Medicare Advantage Changes 2025: Humana, Cigna, & Centene

As millions of Medicare beneficiaries approach the 2025 Annual Enrollment Period (October 15th to December 7th), the Medicare Advantage market is facing significant disruptions.

Major players, including Humana, Cigna, Centene, Premera Blue Cross of Washington, and Blue Cross of Kansas City, are dropping Medicare Advantage members, leaving many seniors reevaluating their coverage options.

This all pertains to Medicare Advantage – if you have a Medicare Supplement with any company, that is not going to change.

This is exclusively directed at Medicare Advantage members.

Important: Check Your Mail

The first thing you’ll want to do this year is check your mail for your Annual Notice of Change (ANOC). This letter will detail any changes to your current plan benefits (if your plan is renewing in 2025), such as:

- Copays

- Coinsurance

- Premium differences

But more importantly, check your mail for a notification that your Medicare Advantage plan will not be renewed in 2025. This is different than the Annual Notice of Change, which simply tells you about minor benefit tweaks for the new year.

A non-renewal notice means that whatever Medicare Advantage plan you have in 2024 may not automatically renew once we hit January 1st, as you’ve experienced in previous years.

Update: If you have received notice that your plan is changing or ending, please call us to find an alternate option: 888-414-4547

Which Companies Are Terminating Plans?

To name a few, big companies like Aetna, Cigna, Humana, and Centene may be reducing benefits for the 2025 year, but more importantly, they have come out publicly stating that they will not be renewing thousands of plans throughout the United States.

Again, check for those notifications to see if you are one of the individuals affected by these plan terminations. Do not automatically assume that your plan will just renew into the new year as it has in the past.

Why is 2025 going to be so much different than past years?

Why Is 2025 So Different?

Well, I believe it comes down to two things:

#1. If you look at a lot of the news headlines, there’s big talk about huge disputes between Medicare Advantage companies and hospitals and medical providers not agreeing on reimbursement rates.

#2. Then you also have the medical loss ratio that insurance companies have to work with, coupled with a lower reimbursement rate from the federal government.

It’s almost like the perfect storm is happening. These companies are saying that the money they’re being reimbursed from the federal government for the 2025 calendar year is not enough to match the amount of money that they’re paying out in claims.

These big companies are looking at all of the country’s lower-performing areas to determine which plans are not profitable. Unfortunately, that’s just the reality of it.

So, who will be affected by this change?

Who Will Be Affected by This Change?

This change will occur across many different states, but generally speaking, larger states, like Florida, Texas, and California, could experience the biggest impact because they have the highest enrollment.

It’s rumored that over 100,000 people in Florida alone will not have a plan renew automatically for the 2025 year.

Let’s take a look at some of these news articles and actual screenshots I took from the home pages of some of these insurance company websites.

- Note: I’ll provide resource links at the bottom of this page so you can read the entire articles. I’m simply going to show you some snippets from each company so you can be aware of these notifications.

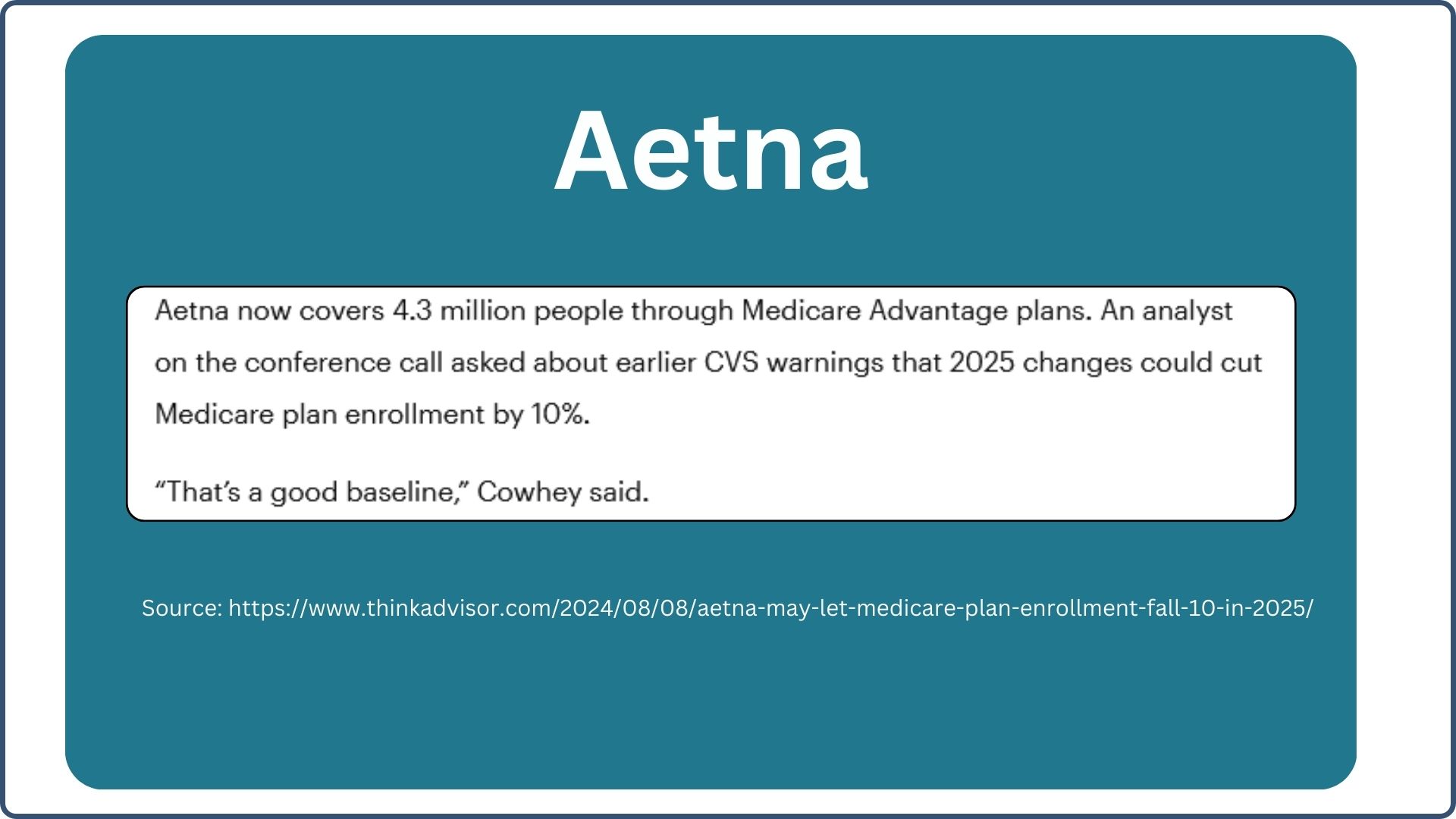

Let’s start with Aetna.

“Aetna now covers 4.3 million people through Medicare Advantage plans. 2025 changes could cut Medicare enrollment by 10%.”

And the CFO, Mr. Cowhey, said, “That’s a good baseline”.

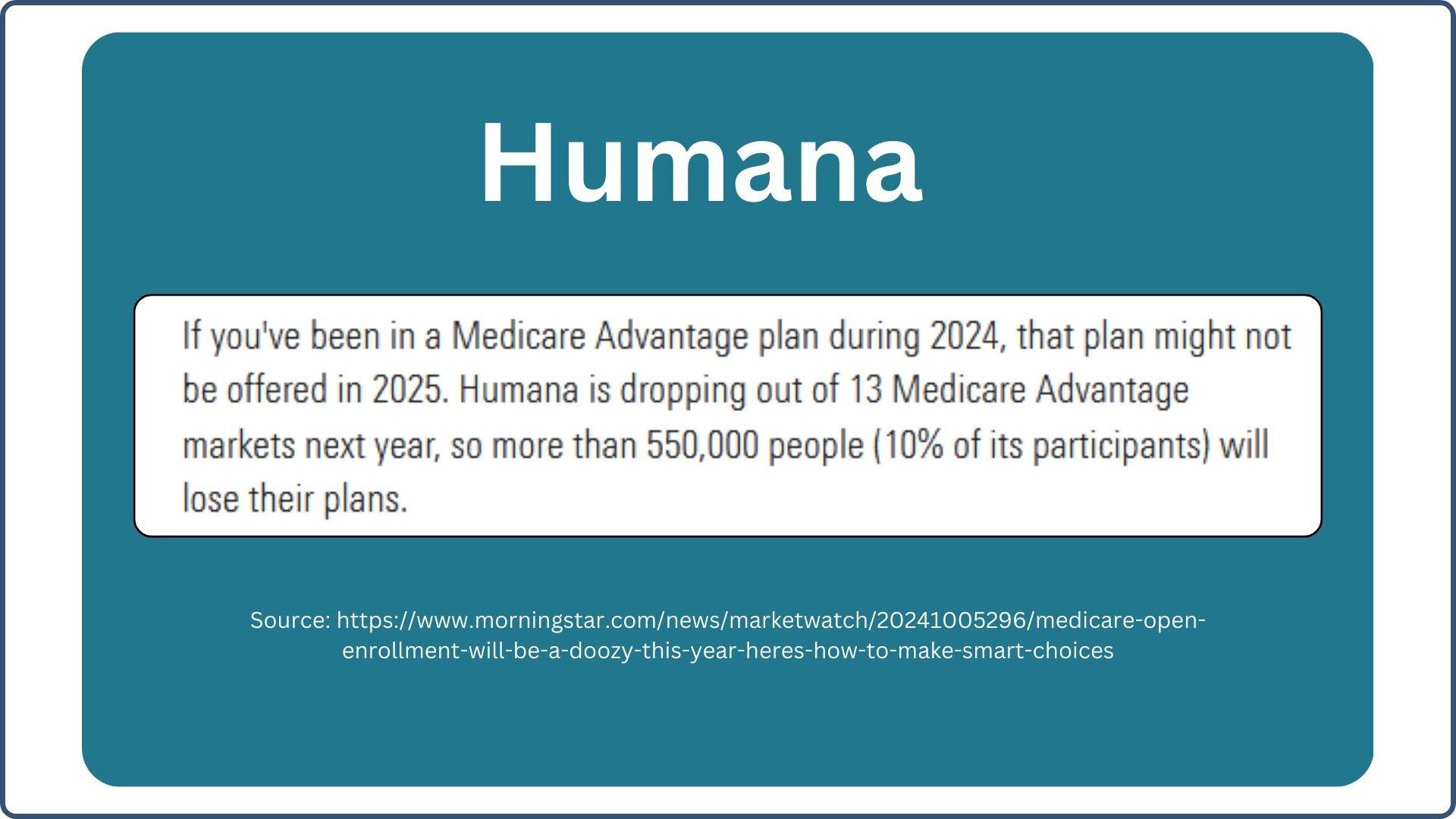

Let’s move on to Humana.

“If you’ve been on a Medicare Advantage plan during 2024, that plan might not be offered in 2025.

Humana is dropping out of 13 Medicare Advantage markets next year, so more than 550,000 people, or roughly 10% of its participants, will lose their plan.”

This is an article taken from morningstar.com that I linked in the sources below.

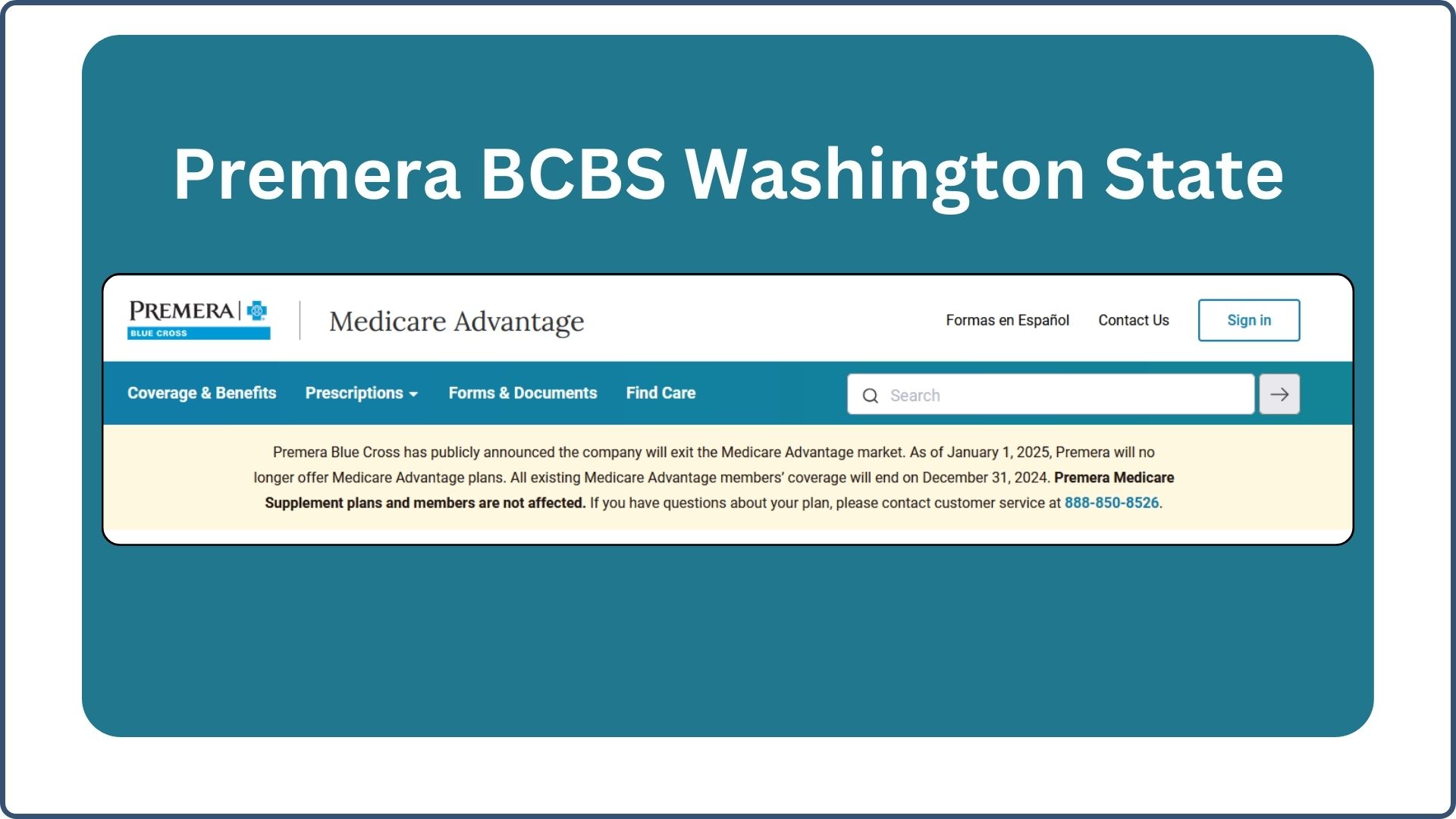

Next, I went directly to the Premera Blue Cross Blue Shield of Washington State website.

“Premera Blue Cross has publicly announced the company will exit the Medicare Advantage market.”

That’s a big one. I believe up to 40,000 people in the state of Washington will have no Medicare Advantage options with Premera.

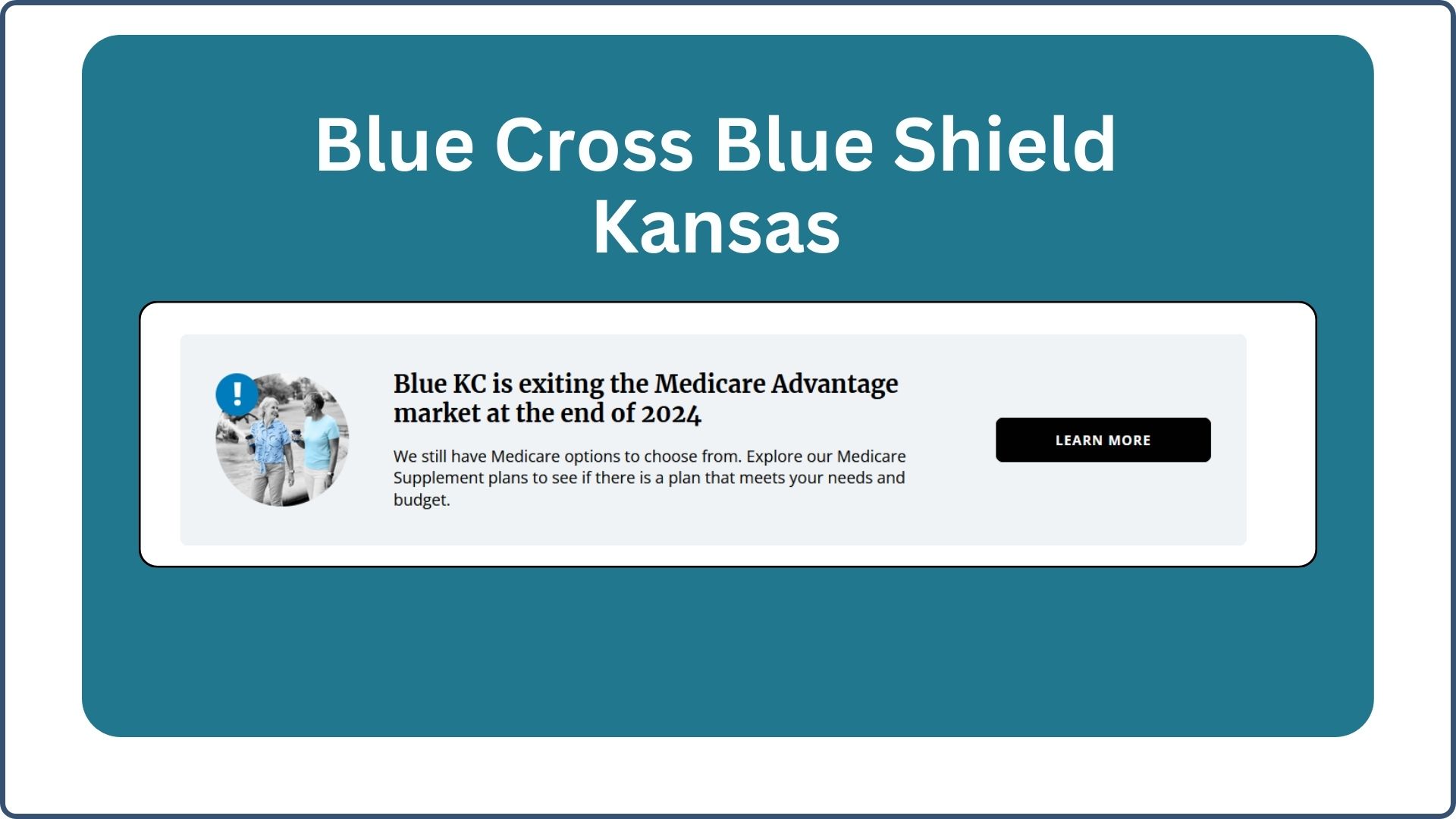

It’s the same problem with Blue Cross Blue Shield of Kansas City.

“Blue KC is exiting the Medicare Advantage market at the end of 2024. We still have Medicare options to choose from.

Explore our Medicare Supplement plans to see if a plan meets your needs and budget.”

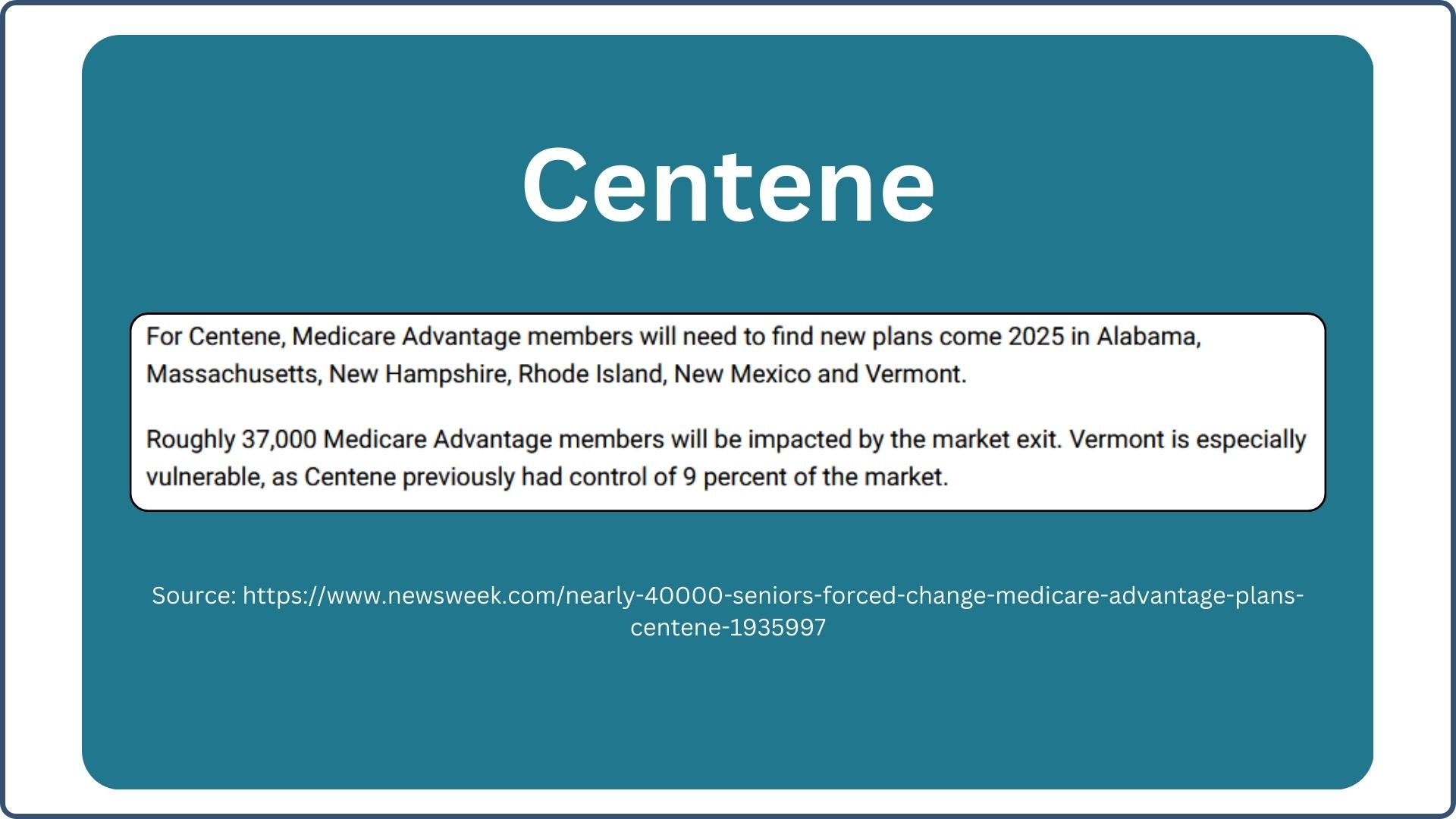

Centene is another one that is dropping almost 40,000 people across several states. Let’s take a look.

“For Centene, Medicare Advantage members will need to find new plans come 2025 in Alabama, Massachusetts, New Hampshire, Rhode Island, New Mexico, and Vermont.

Roughly 37,000 Medicare Advantage members will be impacted by the market exit. Vermont is especially vulnerable, as Centene previously had control of 9% of the market.”

So, what they’re saying is that the biggest disruption with Centene will be in the state of Vermont.

What to Do Next?

Here are a few tips and recommendations for what you can do if you do receive a notification that your plan is not renewing.

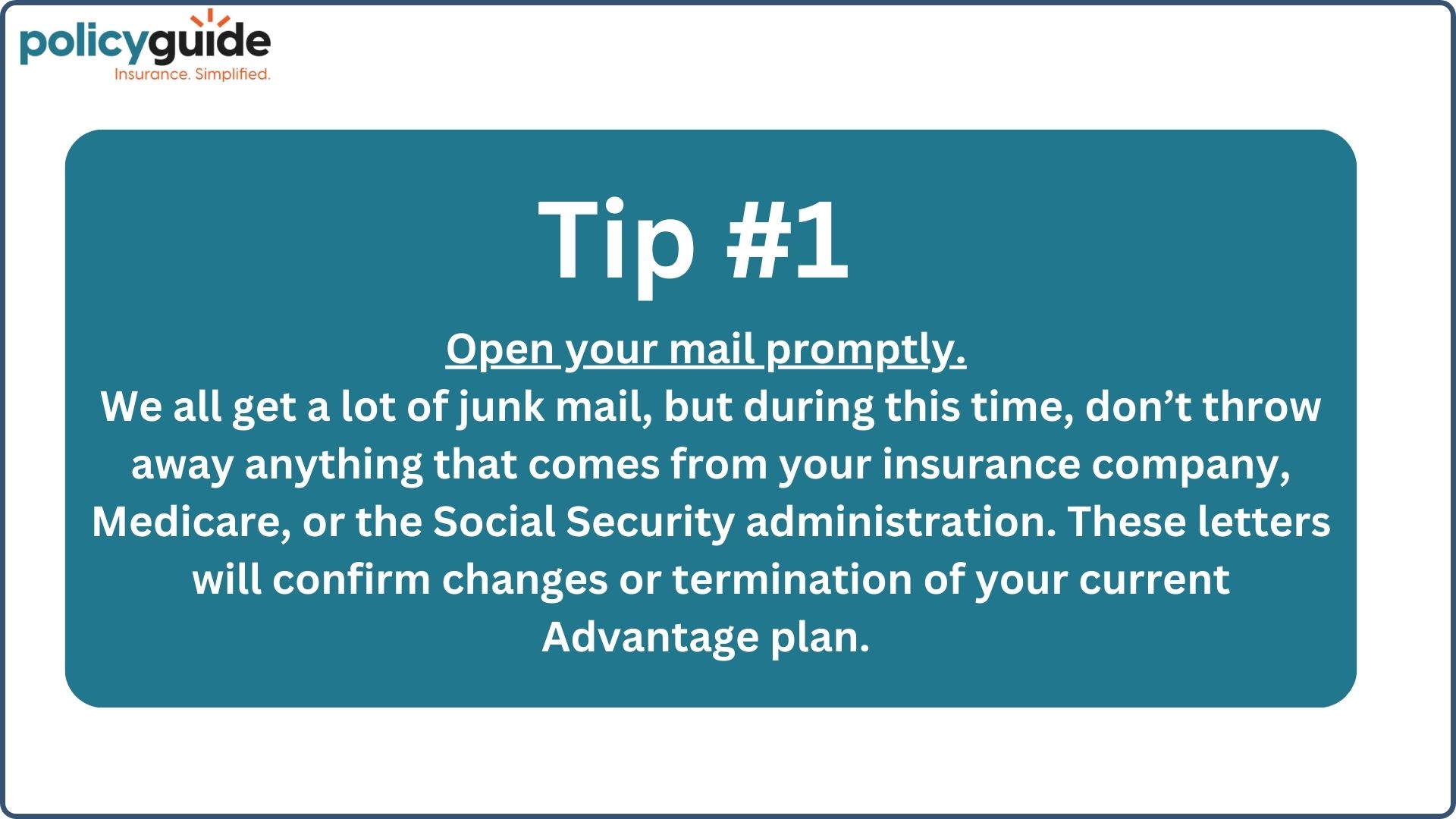

Tip #1: Open your mail promptly

I know that we all get a lot of junk mail every day. I highly recommend not throwing anything away that concerns your insurance company, Medicare, or the Social Security Administration.

These letters will confirm changes or terminations of your current Medicare Advantage plan.

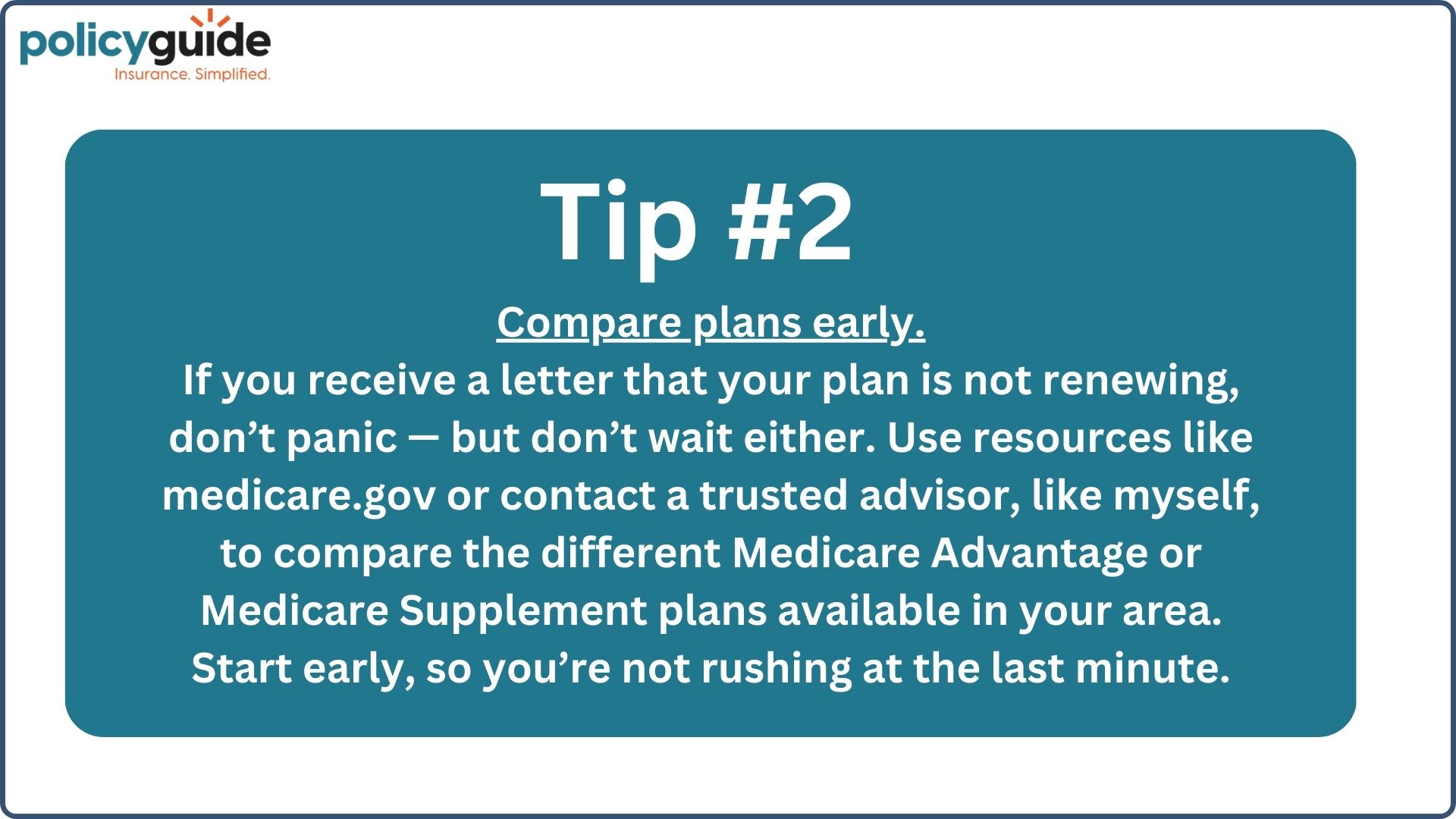

Tip #2: Don’t panic

If you receive a letter that your plan is not renewing, do not panic, but also don’t wait.

Use resources like Medicare.gov or contact a trusted advisor like myself to compare the different Medicare Advantage or Medicare Supplement plans available in your area.

Again, start this process early, so you’re not rushing at the end of the Annual Enrollment Period.

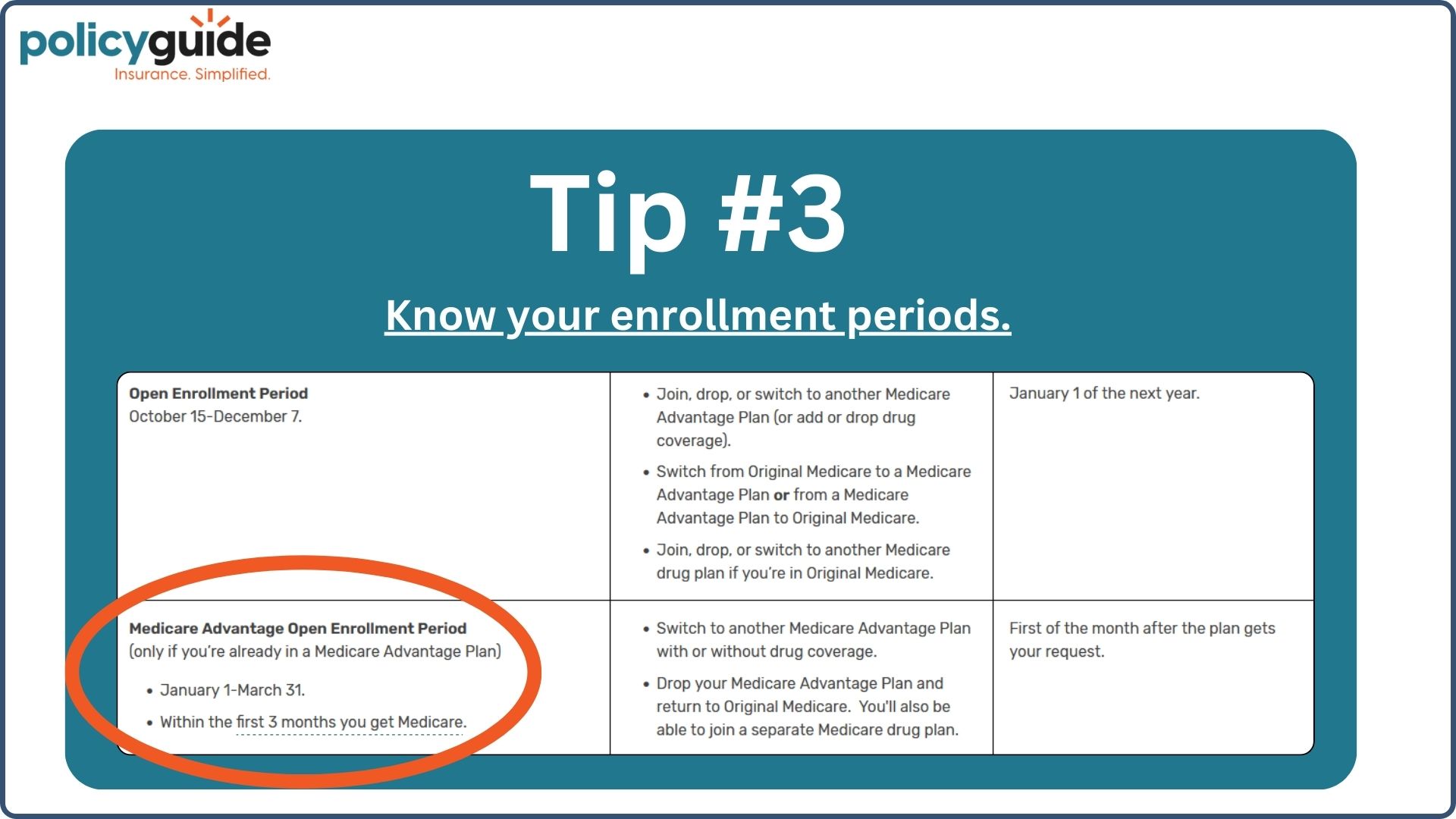

Tip #3: Know your enrollment periods

Should you experience loss of coverage, the most common enrollment period to change is during the Annual Open Enrollment Period, which runs from October 15th through December 7th.

You also have the Medicare Advantage Open Enrollment Period, which runs from January 1st to March 31st if you want to go from one Medicare Advantage plan to another.

Switching to Another Medicare Advantage Plan

So, if you’ve lost your plan and want to stay with a Medicare Advantage plan, make a list of:

- Your medical providers and hospitals

- Your prescription medications (including proper spelling and dosage)

That way, when you go to compare plans, you’ll have the most information that pertains to your individual situation to make sure that another company will cover all of your providers in-network and cover your needed prescriptions on their formulary list.

Switching to a Medigap Plan

Now, there is a silver lining opportunity in all of this chaos.

If you lose your plan and want to switch to a Medicare Supplement plan (because your Advantage plan will not renew), you will now have a guaranteed issue rights period.

What does that mean? That means you’ll receive a period of time where you can avoid medical underwriting when applying for a new Medigap plan.

If you’ve wanted a Medigap (or Medicare Supplement) plan in the past but have been unable to get one due to medical reasons, you now have a period where you can do that with no medical questions asked.

Don’t take this guaranteed issue right lightly.

Benefits of a Medigap Plan

Medicare Advantage plans require prior authorizations, and now you’re seeing that the government reimbursement rate can take that plan away from you. That is all quite the opposite when on a Medigap plan.

Yes, Medigap plans have a higher cost per month, but you will never deal with these government reimbursement problems. You will never deal with a provider dispute between a Medicare Advantage company and a provider.

Medigap plans do not engage in those agreements. They simply fill in the gaps and pay for everything that Original Medicare does not cover.

Medigap plans also do not have prior authorizations. I cannot emphasize enough the importance of that. All Medicare Advantage plans have prior authorizations, meaning the company has the right to approve or deny medical care on your behalf.

Medigap plans completely bypass that prior authorization process, and the benefits are fixed for life.

Final Thoughts

Keep an eye on your mail. See what’s happening to you personally. Be prepared, know your options, and decide what to do.

Hopefully, I haven’t overwhelmed you with information. If you should have any questions, call us directly. We would be happy to help you understand these changes for yourself.

If you get your letter, we can read through it and tell you if there’s anything you need to do or don’t need to do. We can also help analyze other companies to determine if you need a replacement and which would be the most suitable. Thanks!

Sources: Aetna Article | Humana Article | Premara BC Washington State | Centene Article

FAQs

- What should I do if I receive a notification that my Medicare Advantage plan is not renewing?

- When is the Medicare Annual Open Enrollment Period?

- What are guaranteed issue rights for Medicare Supplement plans?

- How do Medigap plans differ from Medicare Advantage plans?

- Can I switch from one Medicare Advantage plan to another outside of the Annual Open Enrollment Period?