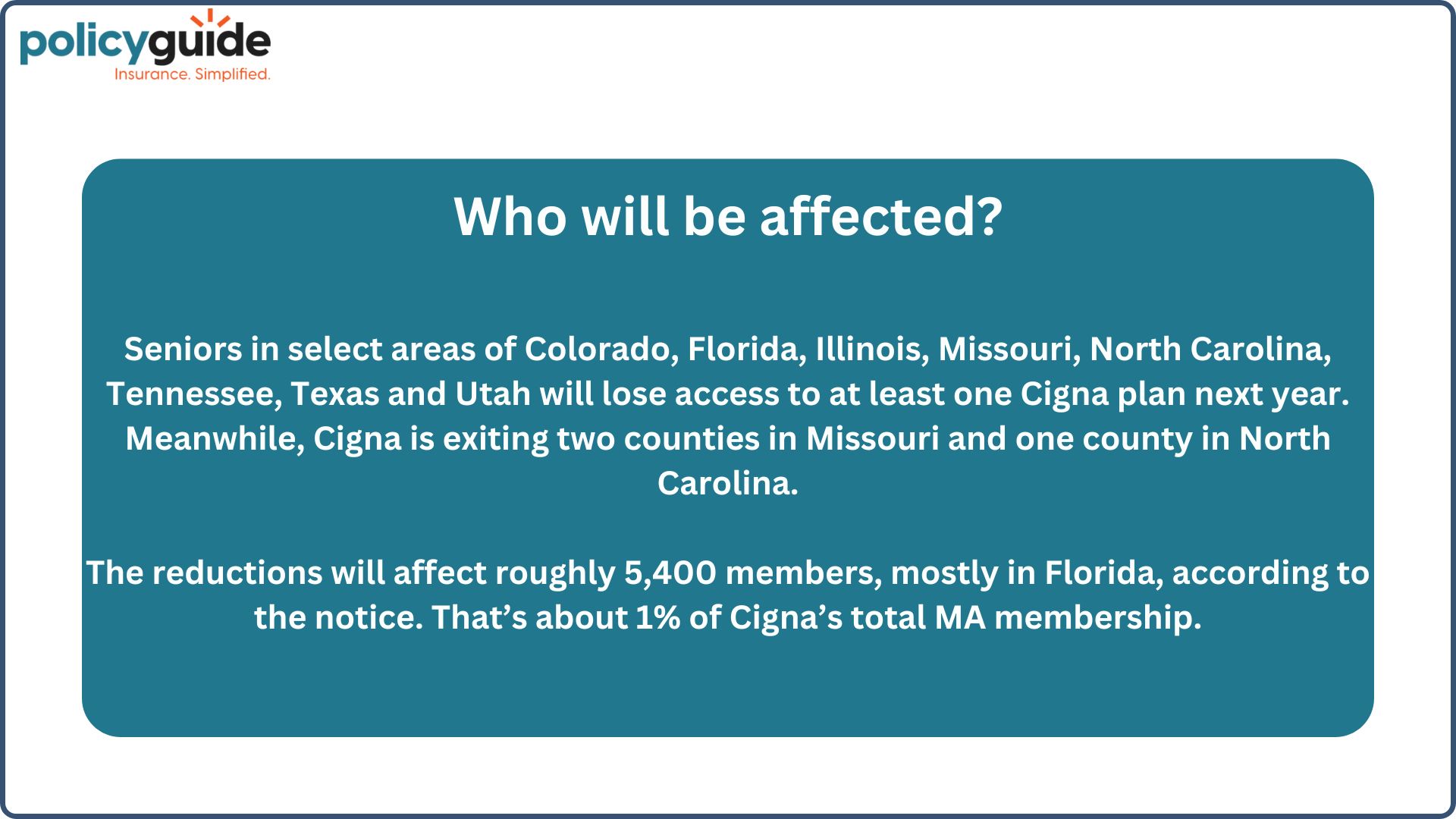

Seniors in select areas of the below states will lose access to at least one Cigna plan next year:

- Colorado

- Florida

- Illinois

- Missouri

- North Carolina

- Tennessee

- Texas

- Utah

According to the notice, the reductions will affect roughly 5,400 members (mainly in Florida).

That’s about 1% of Cigna’s total Medicare Advantage membership.

Now, in all of these states I just listed, it doesn’t explicitly say that they’ll be losing plans or not renewing; it just means they’ll have fewer Cigna plans to choose from.

It looks like the all-out reduction is heavily focused on the state of Florida, with 5,400 members (and potentially more) being affected.

We’ve been in the Medicare space for 15 years, teaching people about Medicare and helping them select the right plan.

This is not new. This comes as no surprise to me, unfortunately.

Companies have been flooding the Medicare Advantage market as baby boomers age into the system, basically to try to get a piece of the pie.

Many companies are finding that they overextended their reach or put too much emphasis on it. With the medical loss ratio, their profits are not in line to be satisfactory for their stockholders.

You have really two avenues, and next, I’ll tell you how to be prepared.

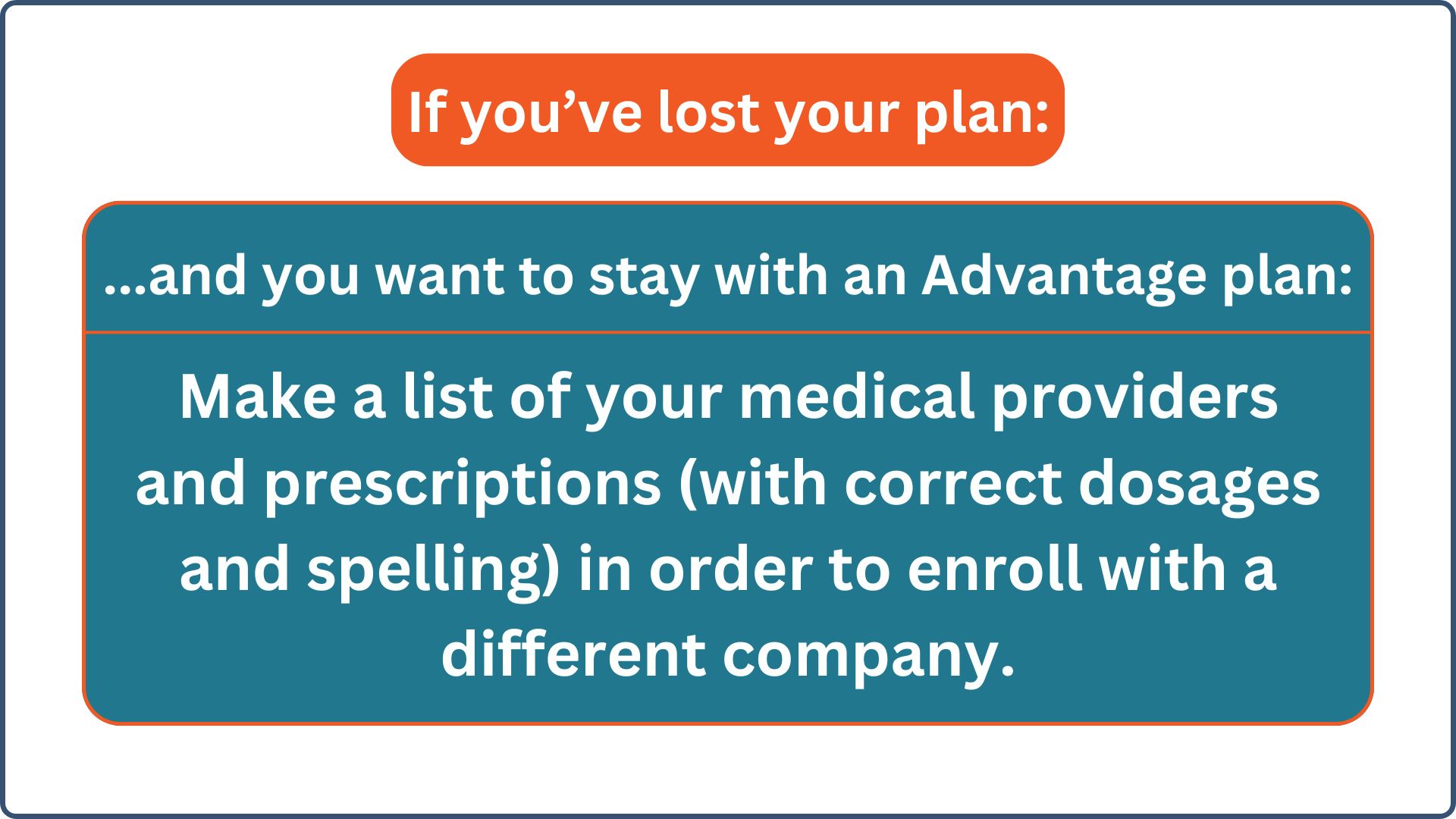

Option #1: Switching Advantage Plans

If you are losing your plan and you want to keep a Medicare Advantage plan: make a list of your doctors, hospitals, medical providers, and prescriptions.

When you create your list of prescriptions, make sure you get the correct spelling of the prescription names (we all know prescription names are very wonky sometimes) and include the correct dosage.

This way, when you go to try to find another plan, let’s say you’re looking at Florida Blue or UnitedHealthcare or whomever it may be, the key information is:

- Make sure that the new company will cover all of your existing providers in-network, and

- All of your prescription medications will be covered on that new company’s formulary list.

Finding another Medicare Advantage plan in Florida should not be a hard task. Florida has the most companies offering Medicare Advantage plans.

Option #2: Switching to a Medigap Plan

Now, here’s a silver lining in all of this: if you lose your plan, through no fault of your own, that creates a guaranteed issue right.

What does that mean?

That means if you lose a Medicare Advantage plan, you can now enroll in a Medicare Supplement (also called a Medigap) plan and bypass medical health questions.

Maybe you’ve wanted to switch to a Medicare Supplement plan in the past, but when you apply, they have health questions, and maybe you have pre-existing conditions.

They may have denied you coverage because you couldn’t pass medical underwriting.

Well, this is going to give you a golden ticket.

A guaranteed issue ticket that says, “I’ve lost my Medicare Advantage plan. I want a Medigap plan. Therefore, I do not have to answer those medical questions”.

Remember: Medicare Advantage is more managed care, with networks, referrals, and prior authorizations. Yes, it’s a lower monthly cost, but it does come with a rule book.

Benefits of Medicare Supplement Plans

When you move to a Medigap plan, you’ll have:

- No provider networks

- No required referrals

- No disputes between the insurance company and the providers

You also will not deal with this government reimbursement rate (like you do with Medicare Advantage) when you’re on a Medigap plan.

Last but not least, probably the most important thing is:

- When you switch to a Medigap plan, you no longer have to deal with prior authorizations.

All Medicare Advantage plans have prior authorizations, but Medigap plans have none. Eliminating those prior authorizations will speed up your access to care and reduce delays.

Medigap plans do come at a higher monthly cost, yes, but they are far superior coverage.

-

Important to know:

- If you pick a Medicare Supplement plan, you will also need to add a prescription Part D plan because, unlike Medicare Advantage, Medicare Supplement does not automatically cover prescriptions.

Final Thoughts

If you choose to pick another Medicare Advantage plan: have your list of doctors, hospitals, and prescriptions ready.

If you choose to switch to a Medicare Supplement plan: you don’t need the list of providers because Medicare Supplement (or Medigap) has no provider network, so you can essentially go wherever you want.

I hope that this information has been helpful and that I’ve given you some resources to prepare should you receive one of these letters. If you have questions or need help picking a plan, we’re here and happy to help.

Thanks!

Source: Healthcare Dive

FAQs

- What should I do if my Cigna Medicare Advantage plan is discontinued in my area?

- What is a guaranteed issue right, and how can it benefit me?

- How do Medigap plans differ from Medicare Advantage plans?